Subscribers Only

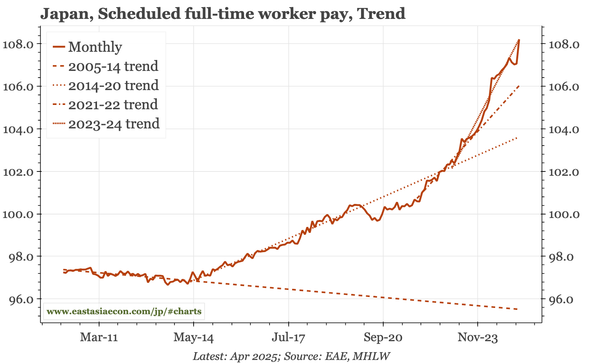

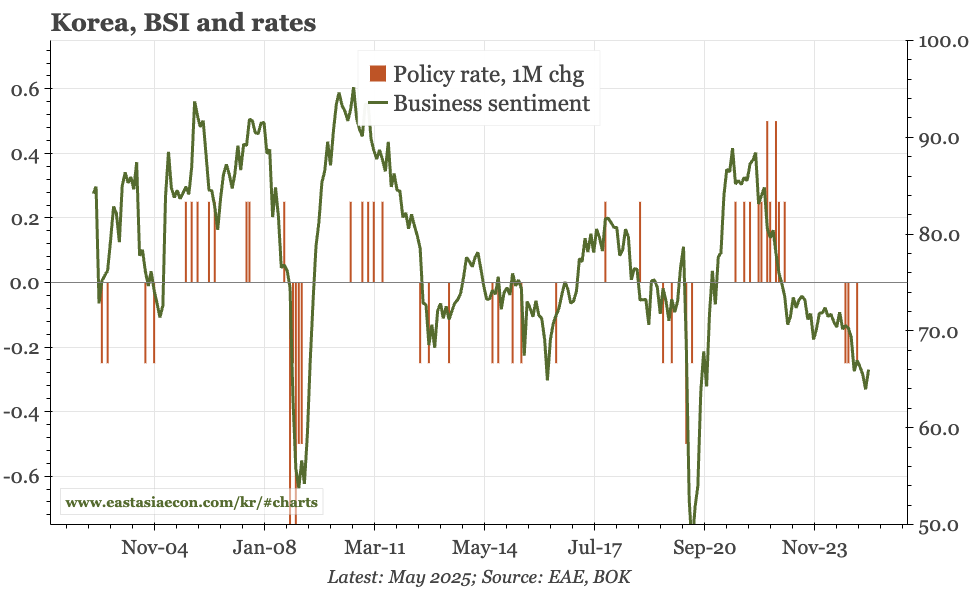

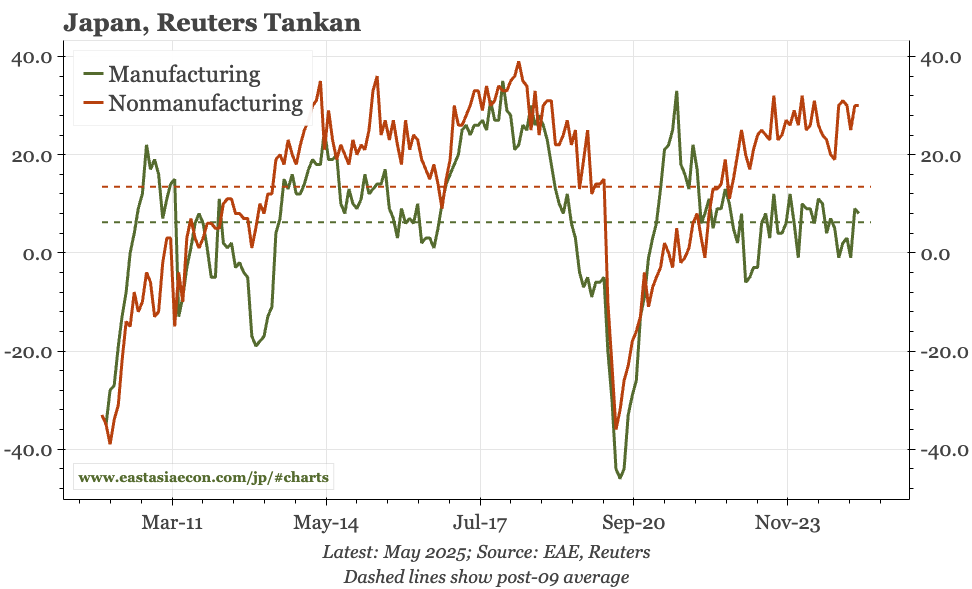

Japan – more subdued

Today's quarterly business outlook survey shows more incremental weakness in business sentiment, led by manufacturing. That's another sign that tariffs in particular have taken the edge of the cycle. However, there's not yet signs of real deterioration, which capex firm and employment still tight.