Subscribers Only

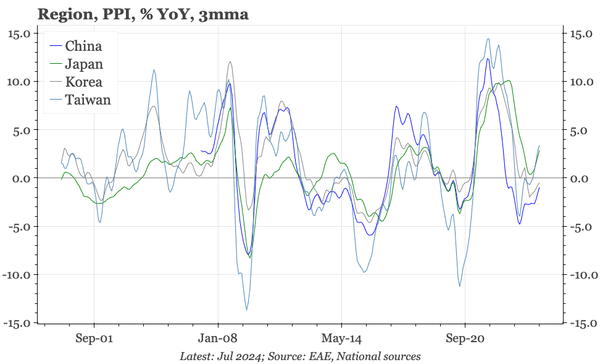

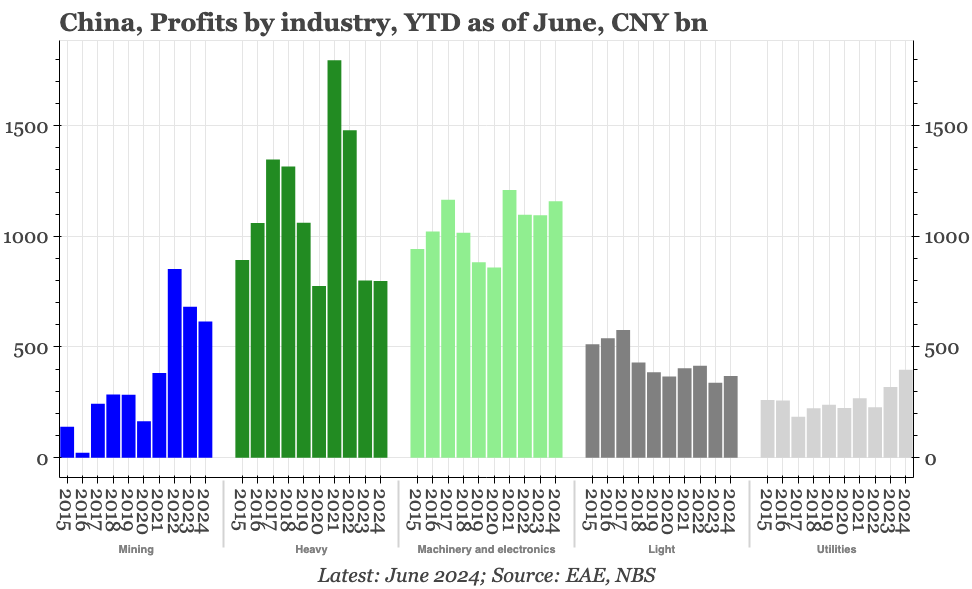

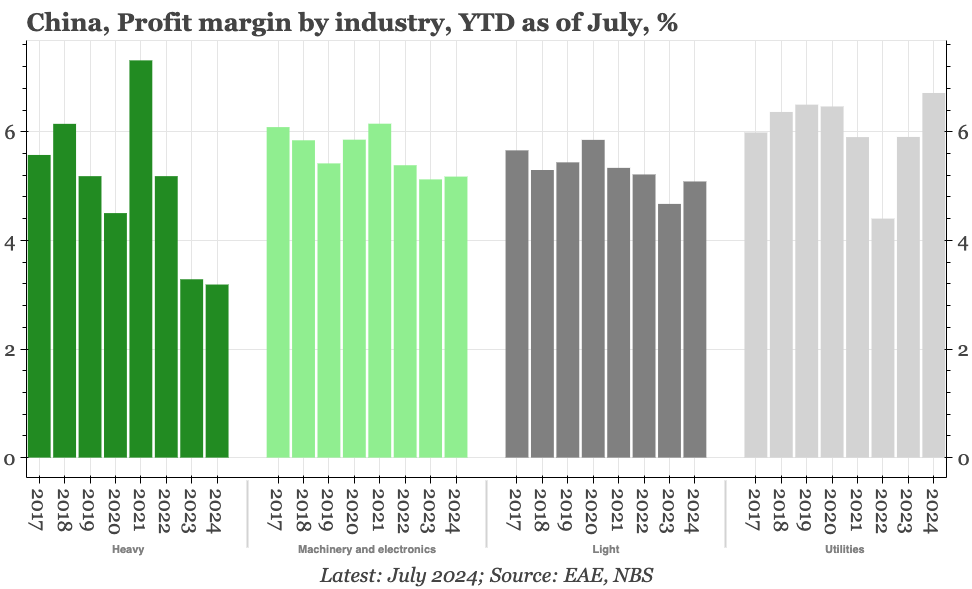

China – heavy industry still the big drag

Yesterday, officials claimed high-tech industry contributed 60% of the aggregate rise in industrial earnings through July. That's partly because profitability in heavy industry is so poor. Even then, overall profits still only rose 4%. New sectors still aren't strong enough to really lift the whole.