Public Post

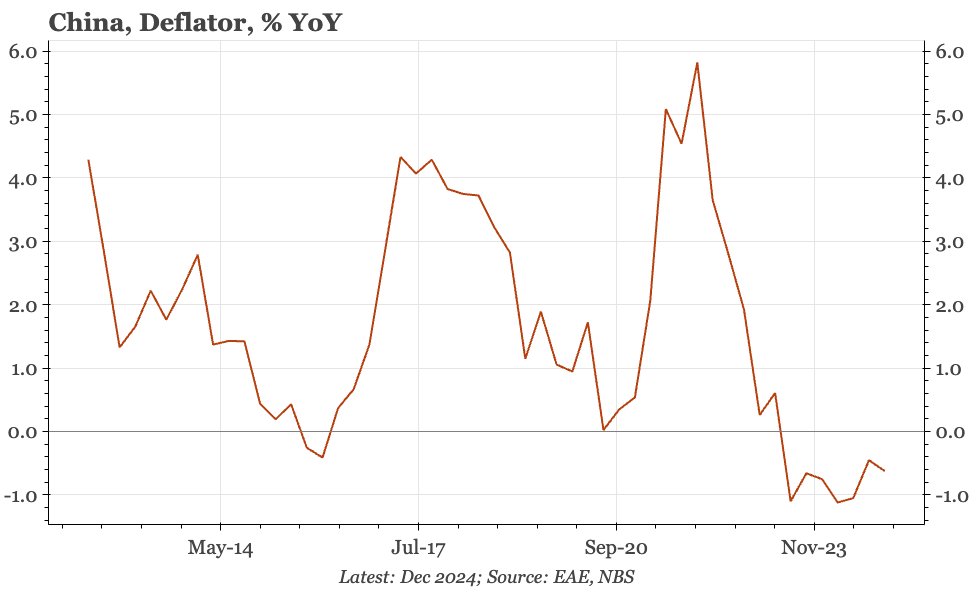

China – no change in Q4 deflator

The Q4 release was tougher to interpret than usual. It included the effect of the upwards revision in nominal GDP level announced at end-2024, but didn't give a back series for revised NGDP for earlier quarters. Today that history was published. The highlight? Still no change in the deflator.