Subscribers Only

East Asia Today

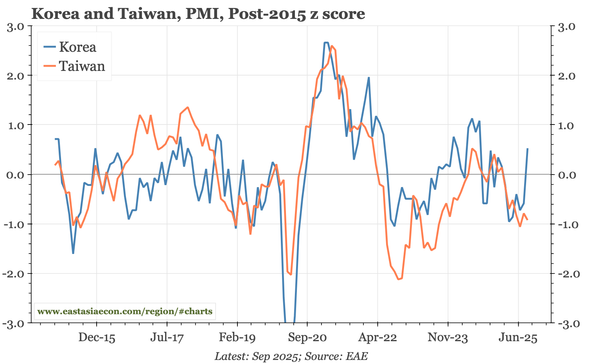

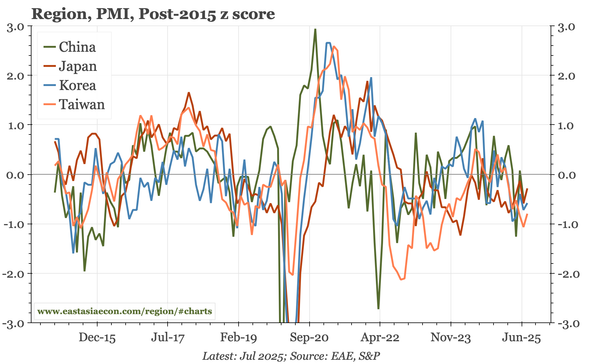

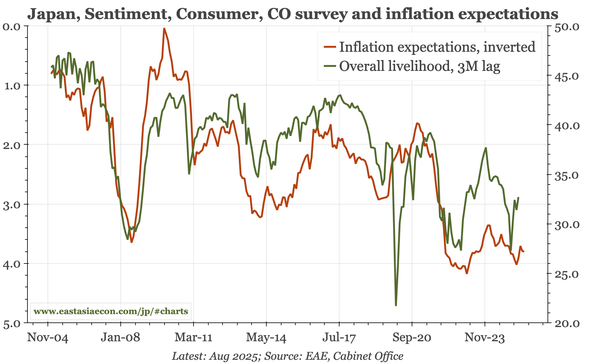

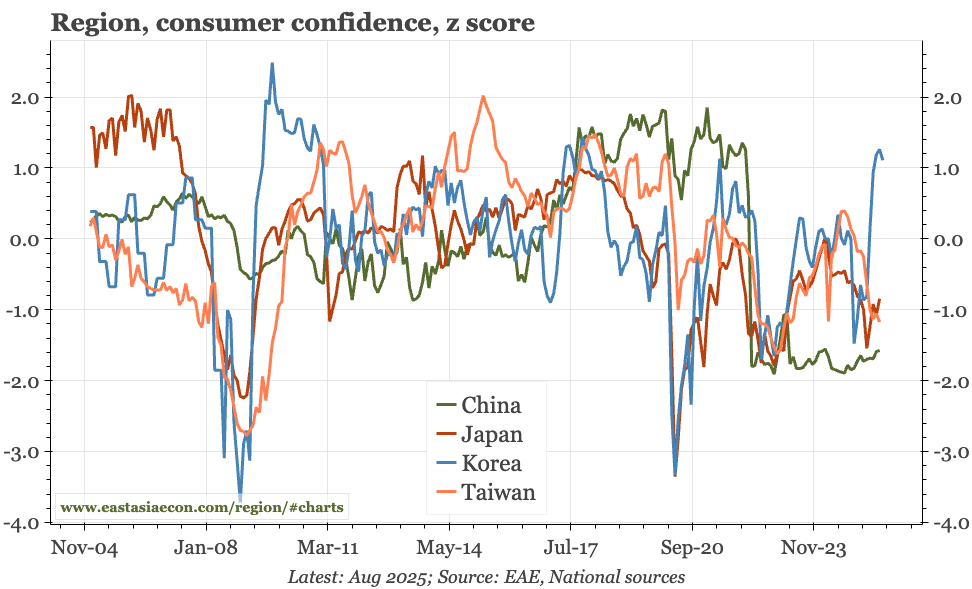

For a second day, there's most to report in Japan, with a speech from Ueda, the services PMI, labour market data and an updated output gap. With most of the surveys now in for September, we can also update regional comparisons of the soft data.