Public Post

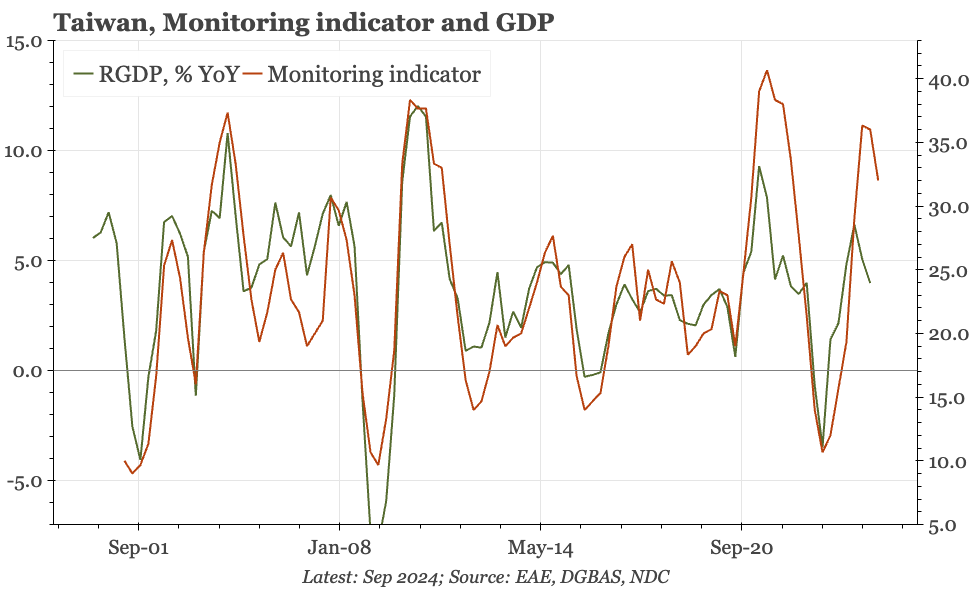

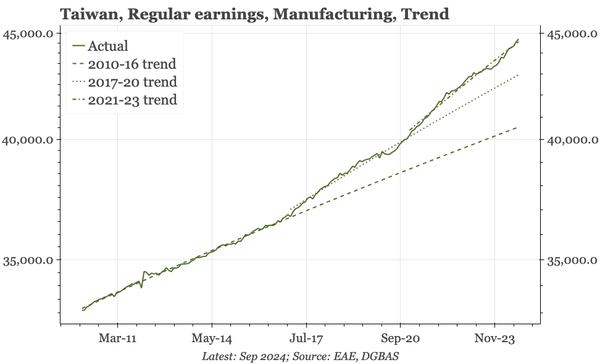

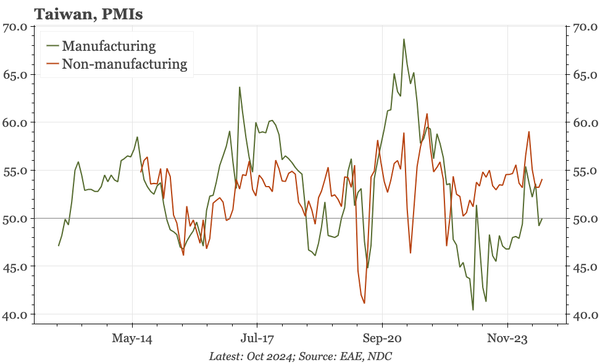

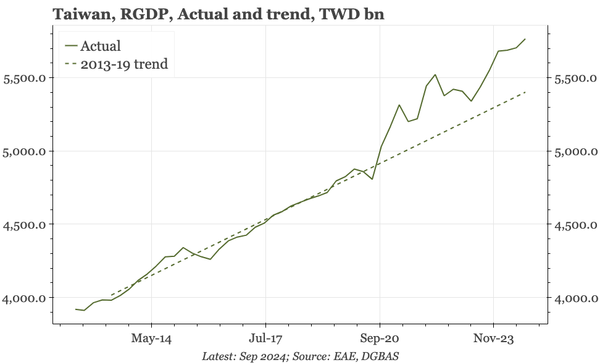

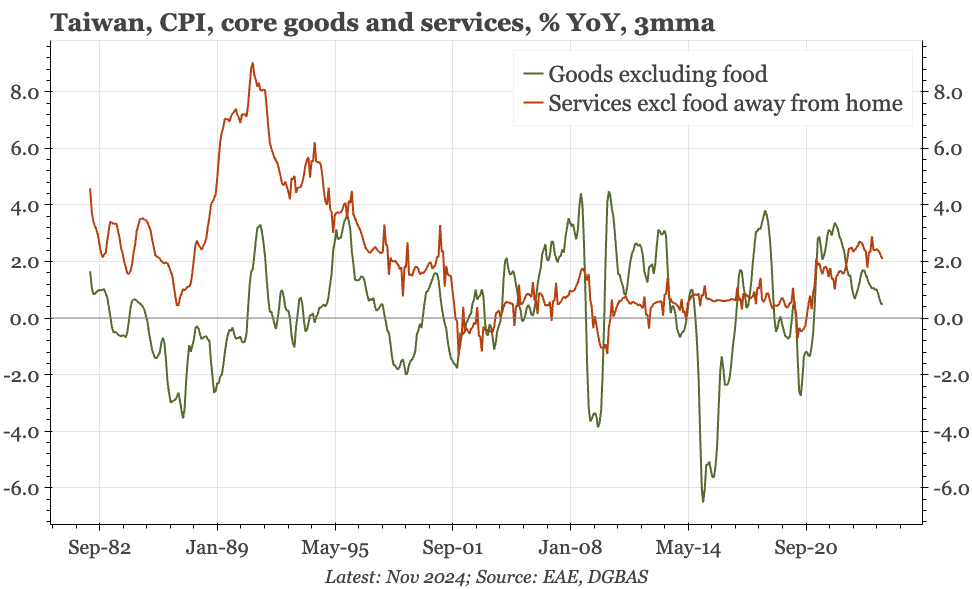

Taiwan – core inflation remaining around 2%

Inflation has eased, but outside of imported prices/goods, still isn't particularly soft. With the cycle also ok, the central bank won't be rushing to cut. So, while it would be usual to compare Taiwan's economy to Korea, in terms of current monetary policy, it has more in common with Japan.