Subscribers Only

East Asia Today

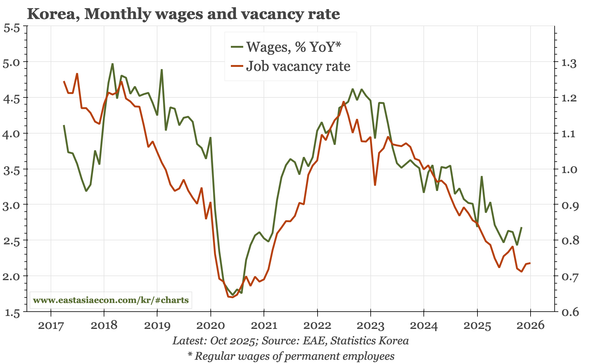

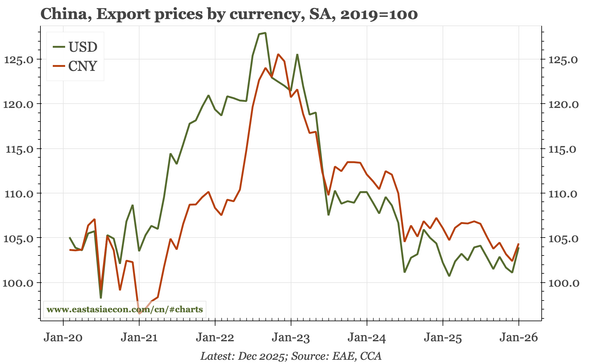

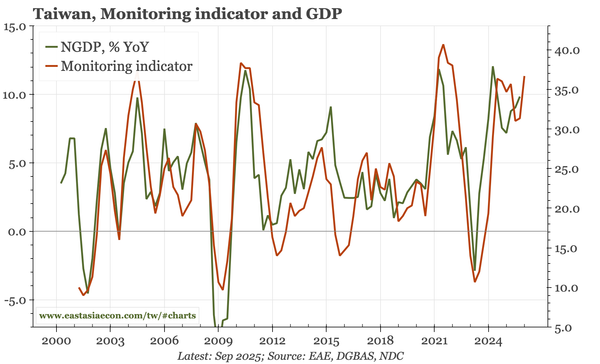

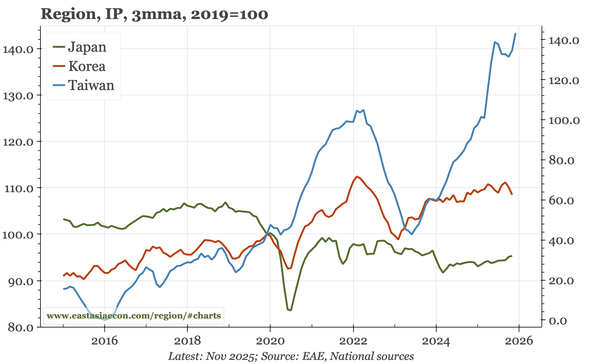

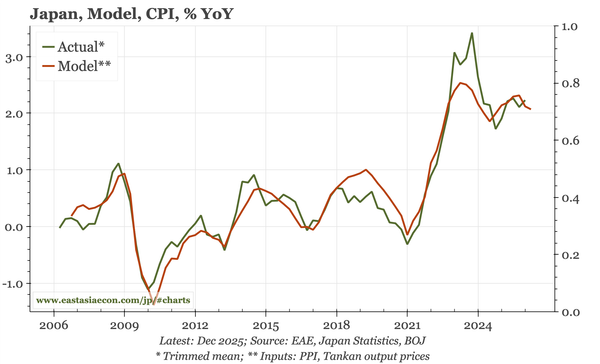

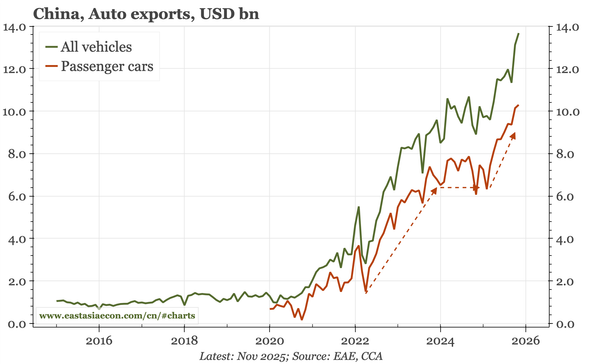

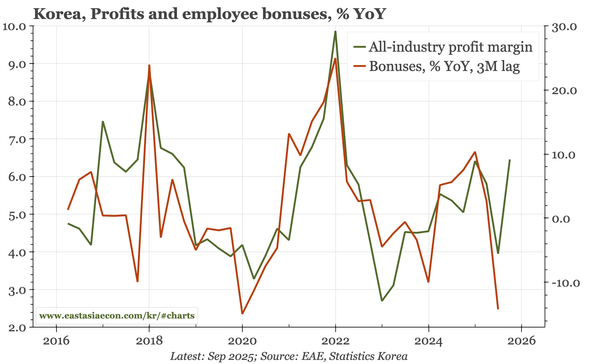

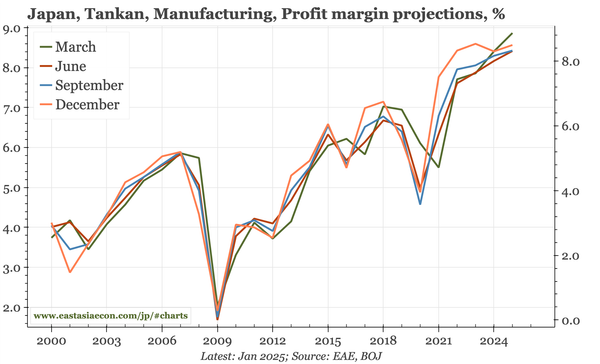

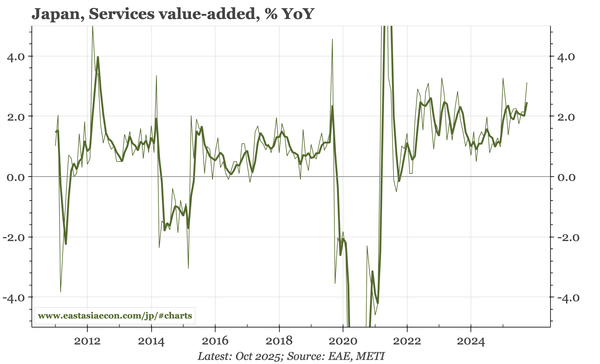

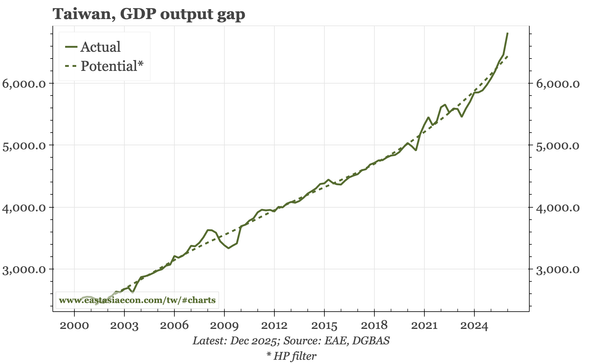

Lots of cycle updates today, with all the month-end data for Japan and Korea, as well as Q4 GDP data for Taiwan, which was another blow-out. China's main data release today showed service exports rising, though not nearly as quickly as exports of goods.