Public Post

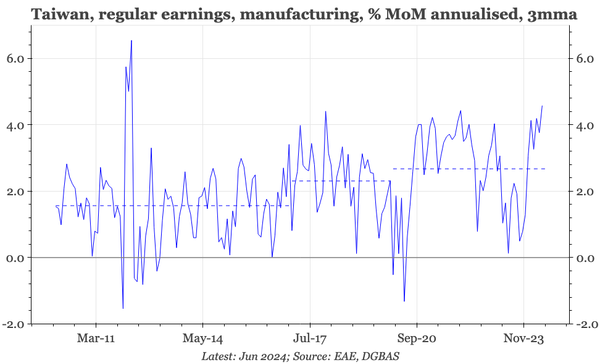

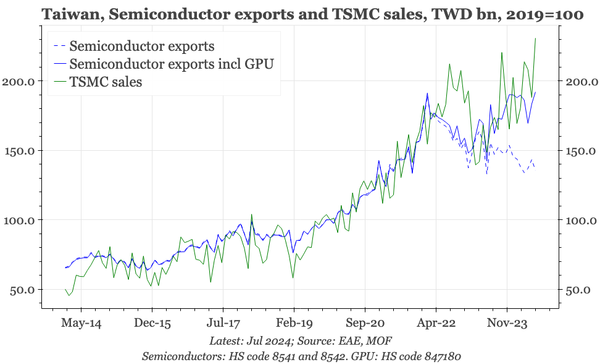

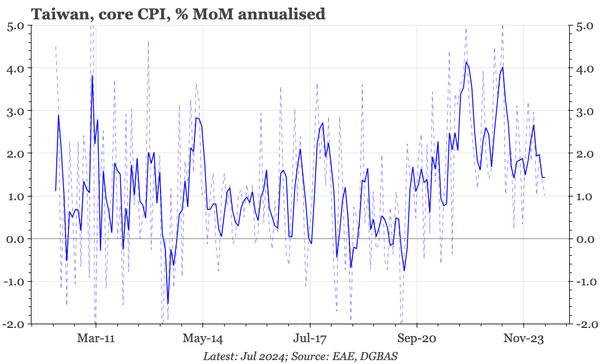

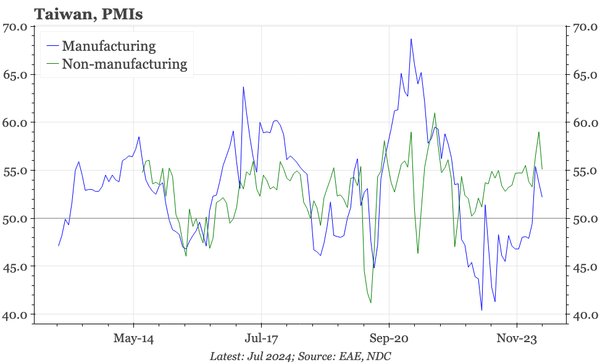

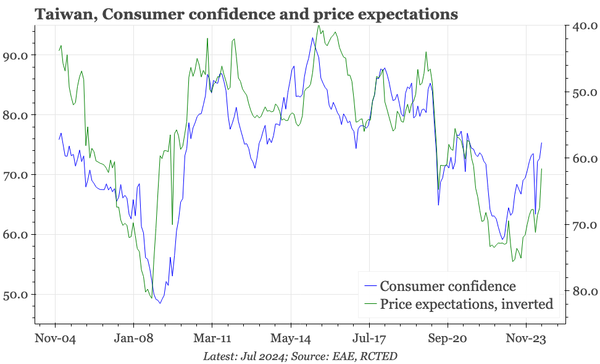

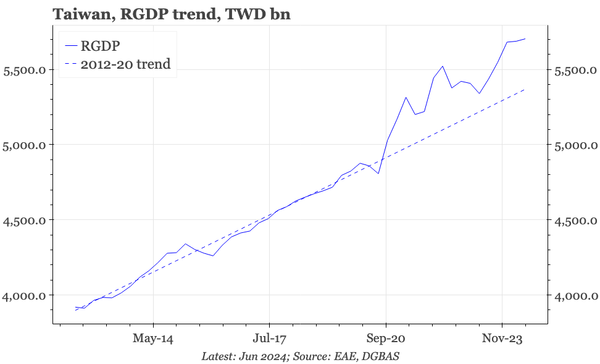

QTC: Taiwan – peaking outlook, but strong profile

In today's full Q2 release, officials kept the 24 GDP f'cast at 3.9%, saying “Exports are not bad, but just weaker than expected”. That characterisation is exactly right. But while cyclical momentum has been a bit disappointing, few other economies have a post-covid profile quite like Taiwan's.