East Asia Today

While the big news is the bloodbath in markets, particularly Korea, there were lots of data releases today. They show that before the Iran war, economic momentum was good in Japan and Taiwan, and poor in Korea. In China, it could be either, depending on which PMI you believe.

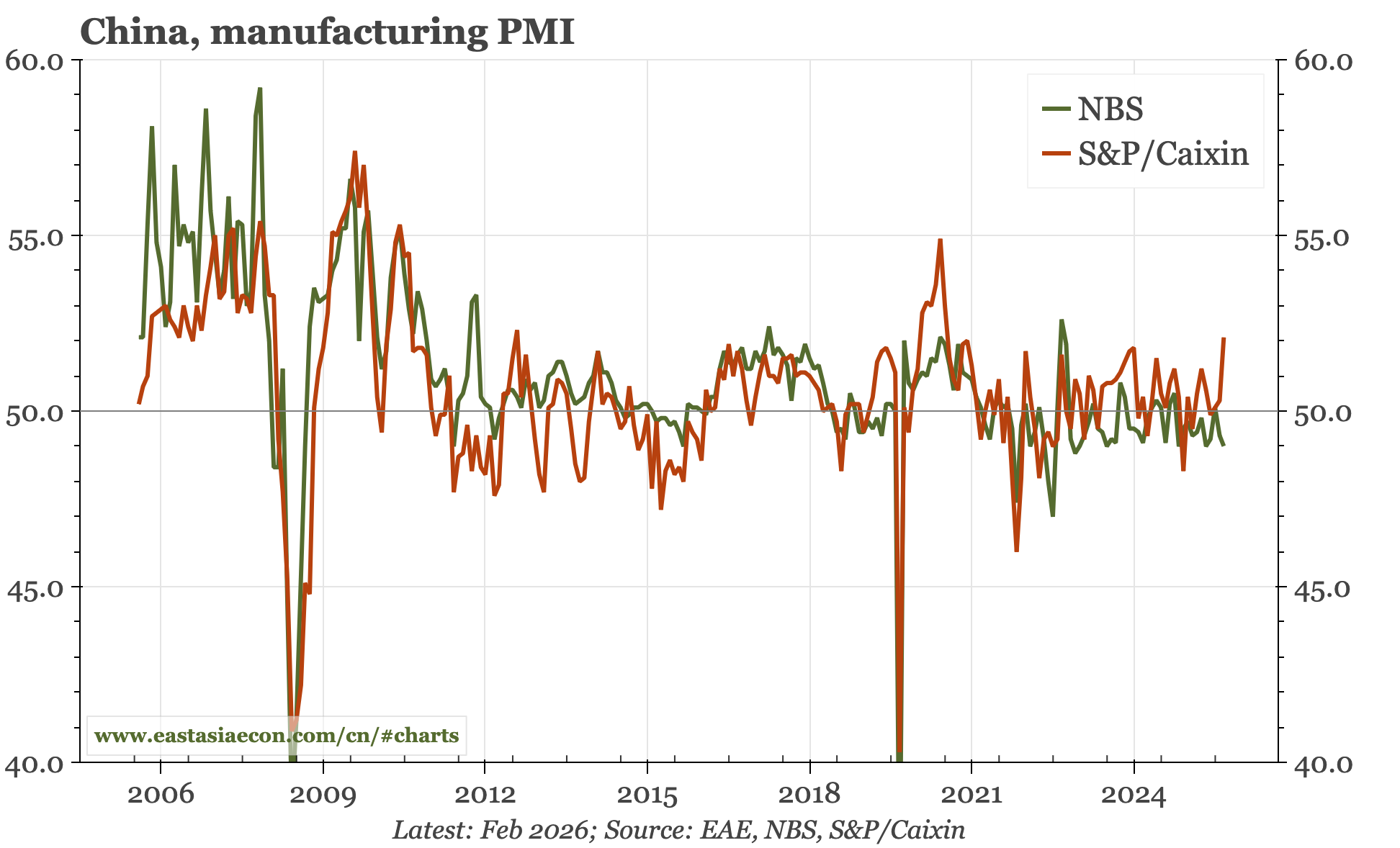

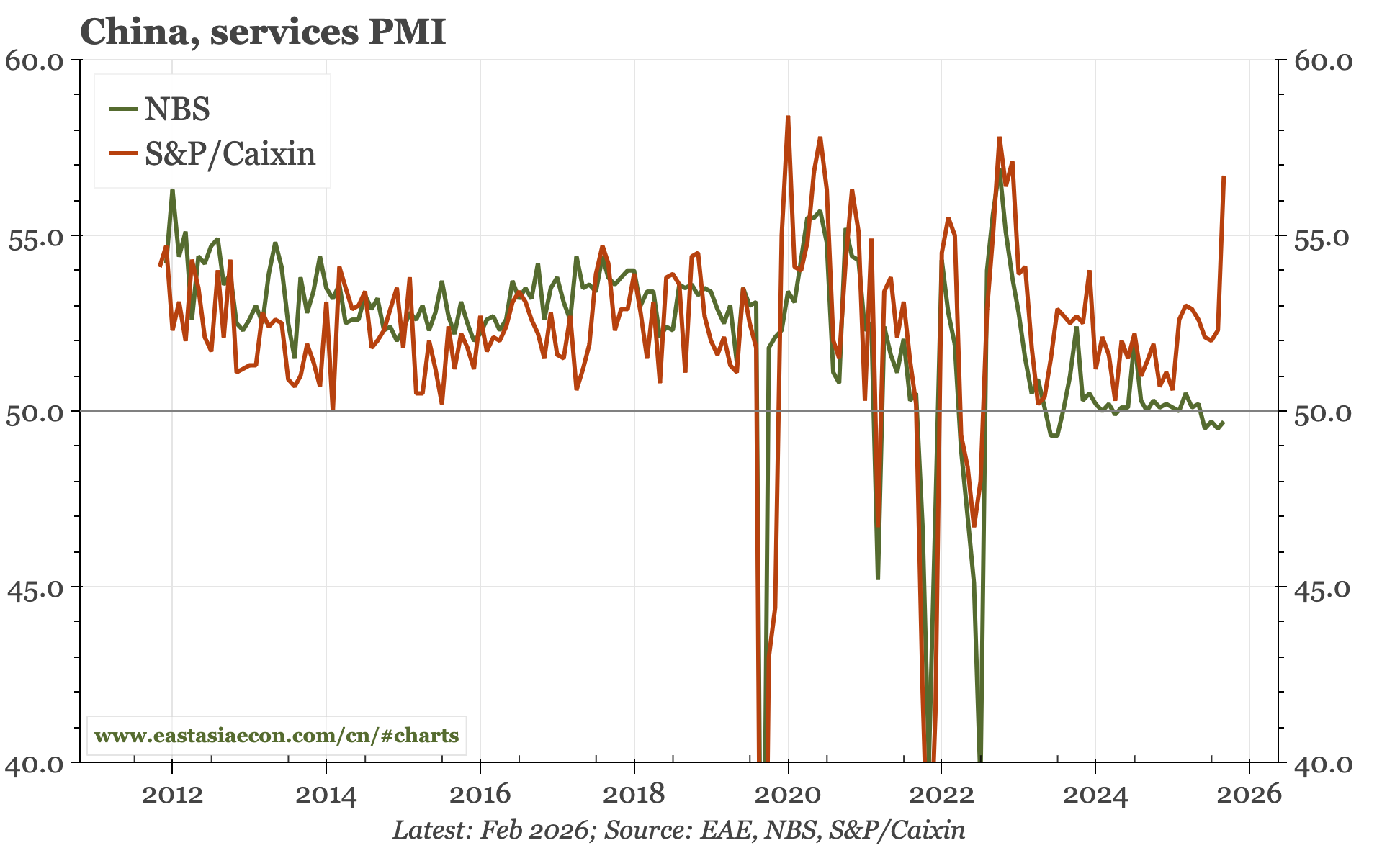

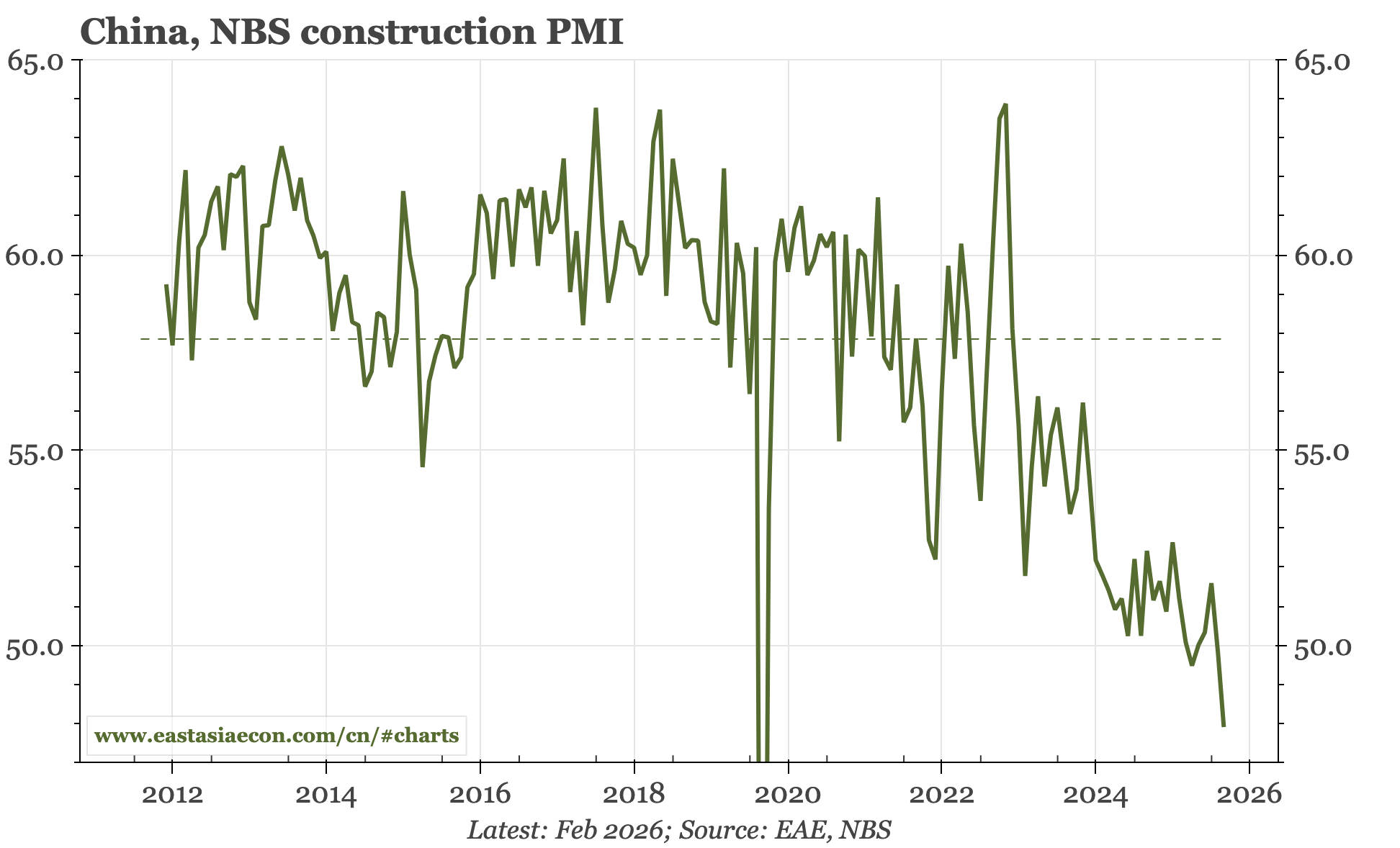

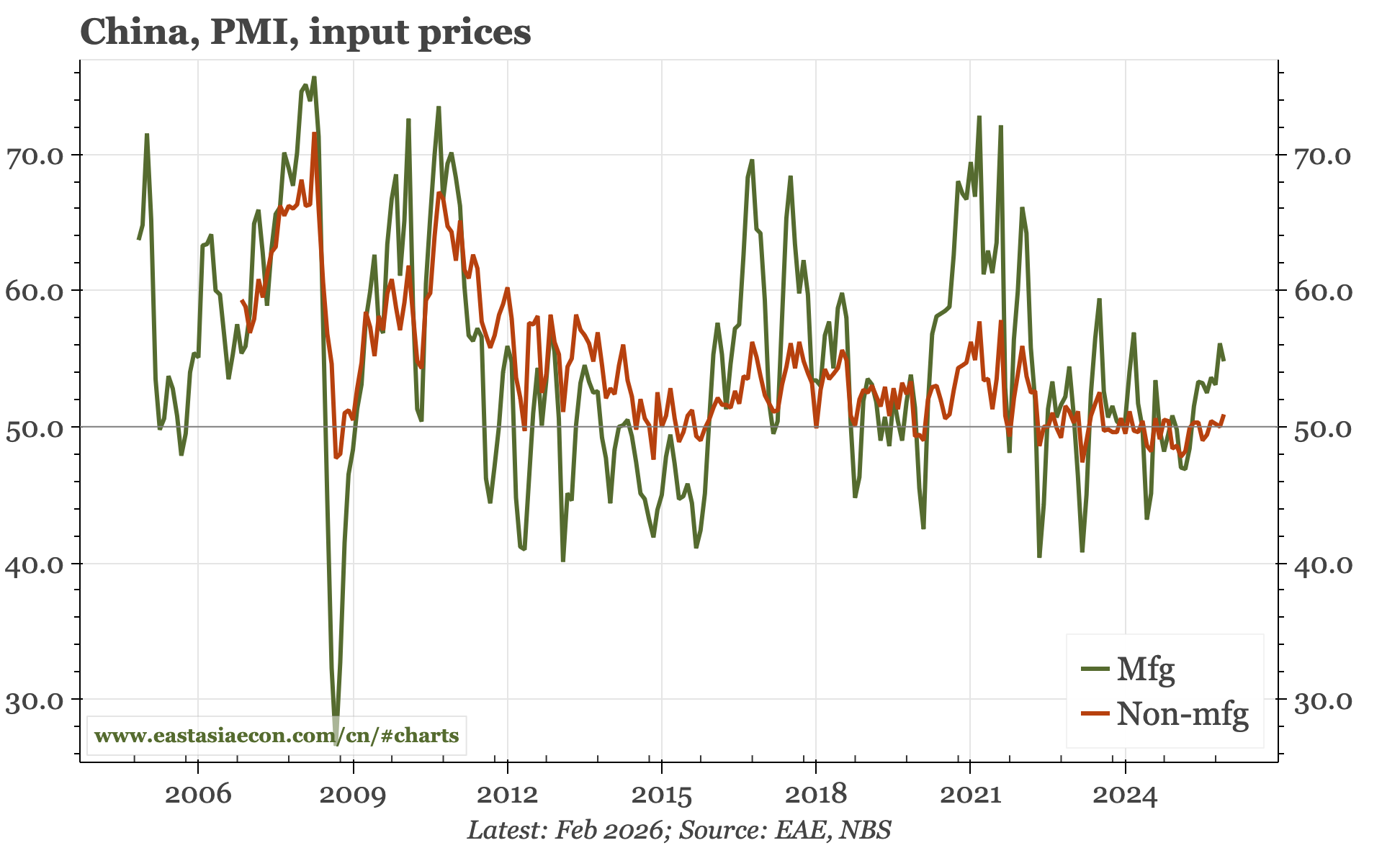

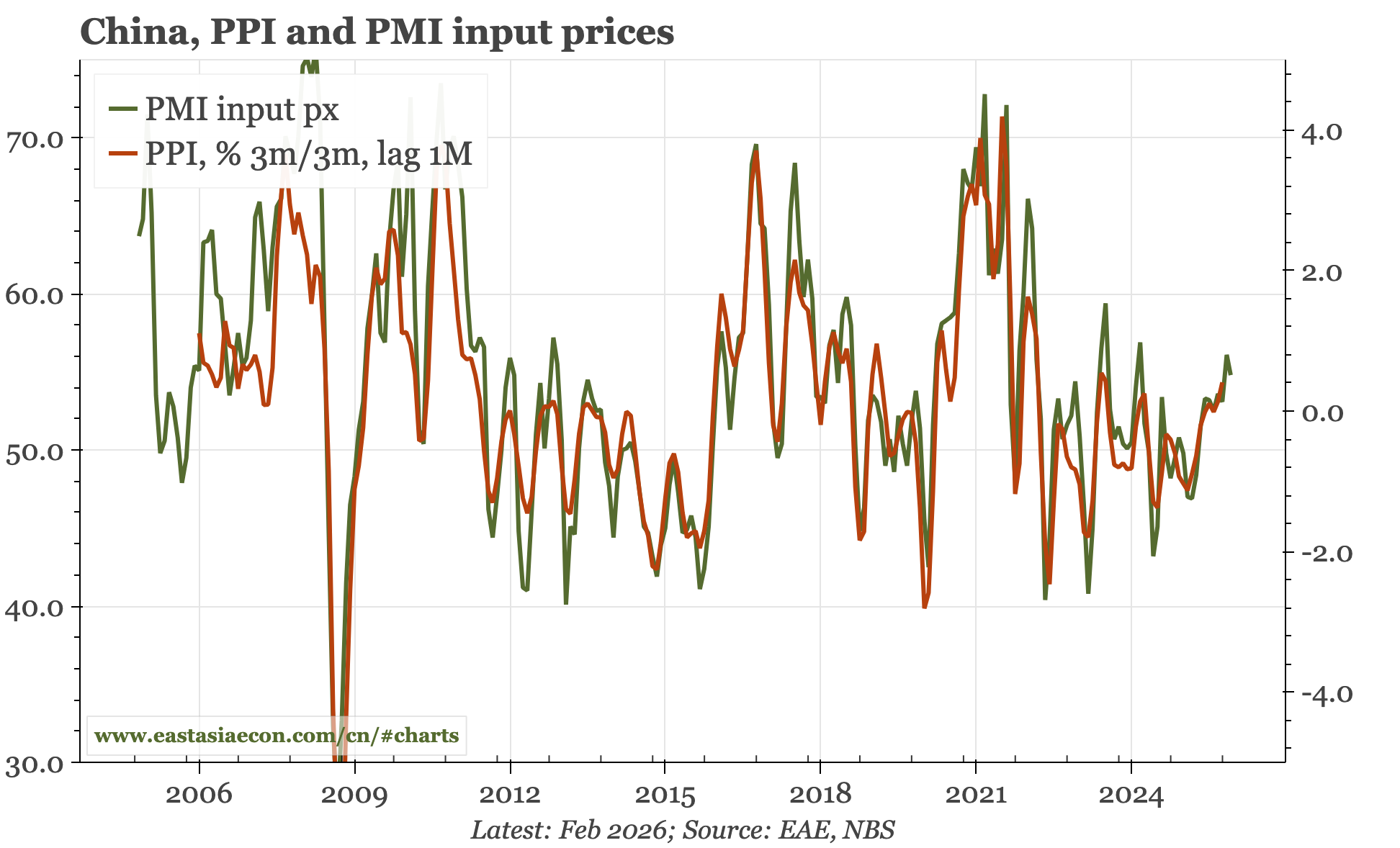

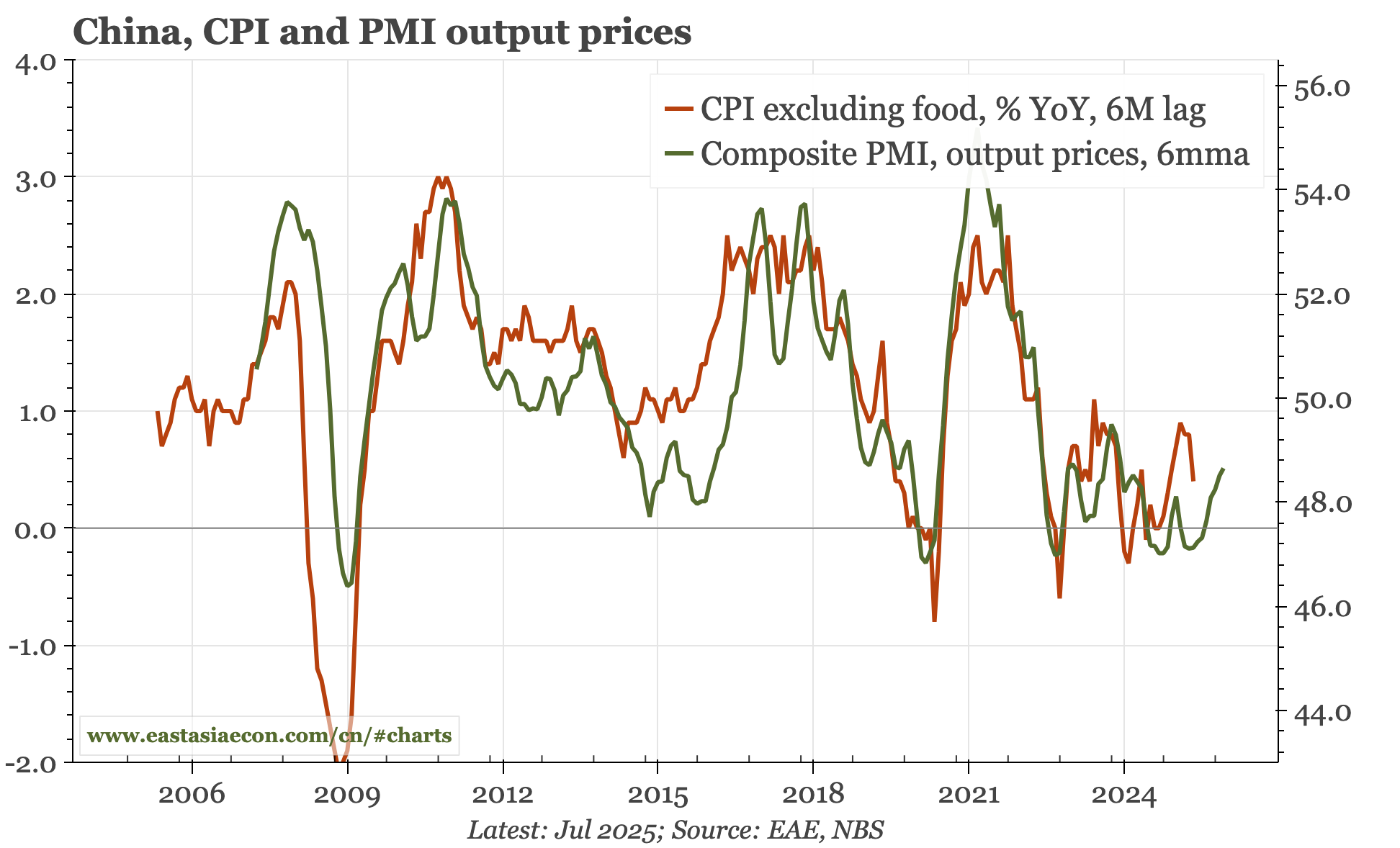

Cycle update – PMIs diverging more than usual. The S&P/RatingDog PMIs suggest an economy that is finally recovering. The official PMIs, by contrast, indicate continued sluggishness. I am inclined to think there is no change, at least until the LNY impact fades. The one common theme is firmer input prices, even before an energy price shock.

If you aren't yet a subscriber, please consider becoming one! This daily product is designed for individuals, but we also have data services and a much more comprehensive offering for financial institutions. If you have any questions or feedback, please get in touch with me directly.

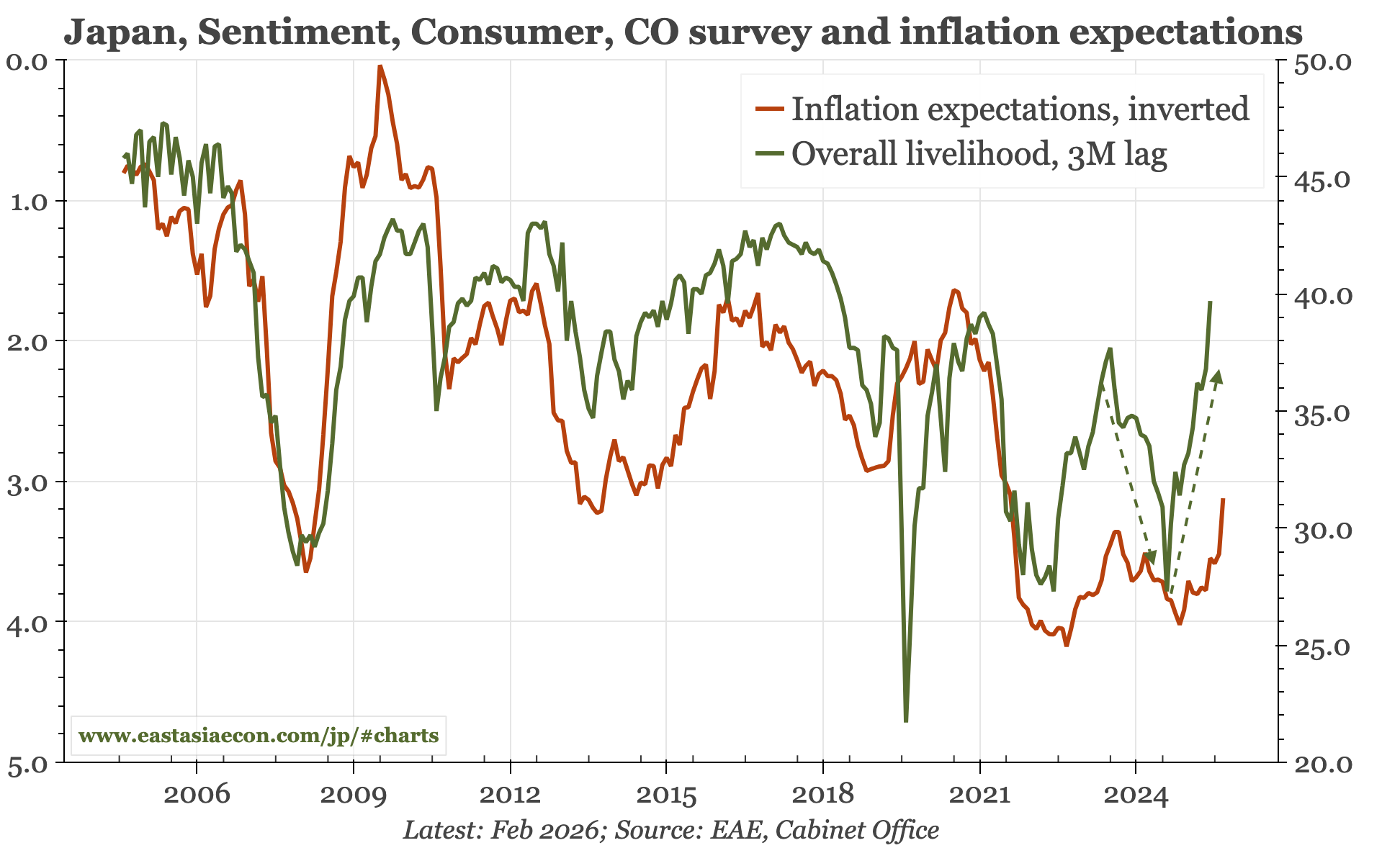

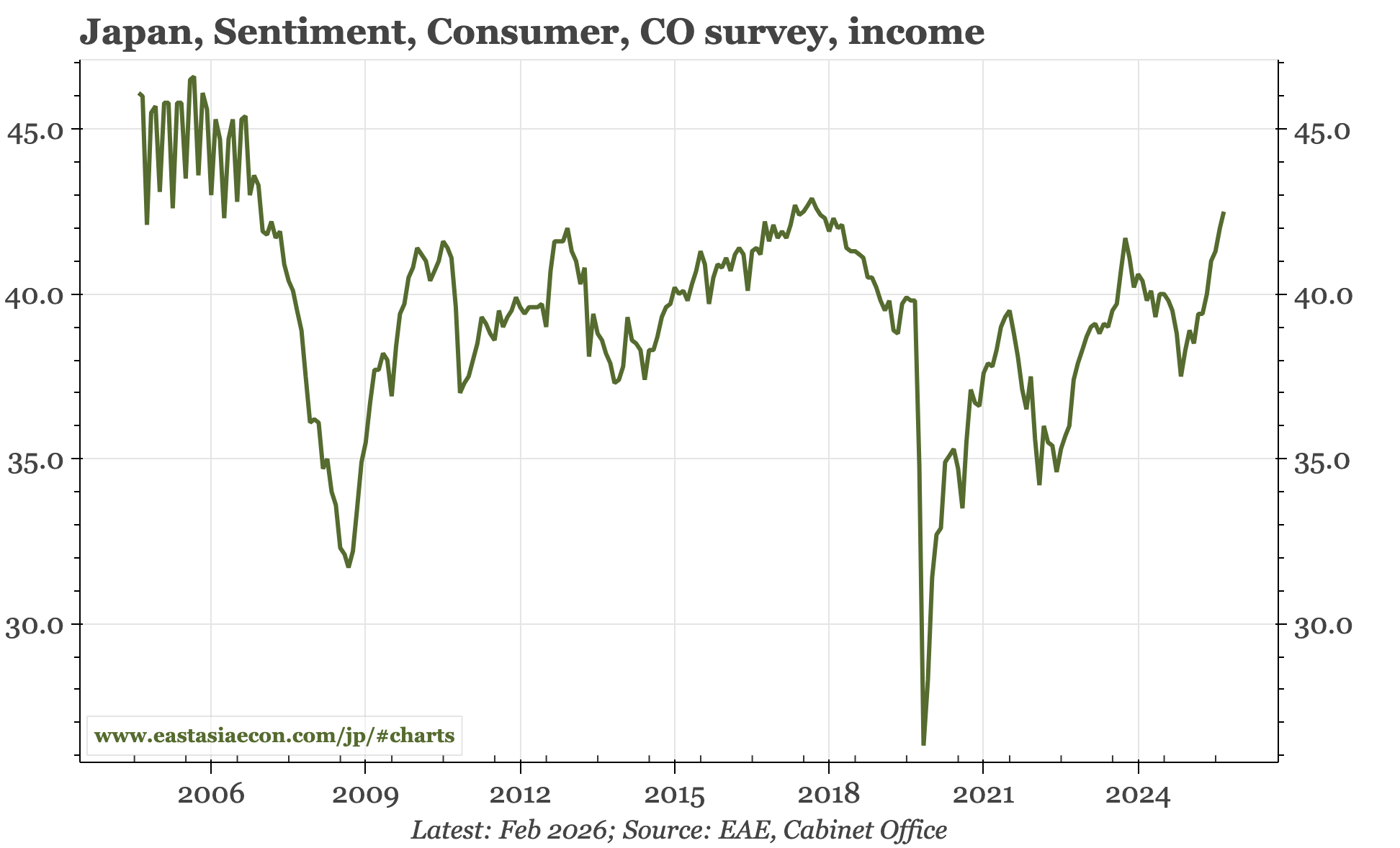

Today's consumer confidence survey shows again that, at least before the Iran war, the economy was on an upswing. Helped by the fall in inflation and optimism following the election, consumer confidence finally regained levels seen before the tax hike of 2019.

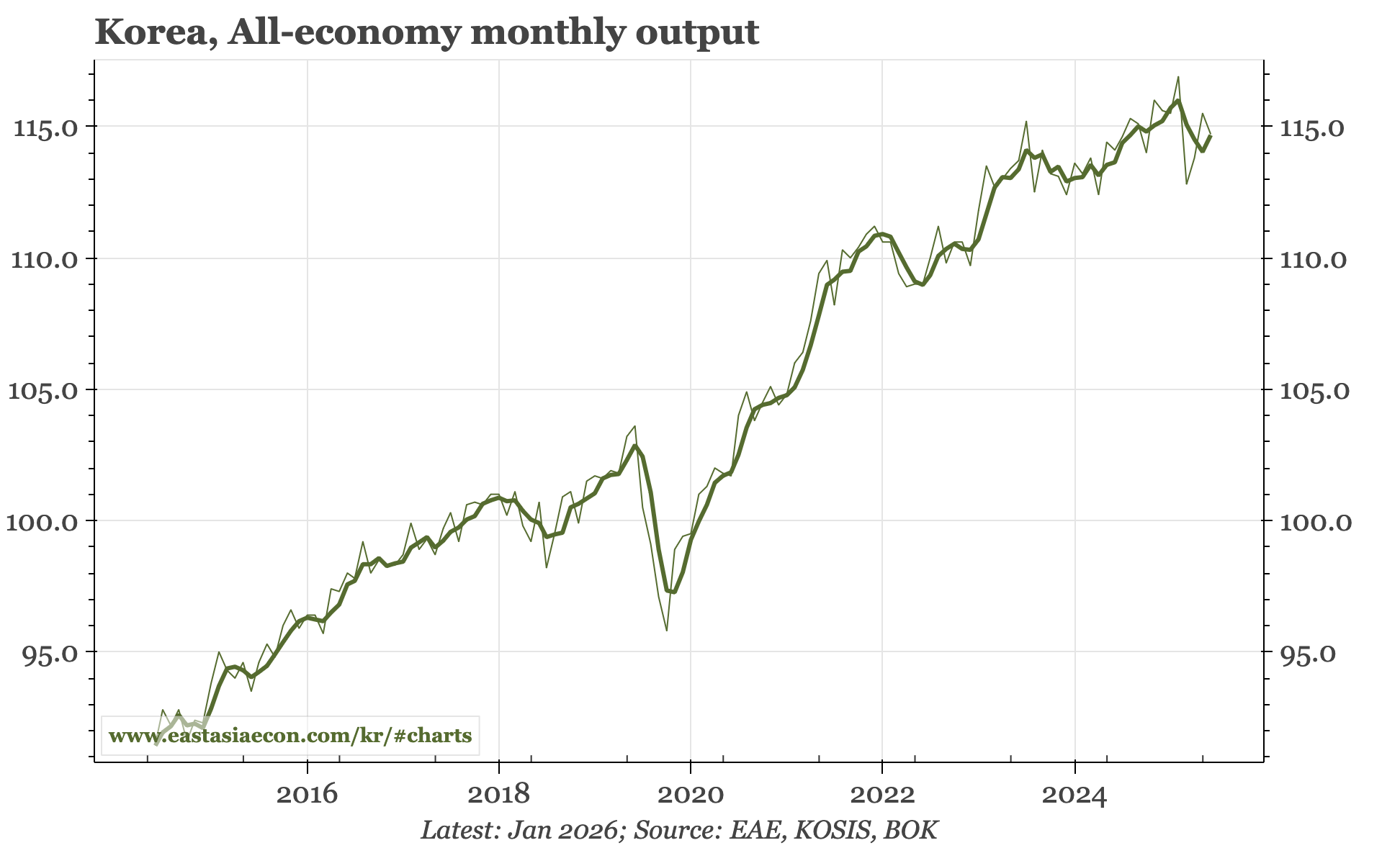

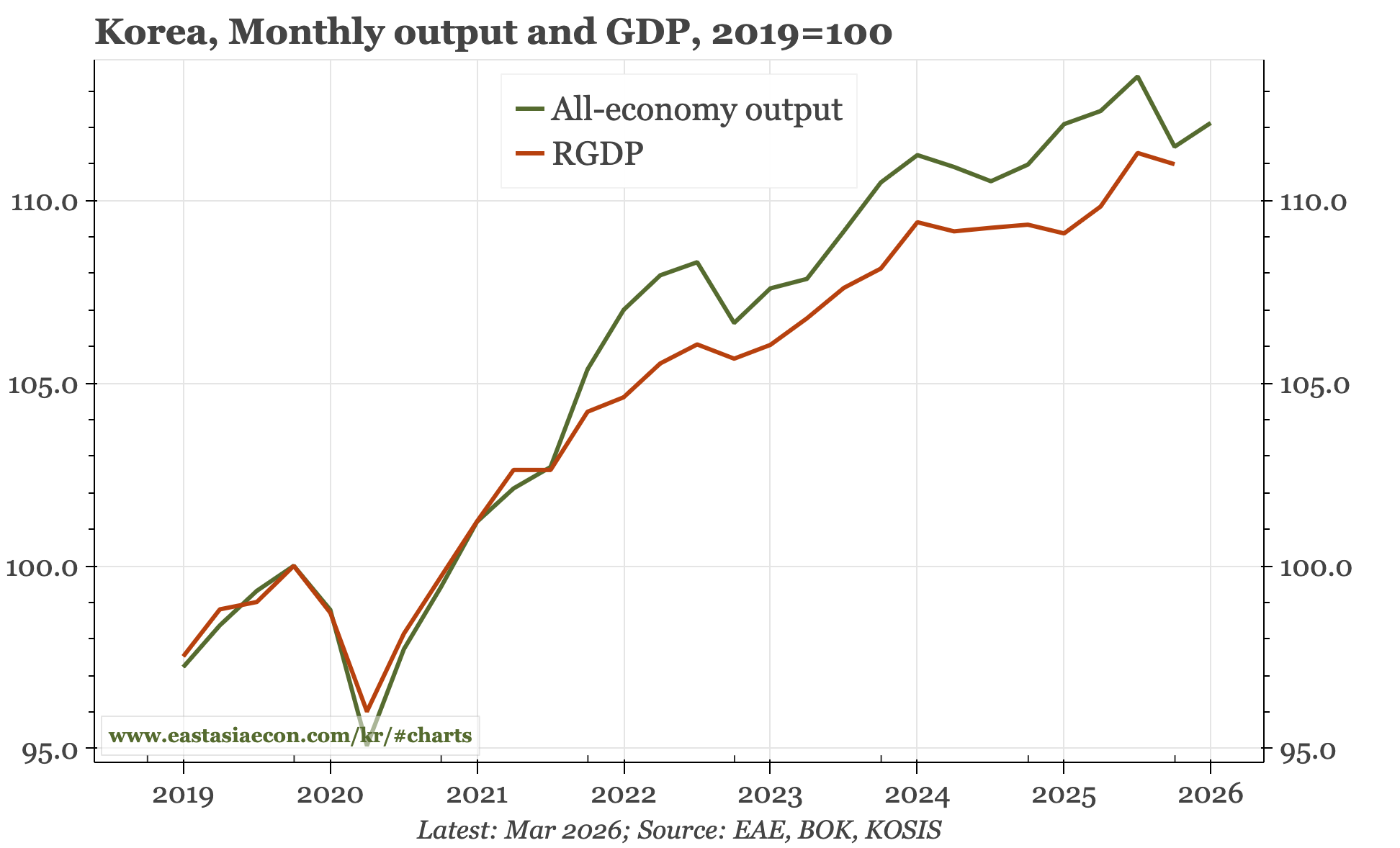

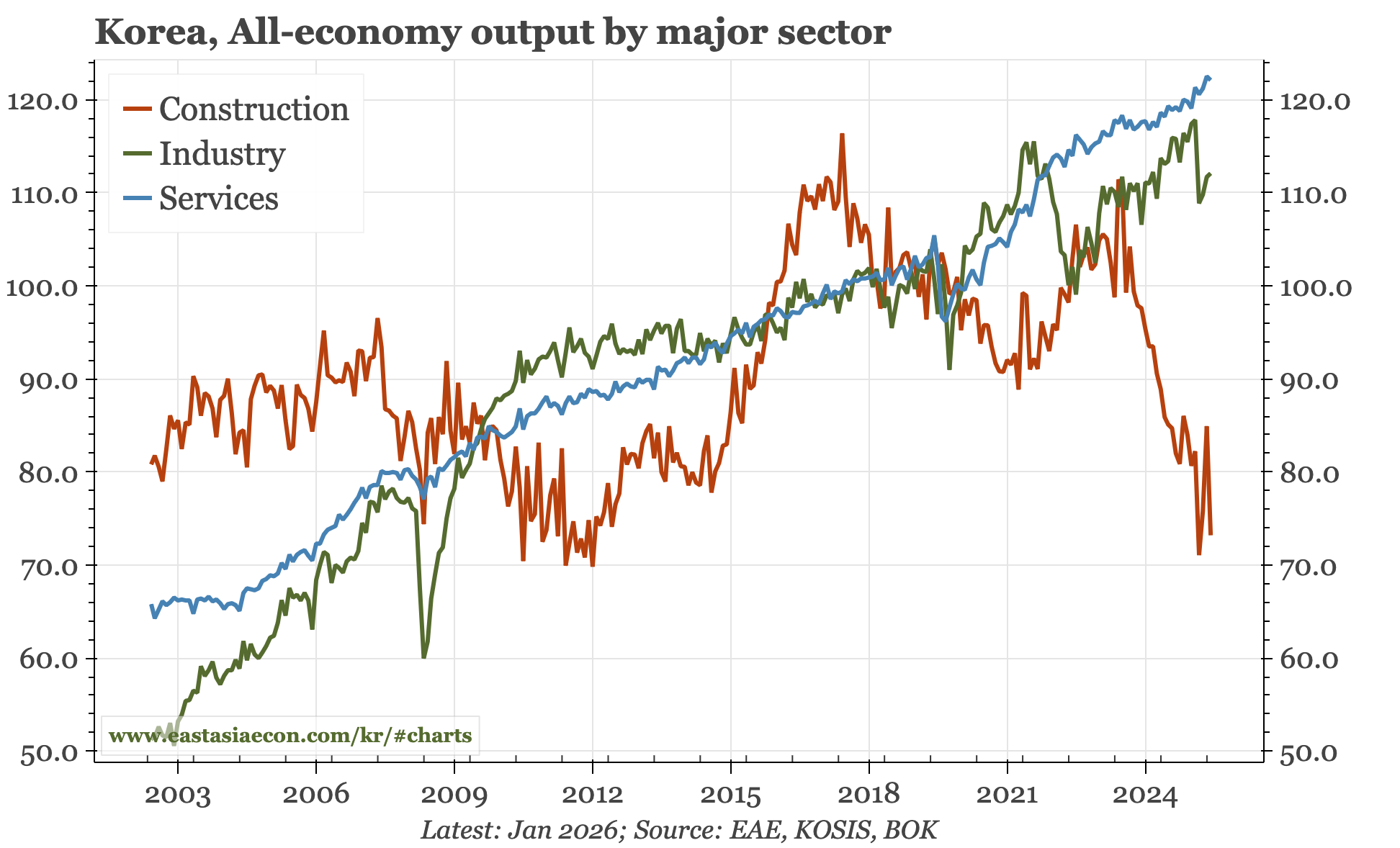

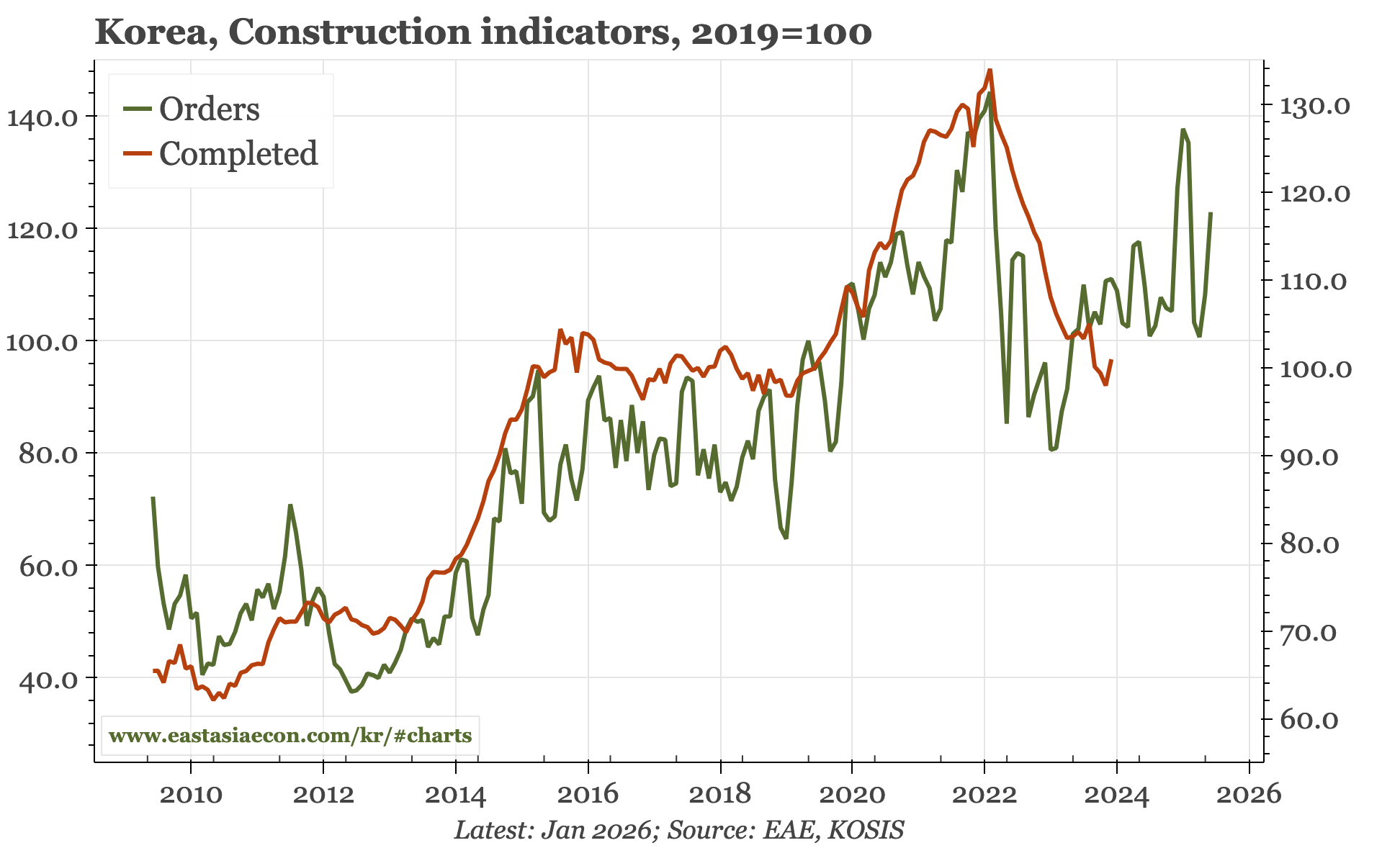

The BOK leadership will be concentrating today on the bloodbath in equities and particularly the KRW rather than statistics. But the dataflow is consistent with their cautiousness last week. All-economy output in January remained below the Q3 peak. Construction output is back near the low of October. Capex isn't so weak, but doesn't show any sign of getting lifted by the semi cycle.

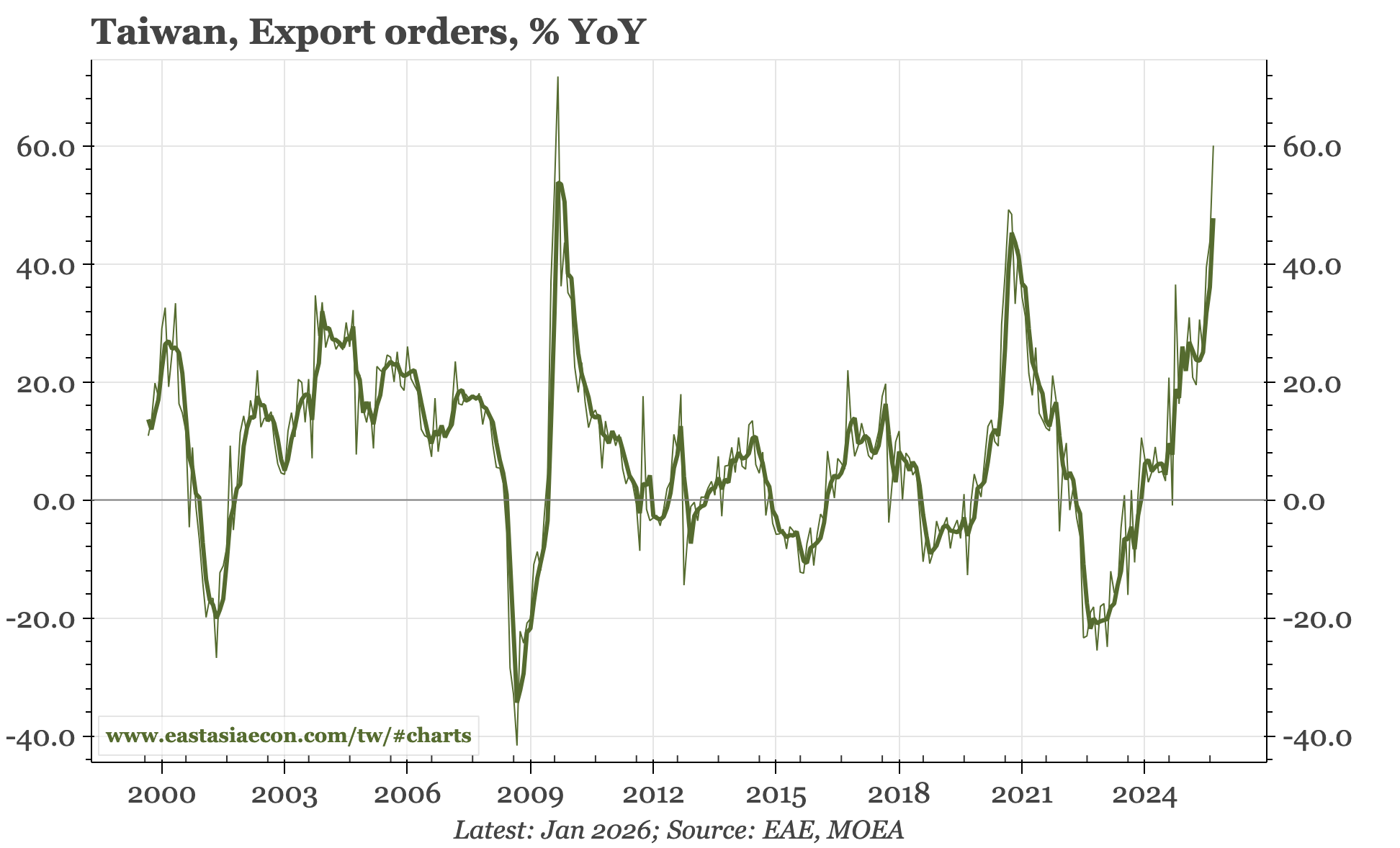

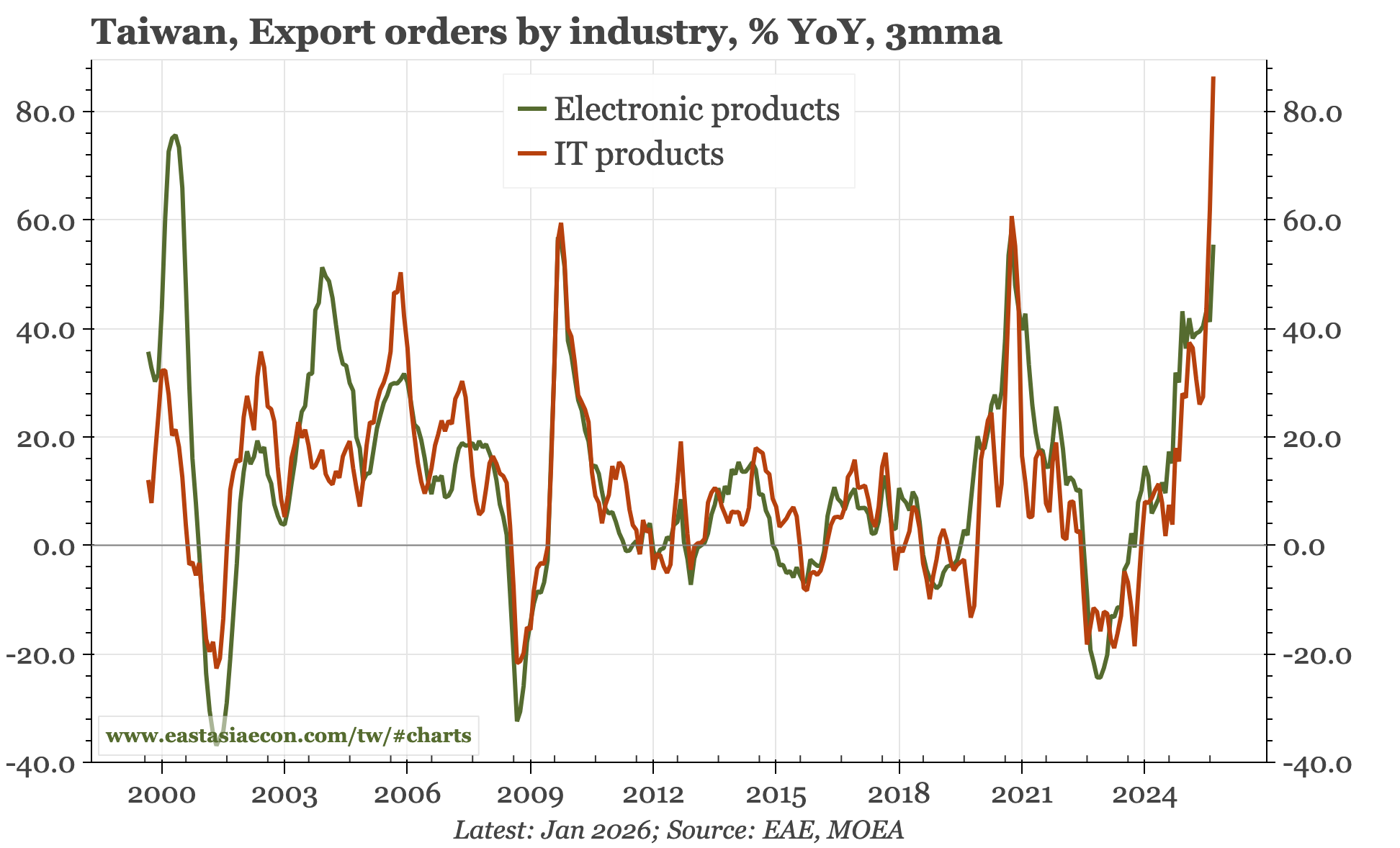

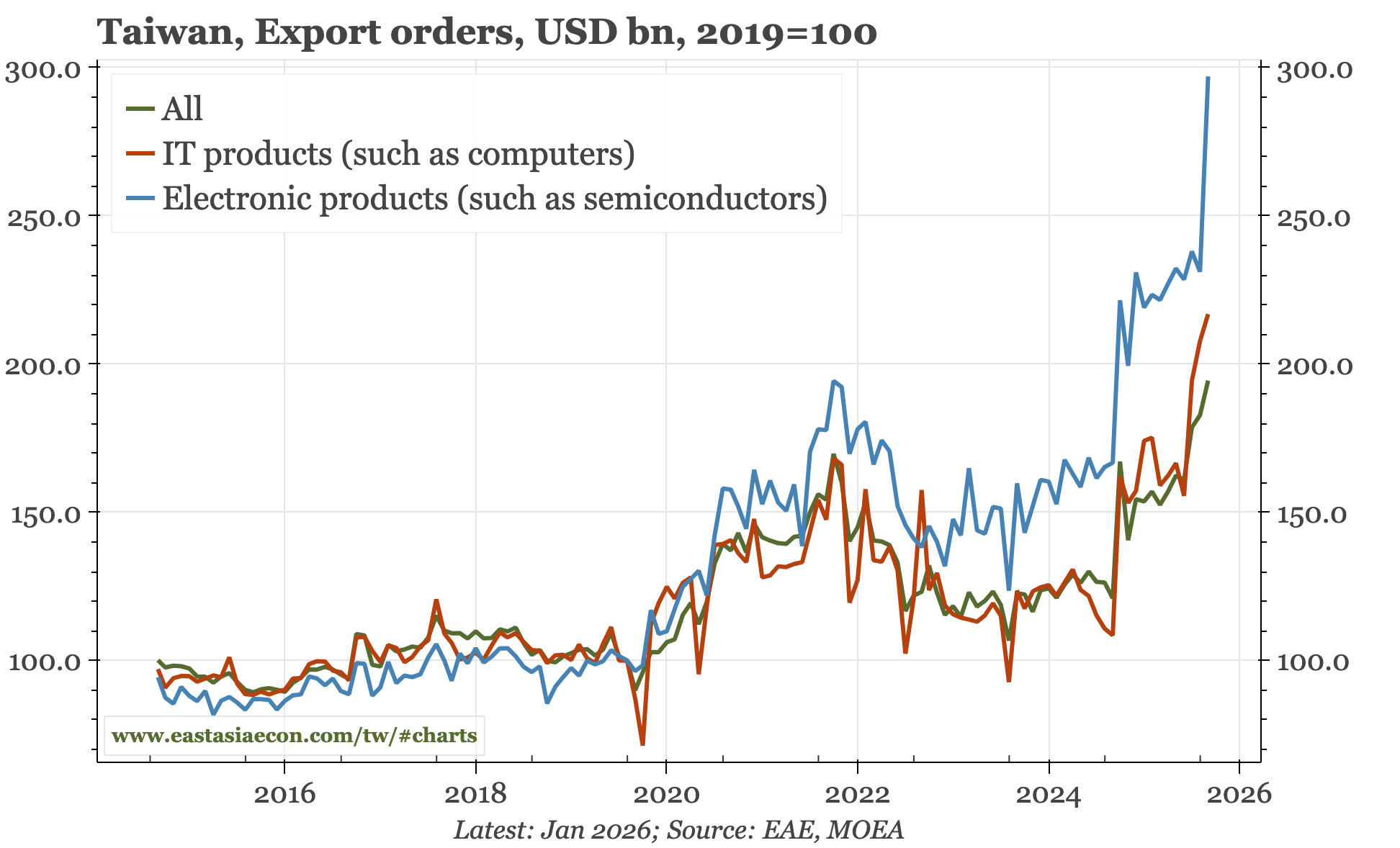

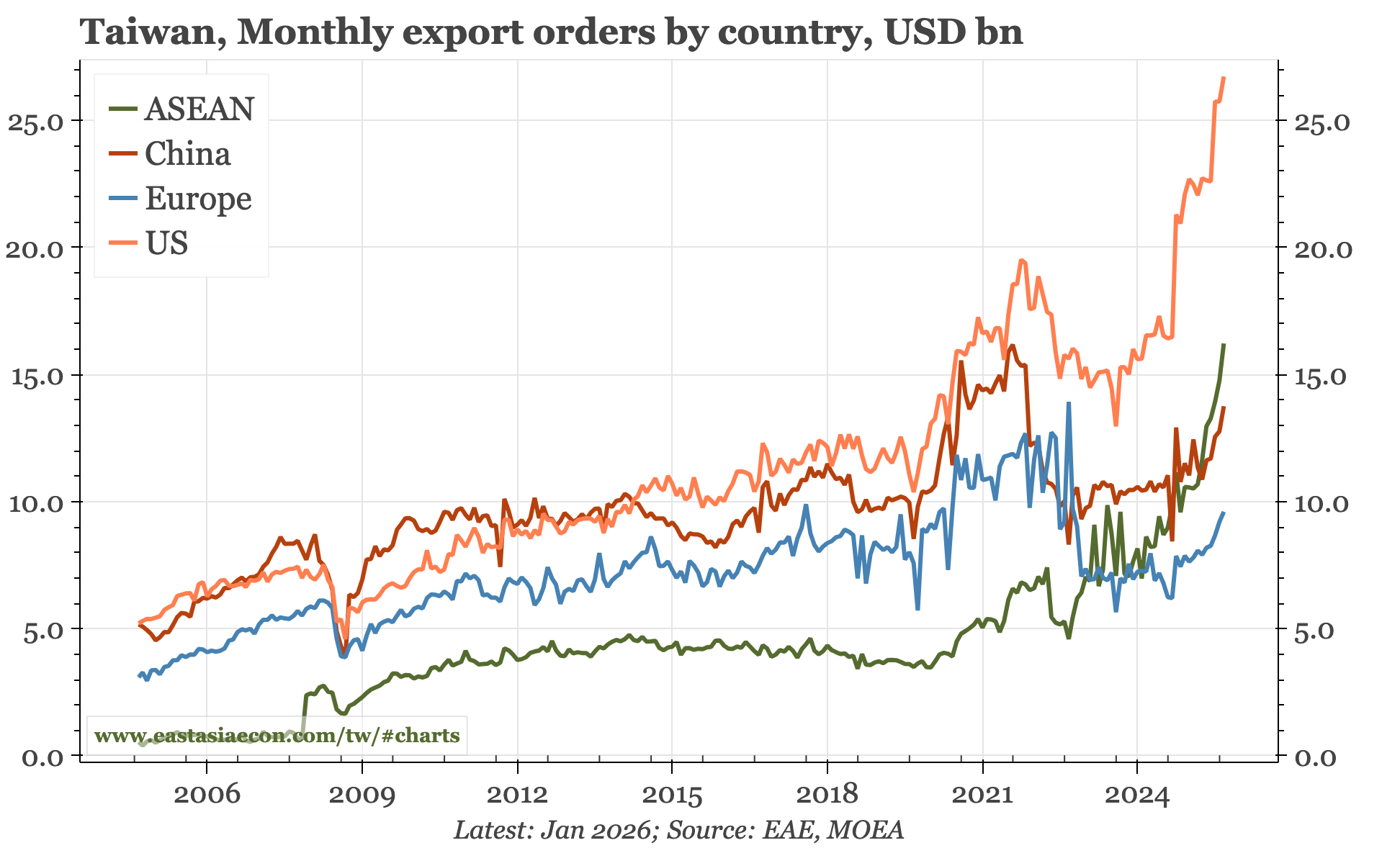

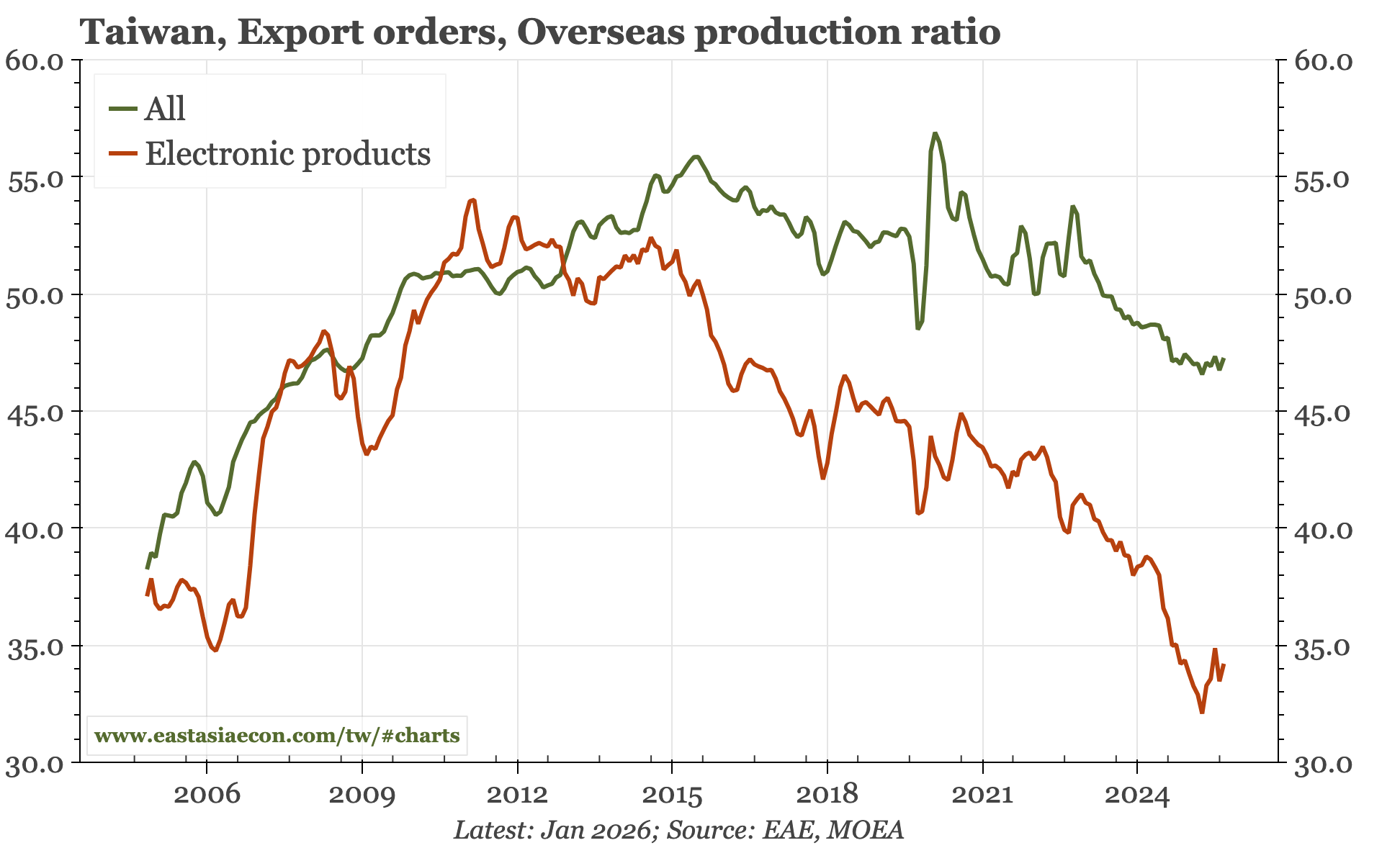

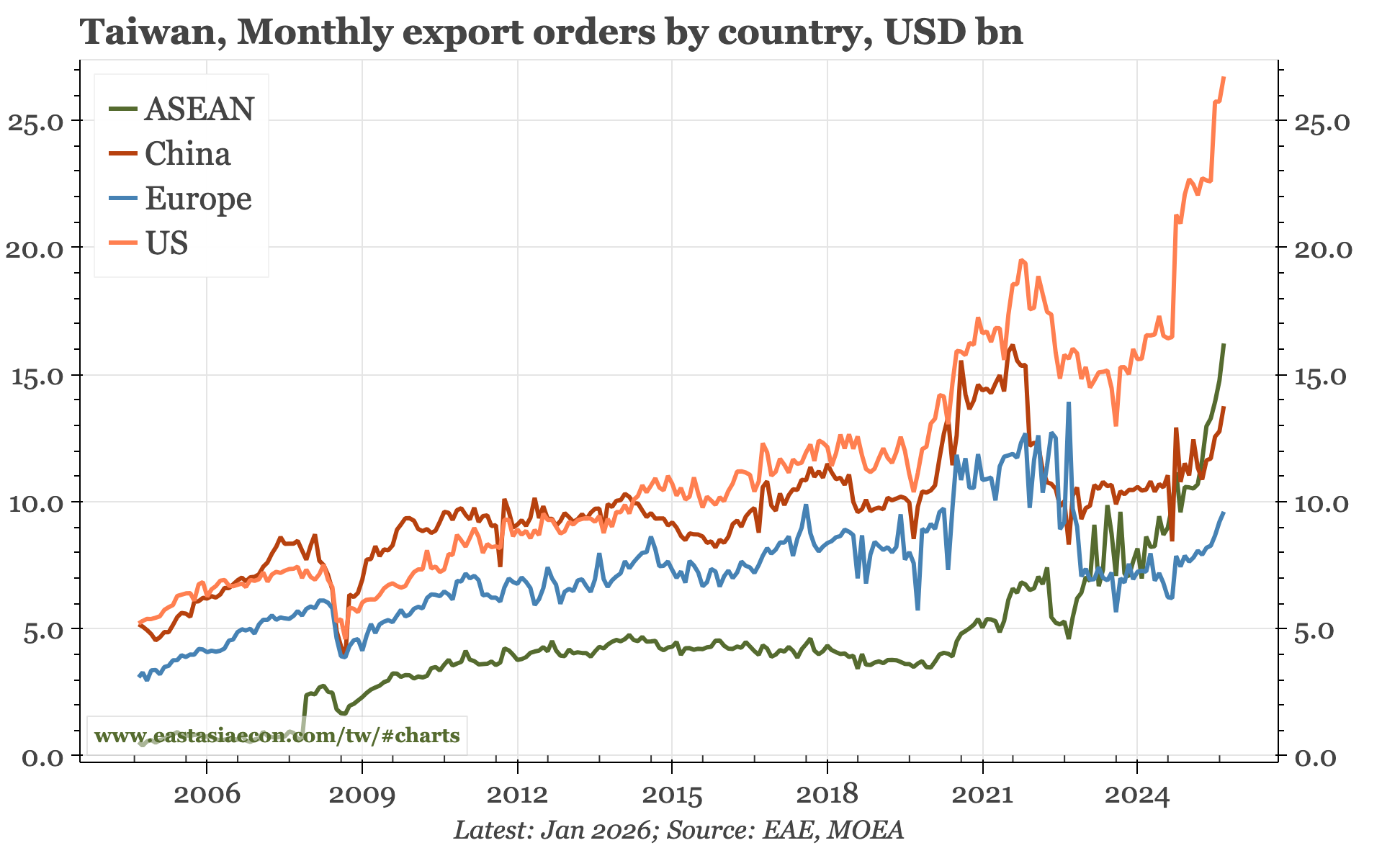

Growth in Taiwan export orders accelerated again in January to 60% YoY, the fastest in 15 years. Given the holiday, we need data for February to get a truer sense of underlying growth in exports. That said, it is interesting that orders from all regions grew. In particular, there is now some upwards momentum in exports from China for the first time since 2020.