Subscribers Only

Japan – Takaichi stresses fiscal responsibility

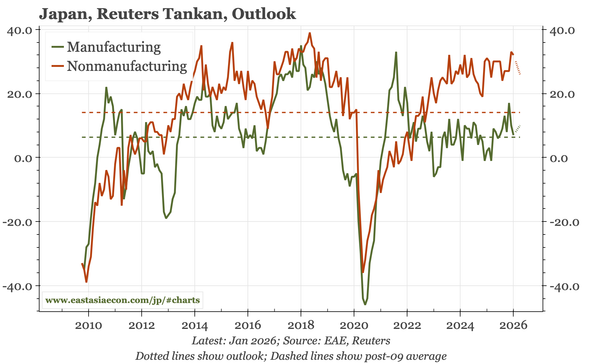

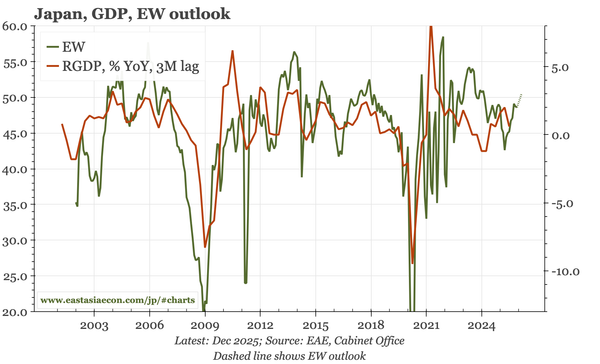

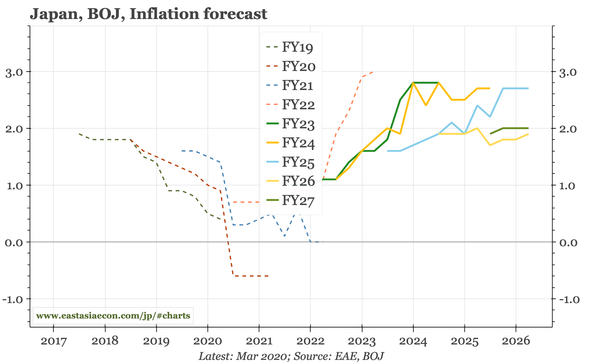

At its meeting today, the BOJ was again more positive on the outlook, but only incrementally. However, the authorities overall have been trying to put a lid on market volatility, perhaps via intervention, but also an interview by Takaichi. Data, meanwhile, show the economy still has good momentum.