Subscribers Only

East Asia Today

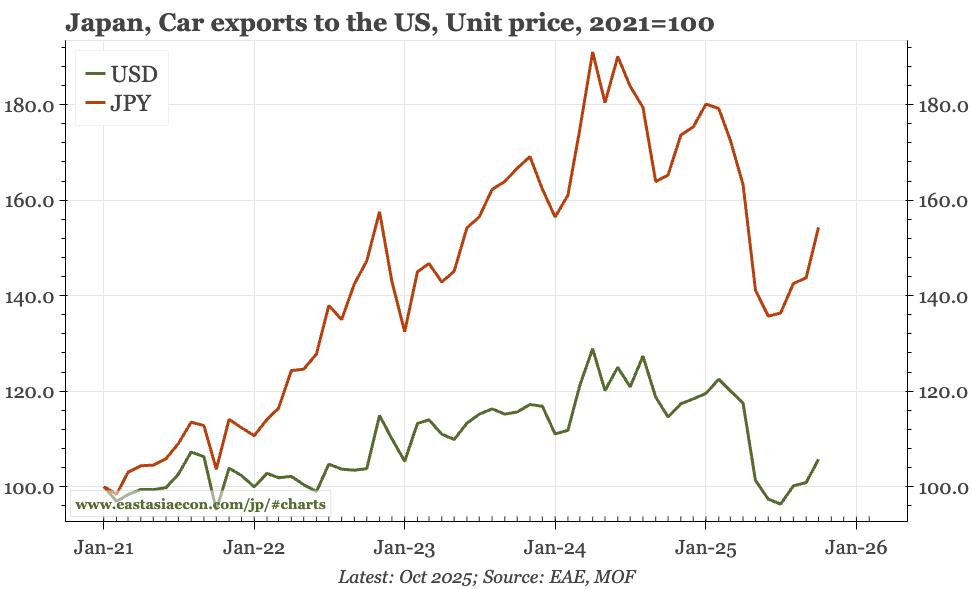

Some of the language in China's CEWC communiqué was encouraging. In Korea, while auto prices remain weak, overall export prices are rising and pushing up the terms of trade. Japan's monetary base is shrinking more quickly than any time since 2007. And my latest video, discussing Japan and the JPY.