Subscribers Only

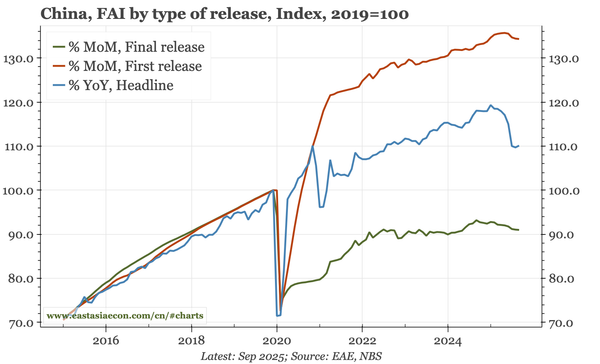

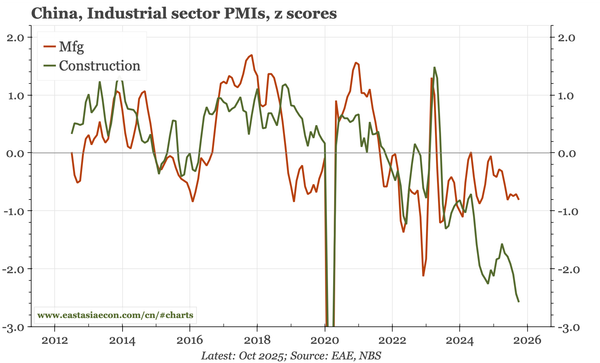

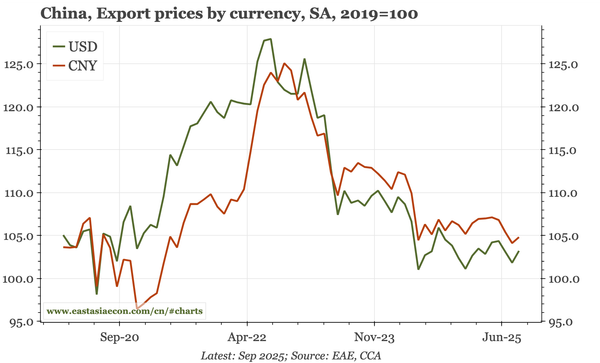

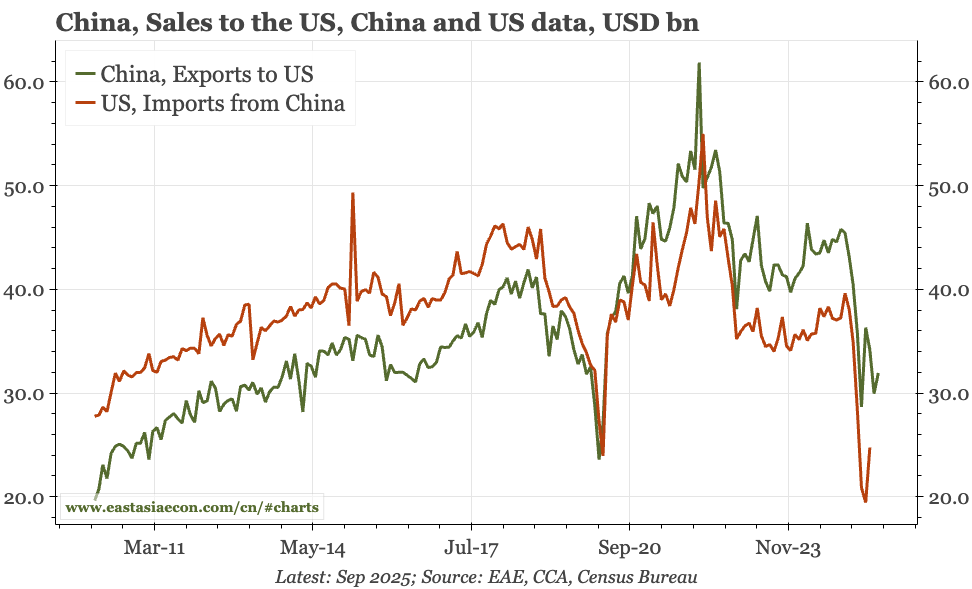

China – not yet soft enough

The October data are soft, but mixed: on the one hand investment terrible and property weak, on the other, output and services more stable. That probably doesn't add up to a change in policy. My idea of stabilisation does look a bit more tenuous, and would be over if upstream prices give way again.