East Asia Today

Highlights of a longer note reviewing cycle developments in Korea before the BOK meeting, and from a short analysis of today's profits release in China. Also, charts on today's other releases: business confidence in Korea, consumer confidence in Taiwan, and services PPI in Japan.

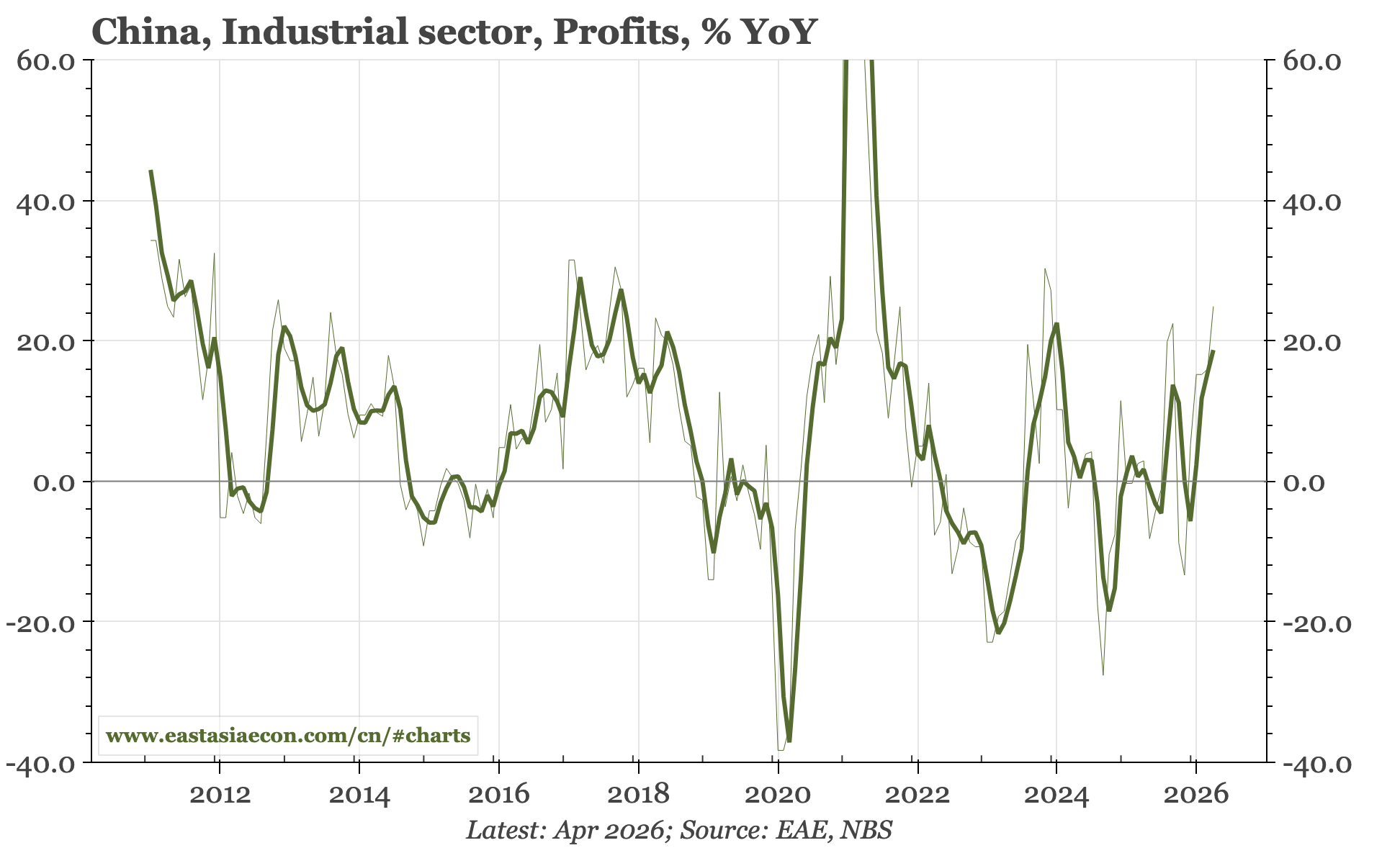

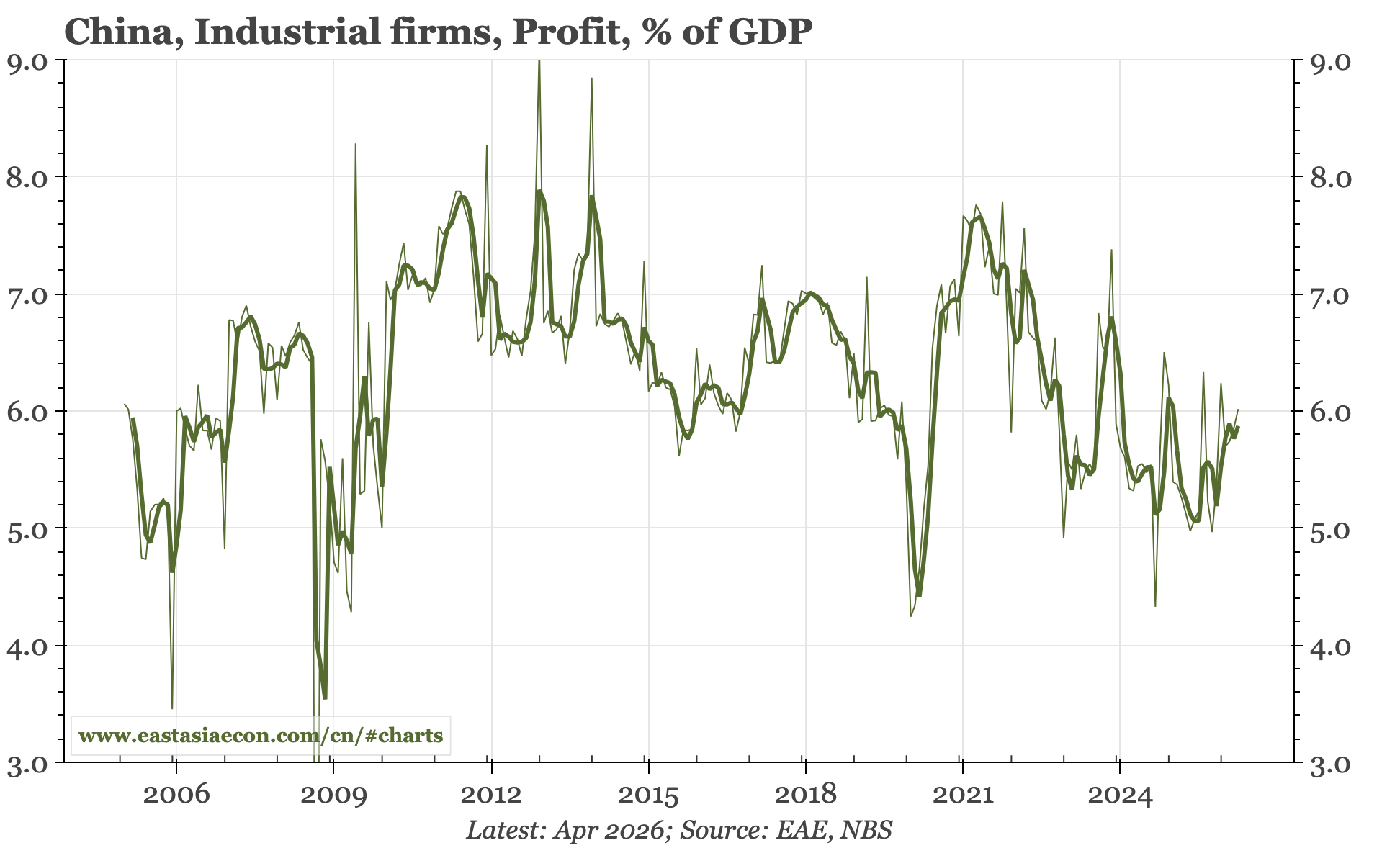

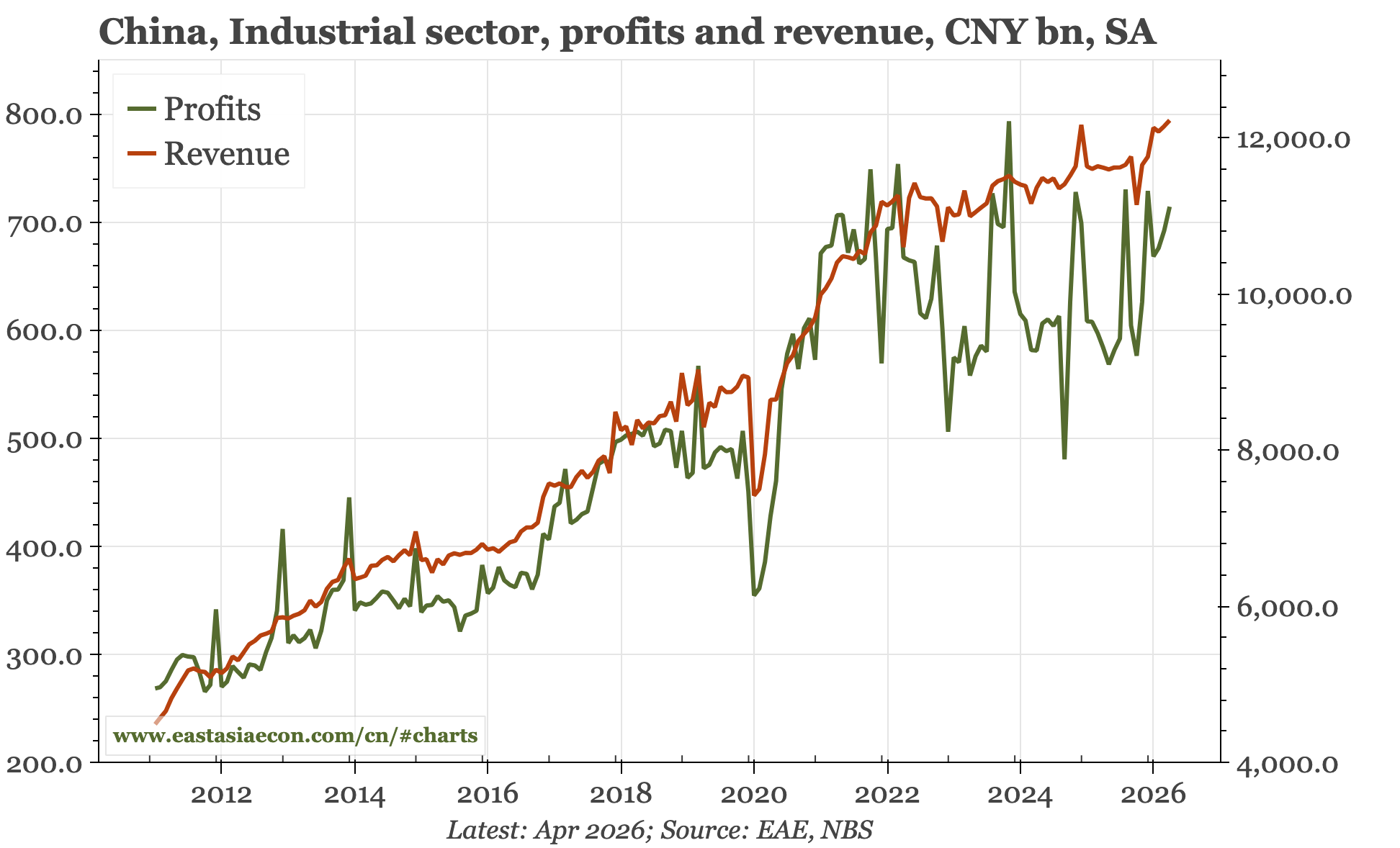

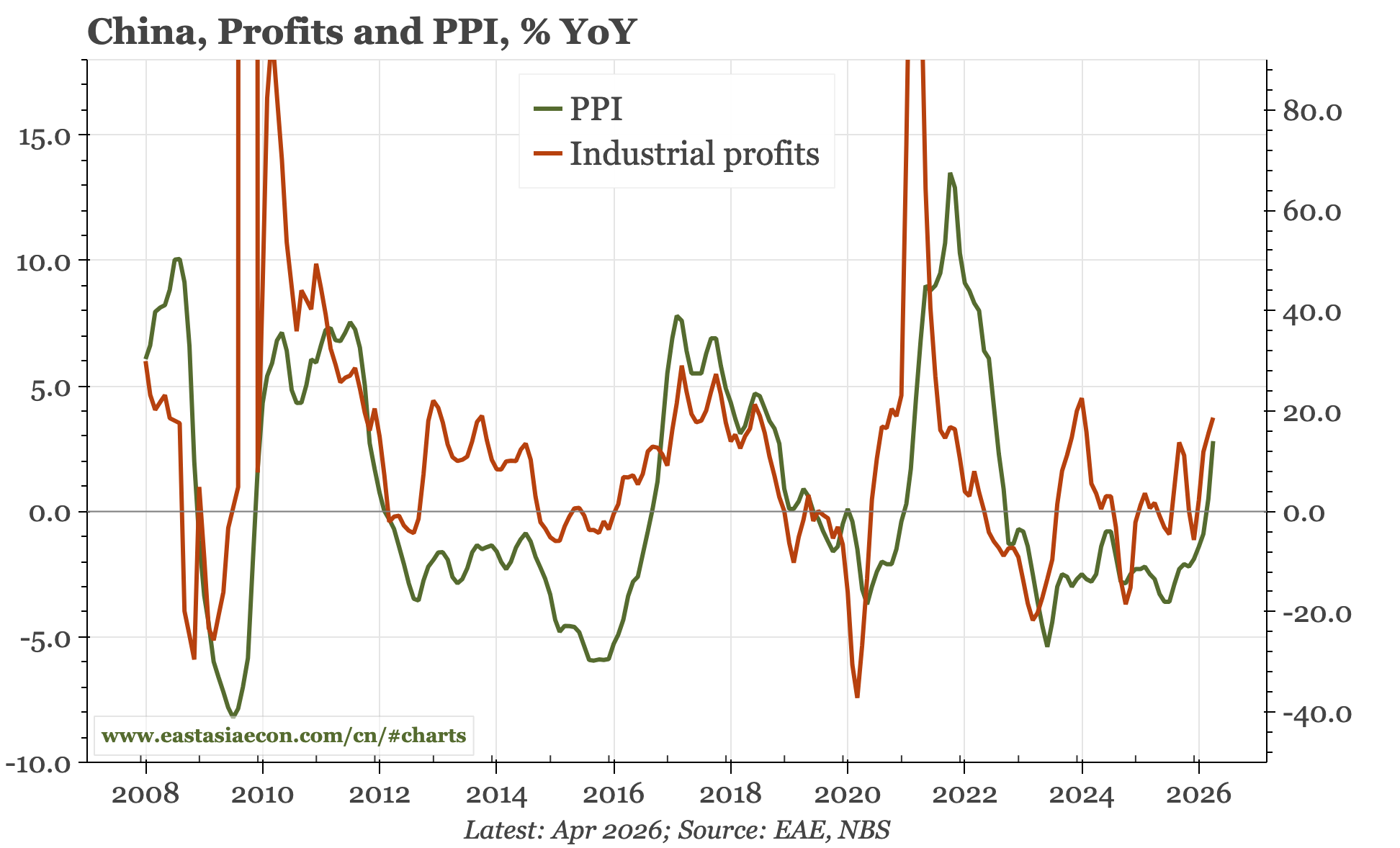

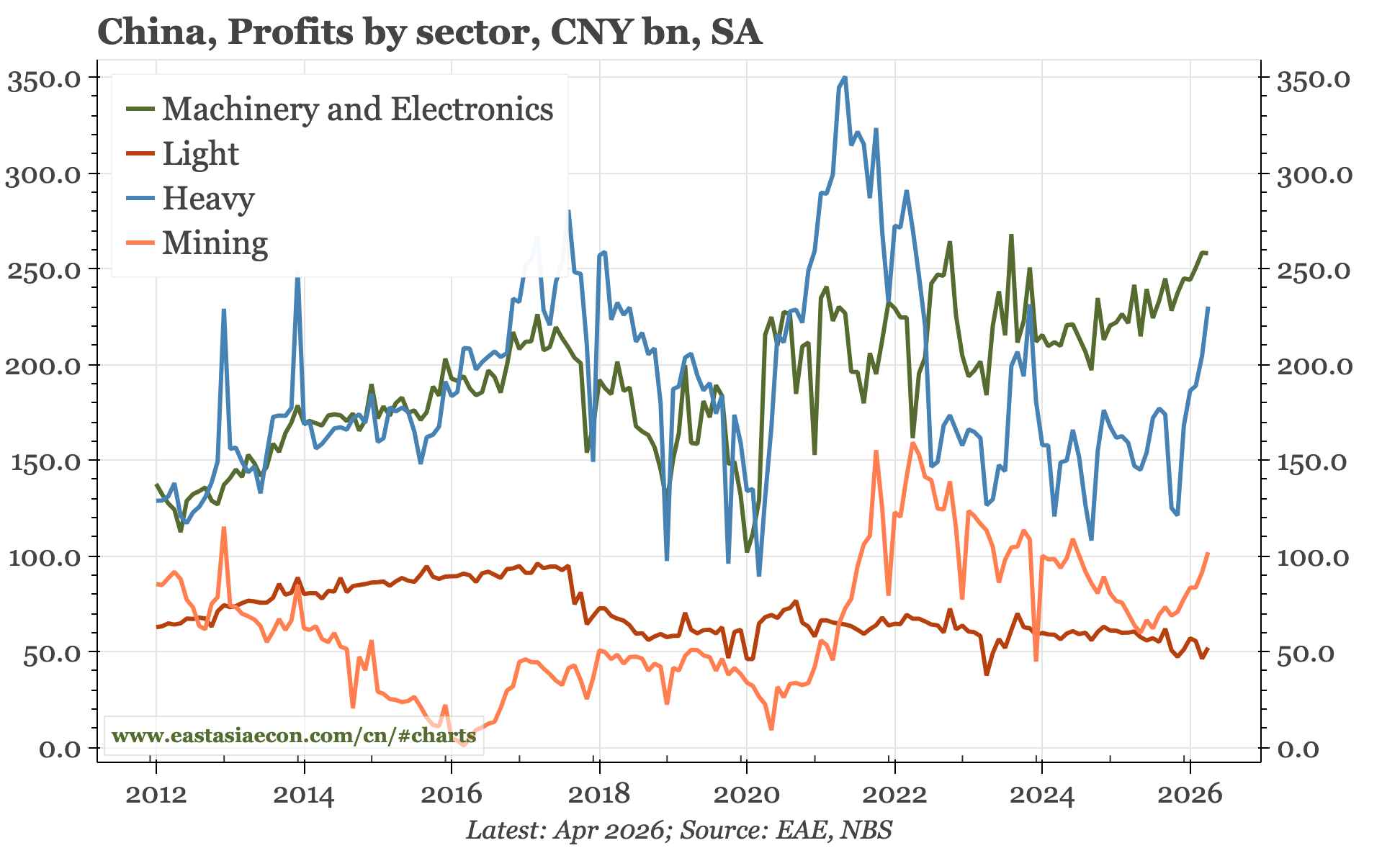

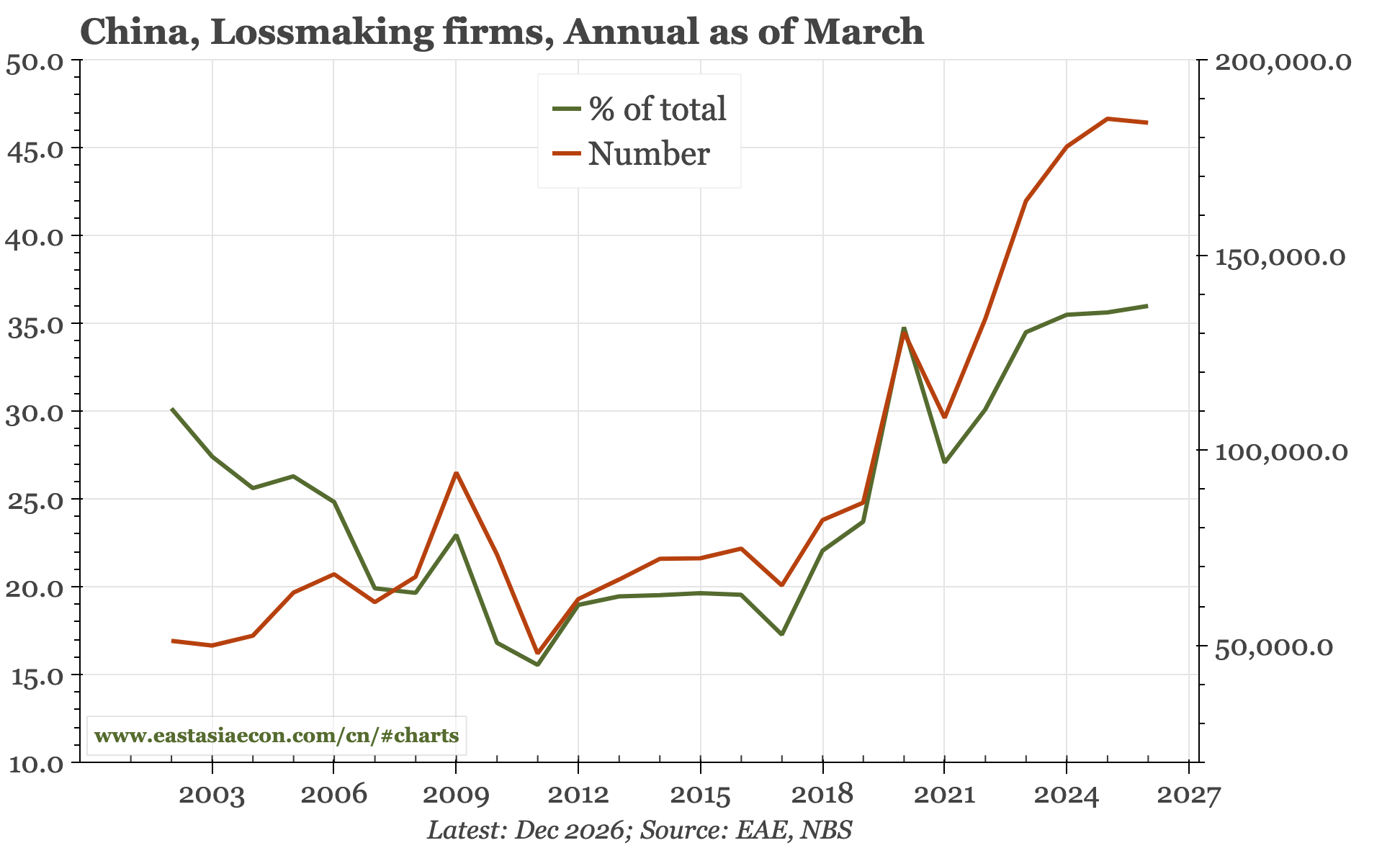

Cycle update – underlying profits a bit better. The bounce in headline profits in April was largely base effect, but there are signs of underlying improvement: revenues have started to rise, the increase in PPI is boosting profits in heavy industry, and hasn't yet derailed the post-2024 increase in total downstream manufacturing earnings.

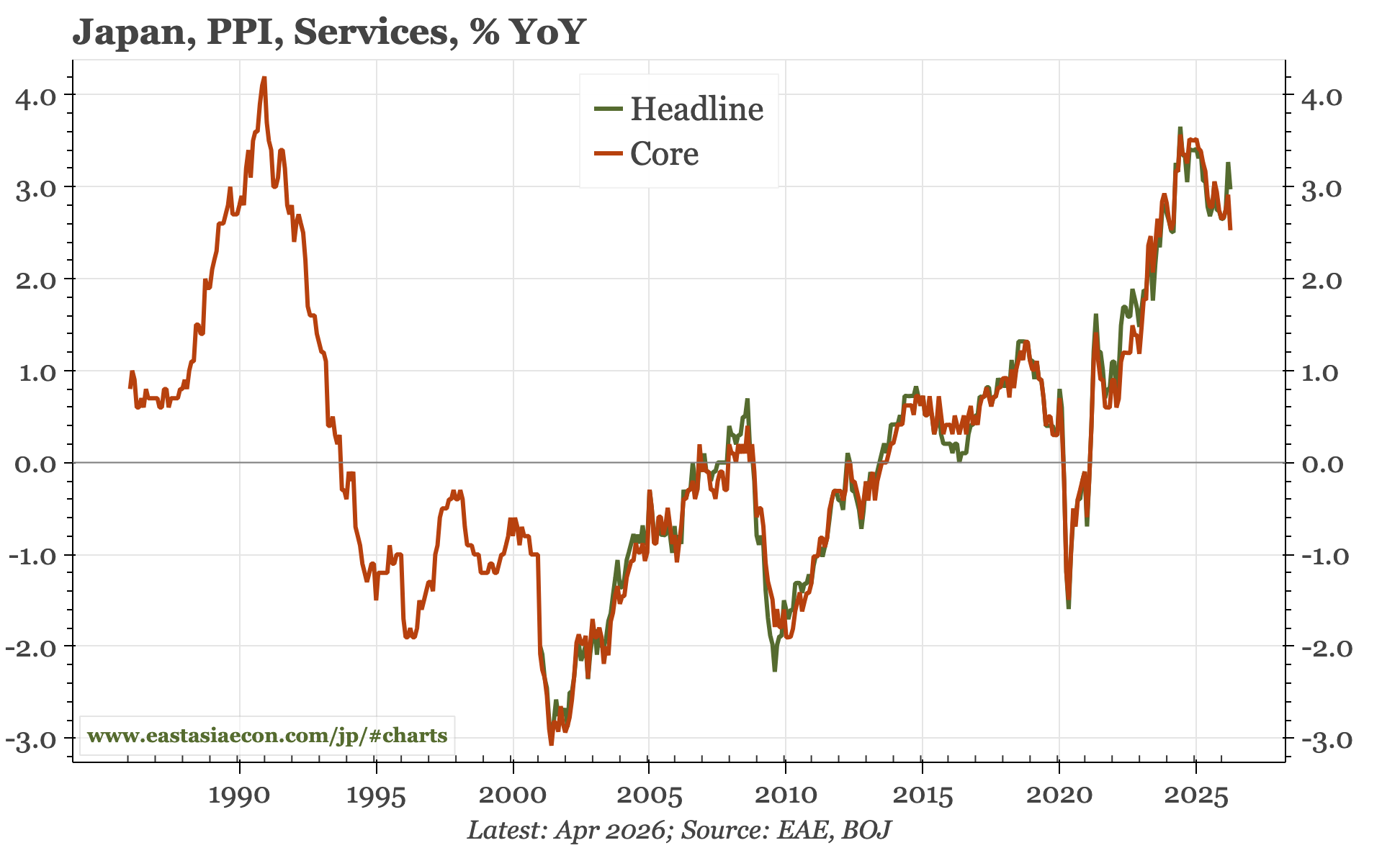

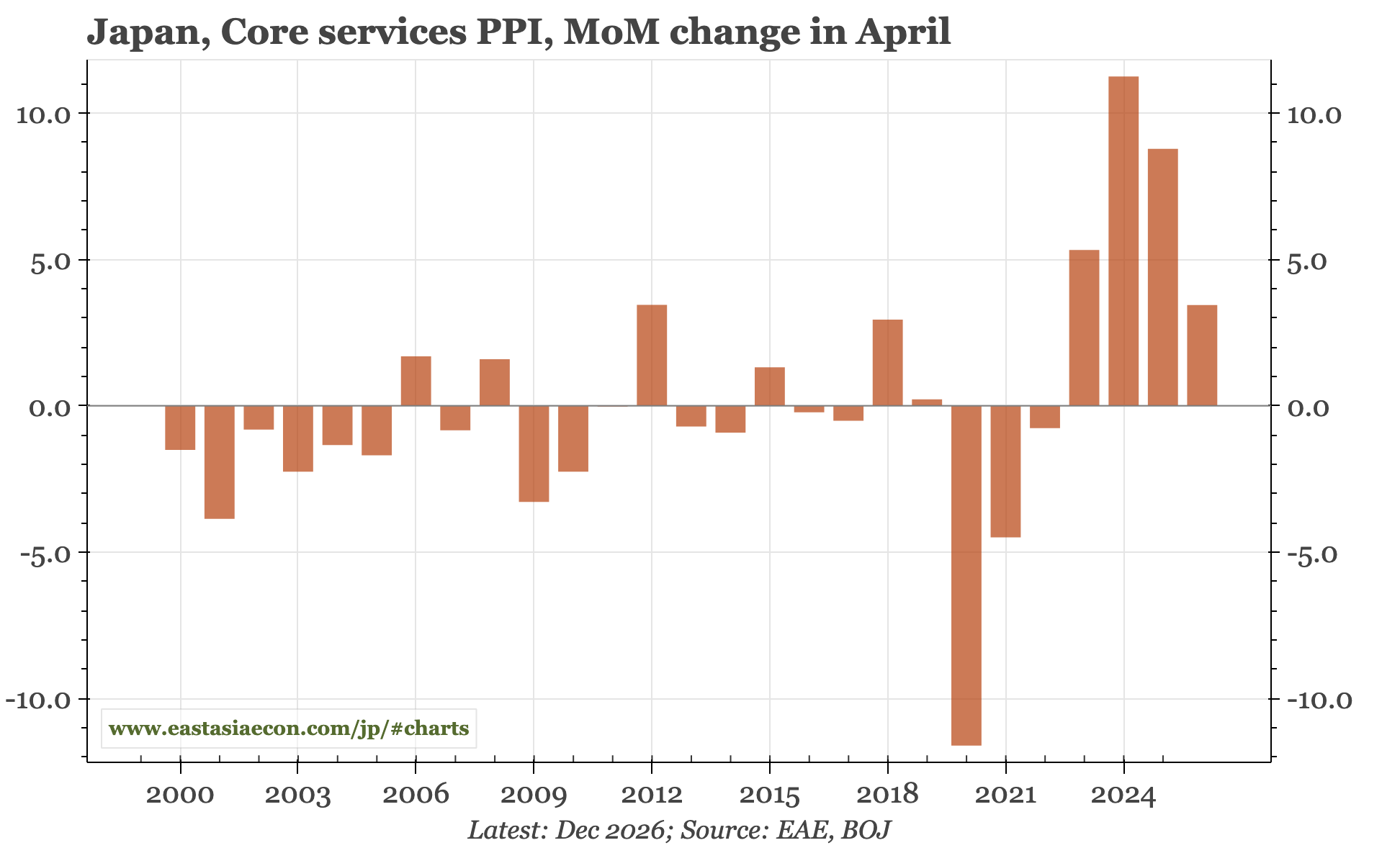

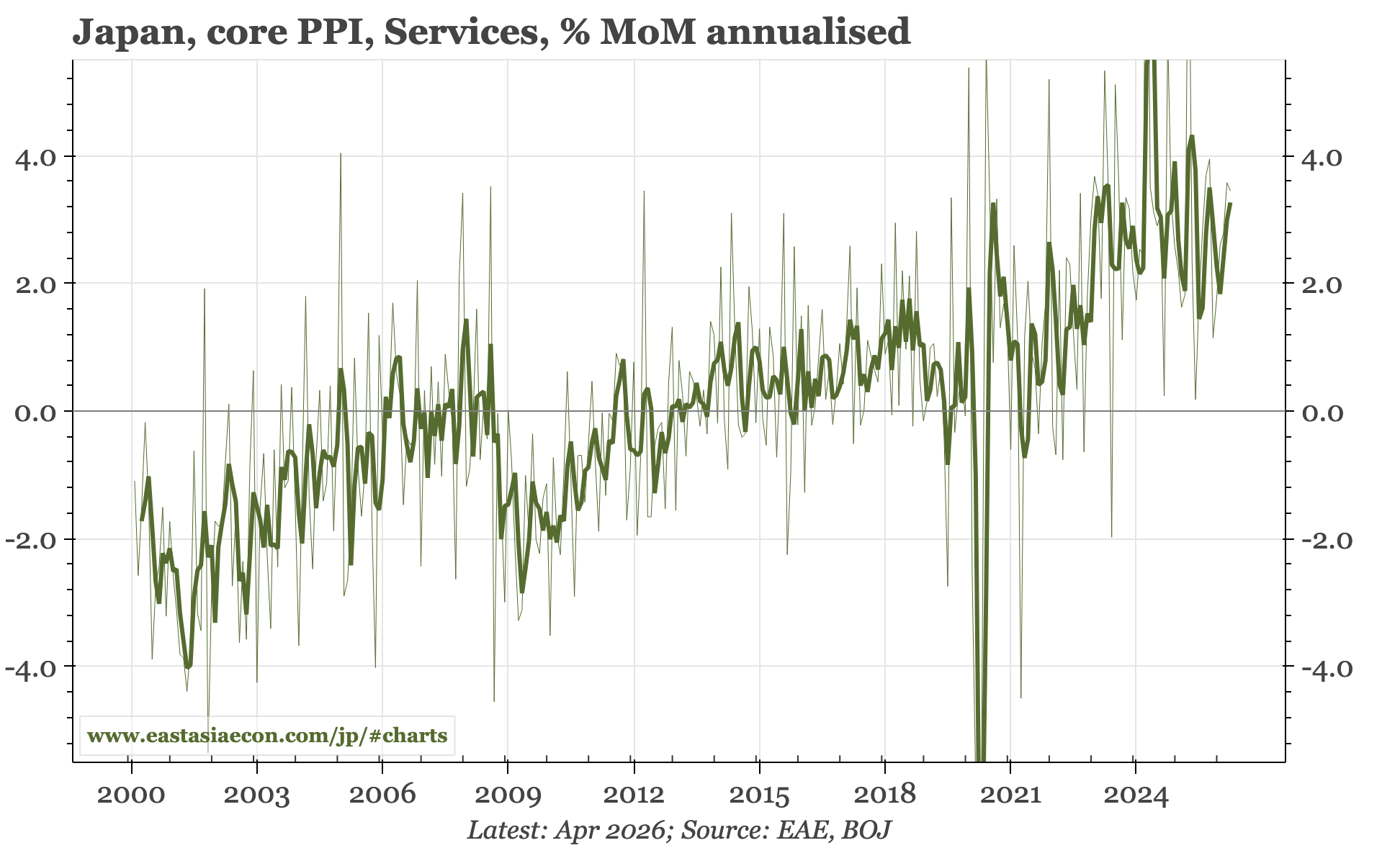

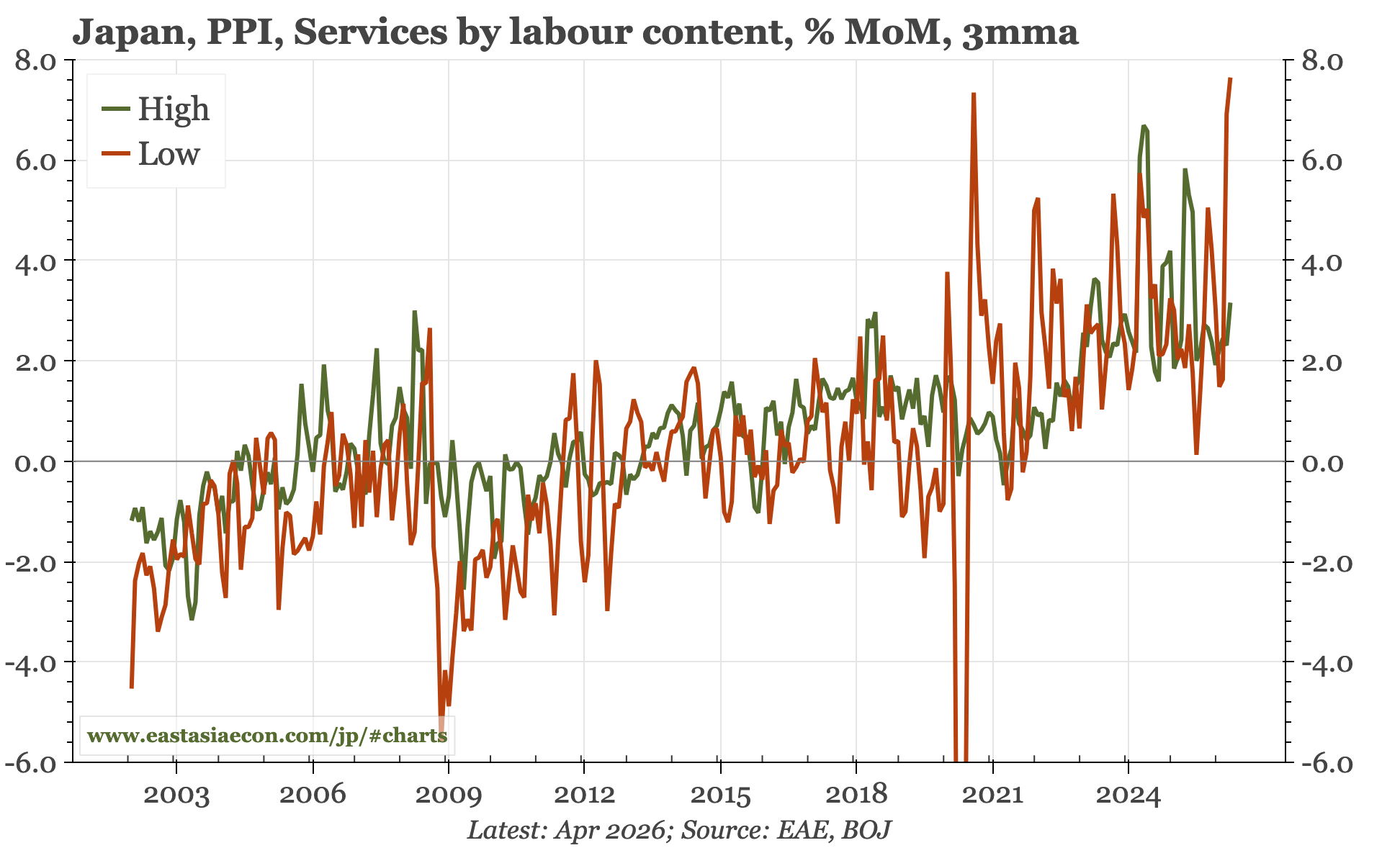

On a headline basis, core services PPI softened in April to 2.5% YoY, the lowest since early 2024. However, on a sequential basis the inflation rate isn't now slowing, and seems to have settled in a 2-3% range. That is also true for inflation in sectors with high labour intensity, an indicator which is important for the BOJ.

If you aren't yet a subscriber, please consider becoming one! This daily product is designed for individuals, but we also have data services and a much more comprehensive offering for financial institutions. If you have any questions or feedback, please get in touch with me directly.

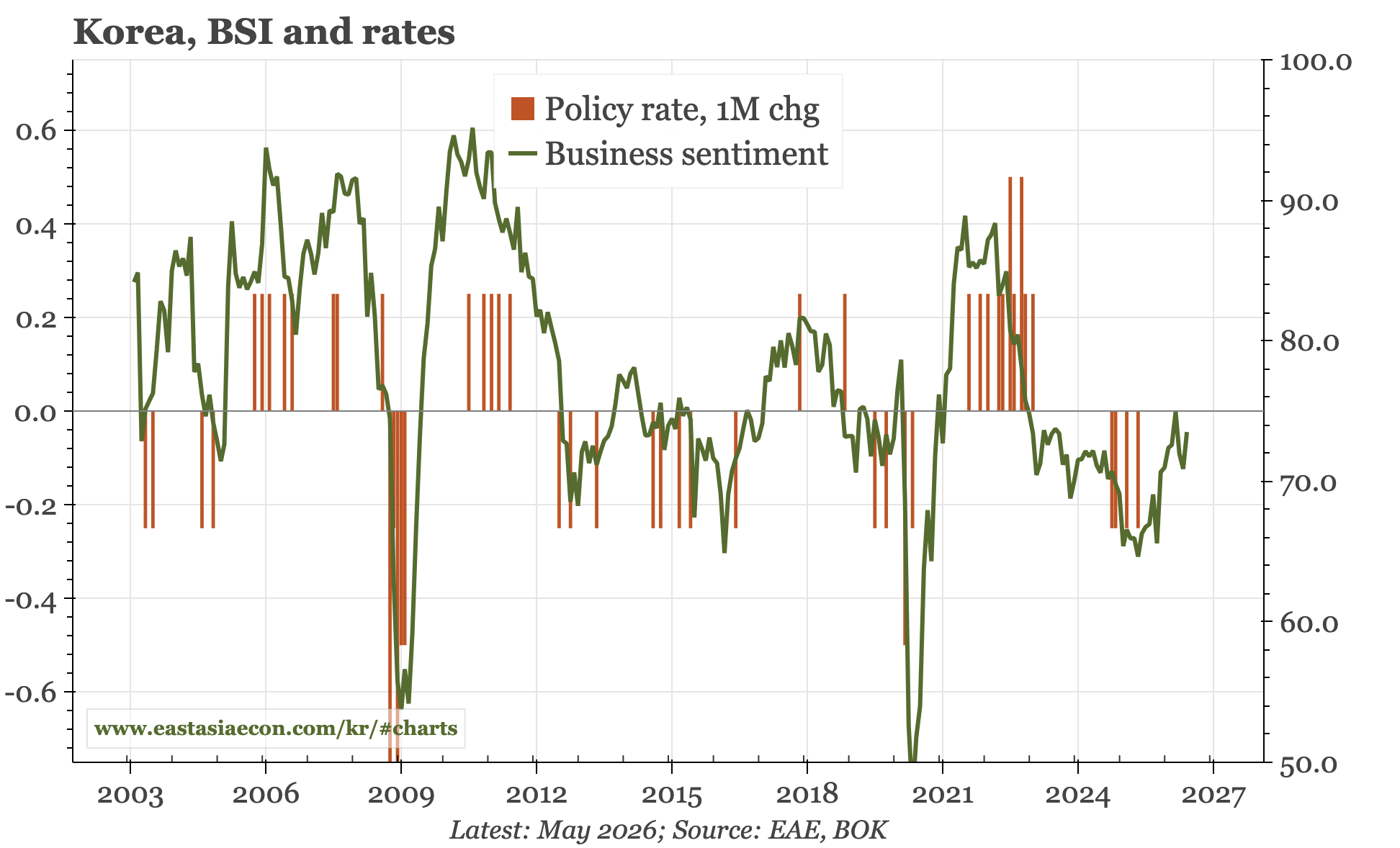

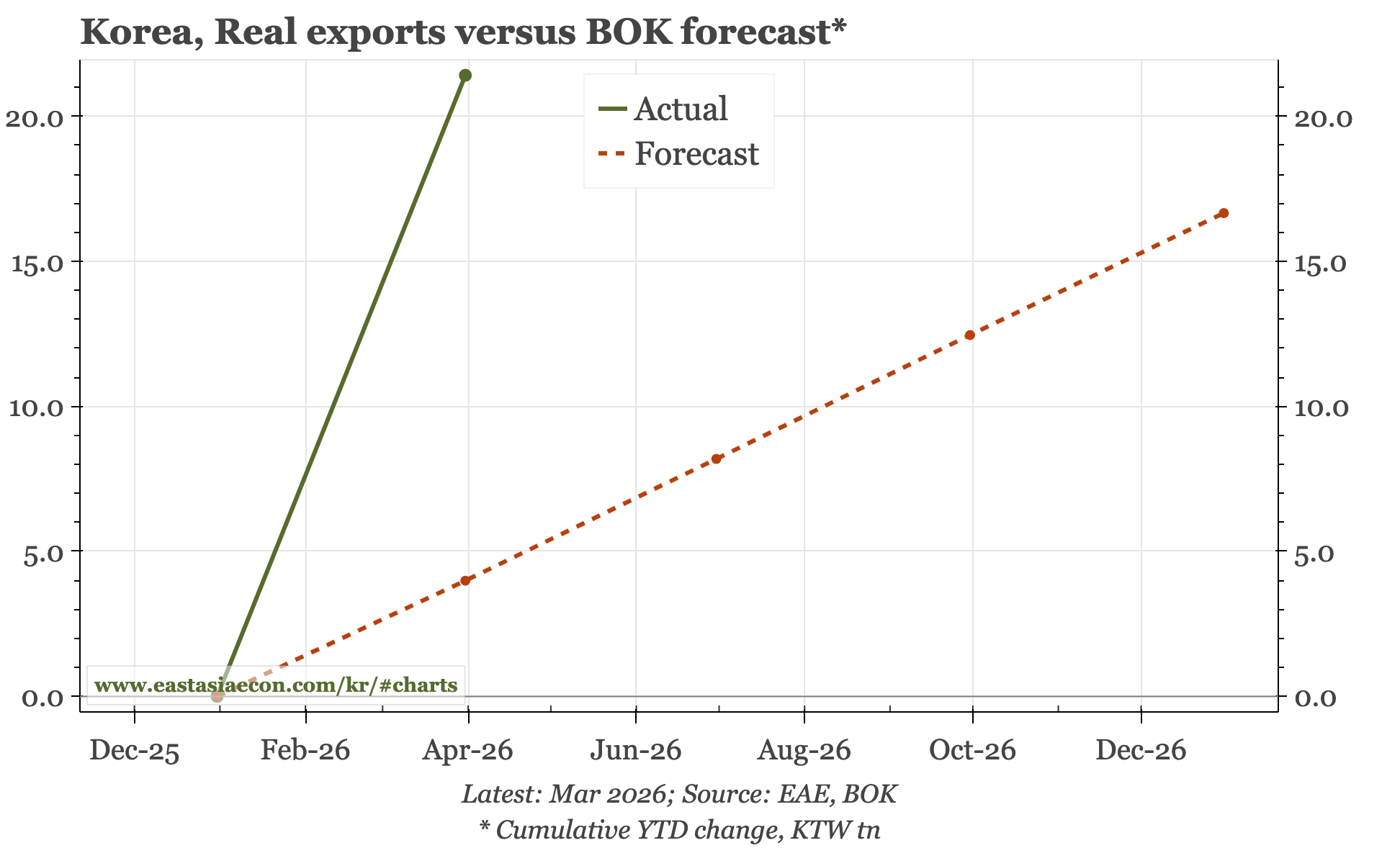

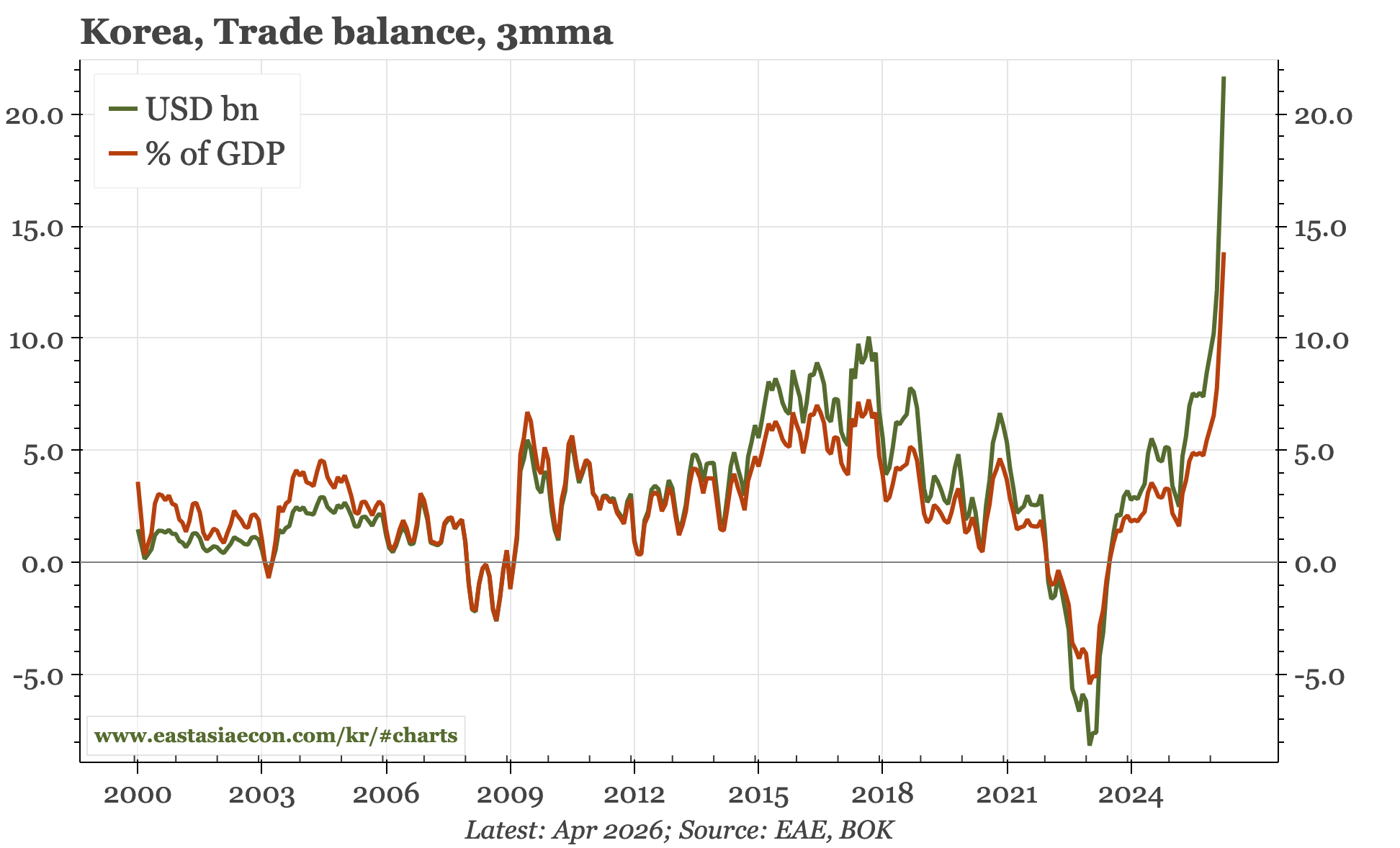

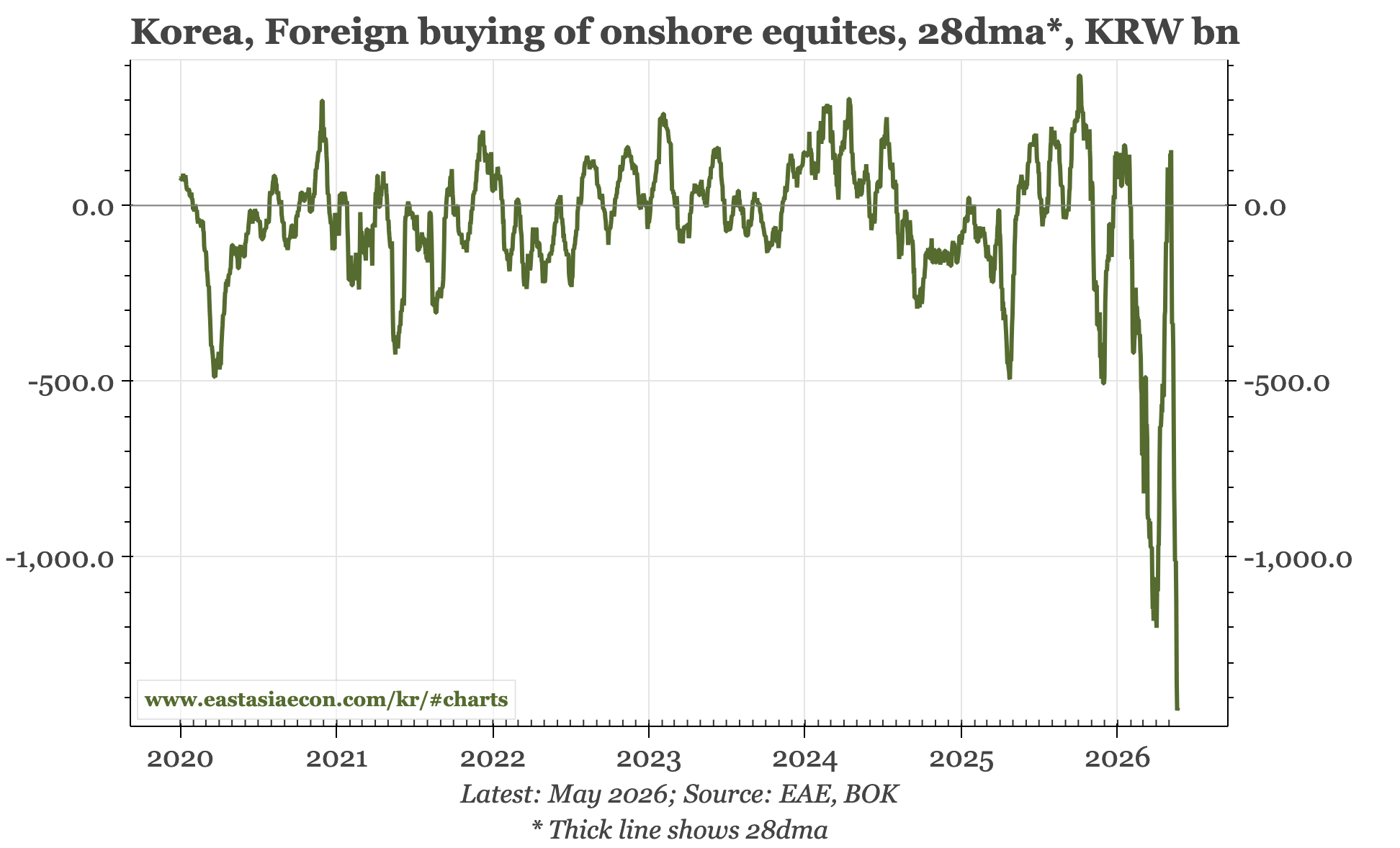

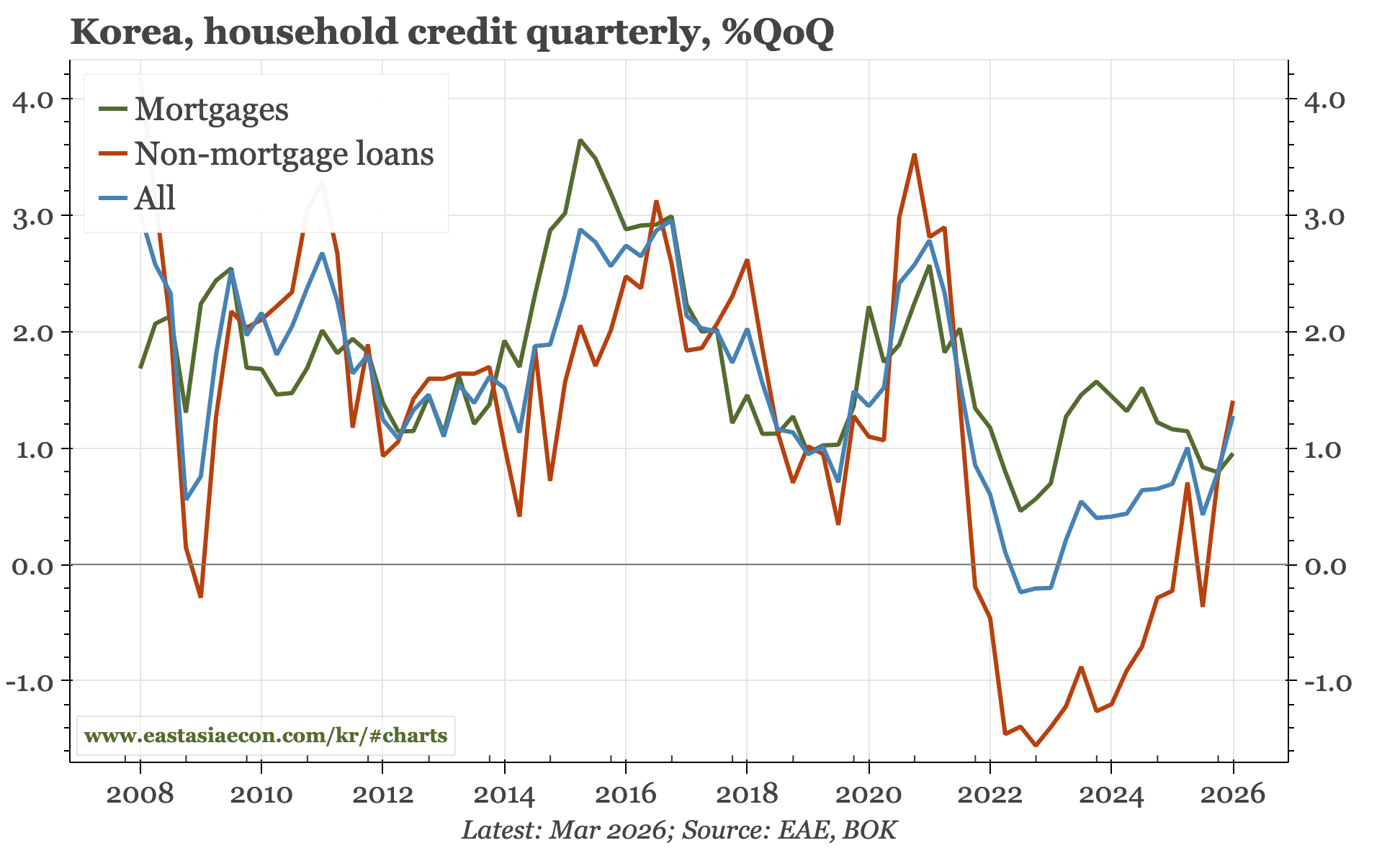

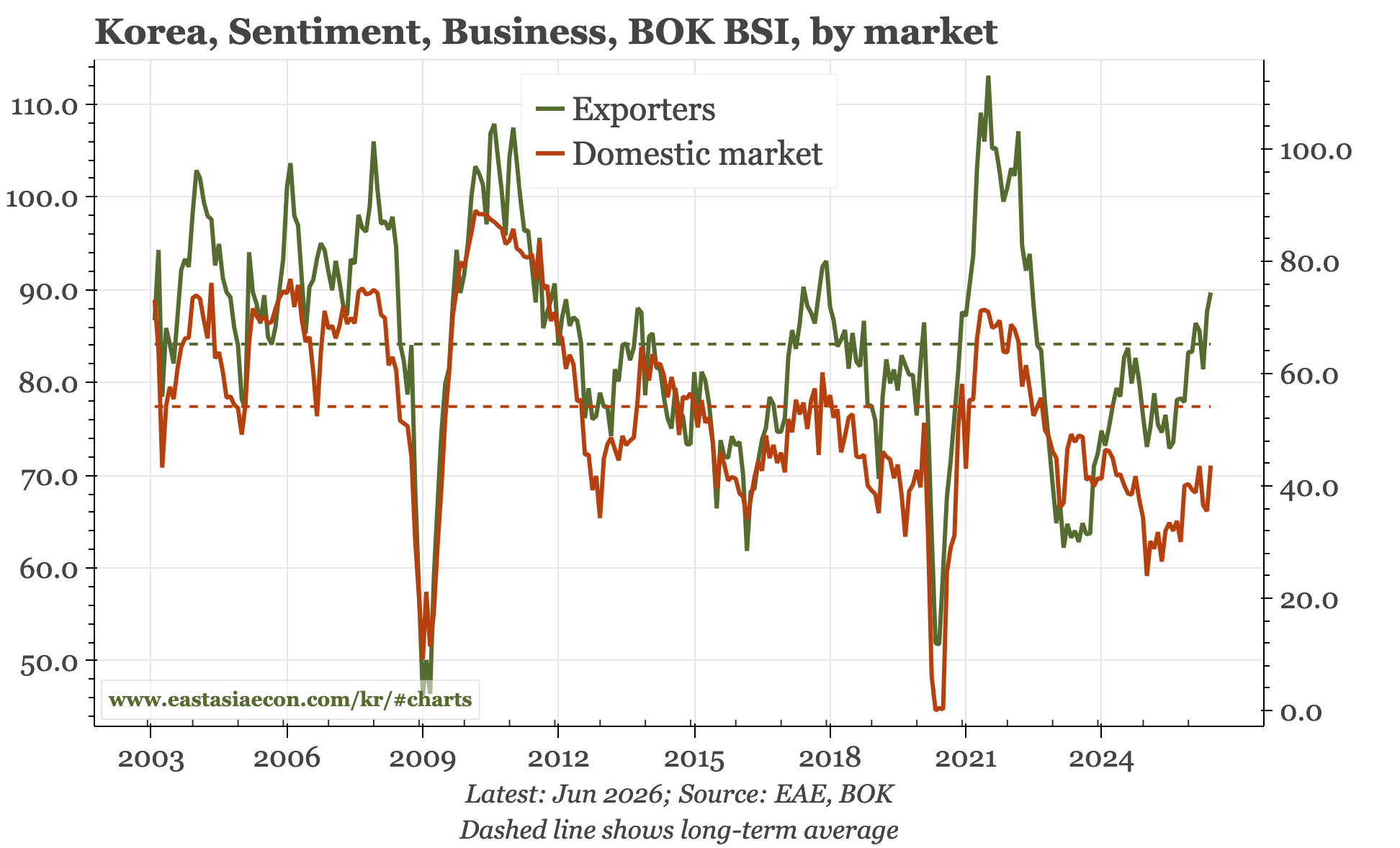

Taking stock – ticking four boxes for a hike. The BOK's main considerations for policy are growth, inflation, KRW and housing. Three were already pointing to hikes, and tomorrow the bank is likely to raise expected growth above potential too. That makes a rate hike likely. The risk is it still just a bit too early.

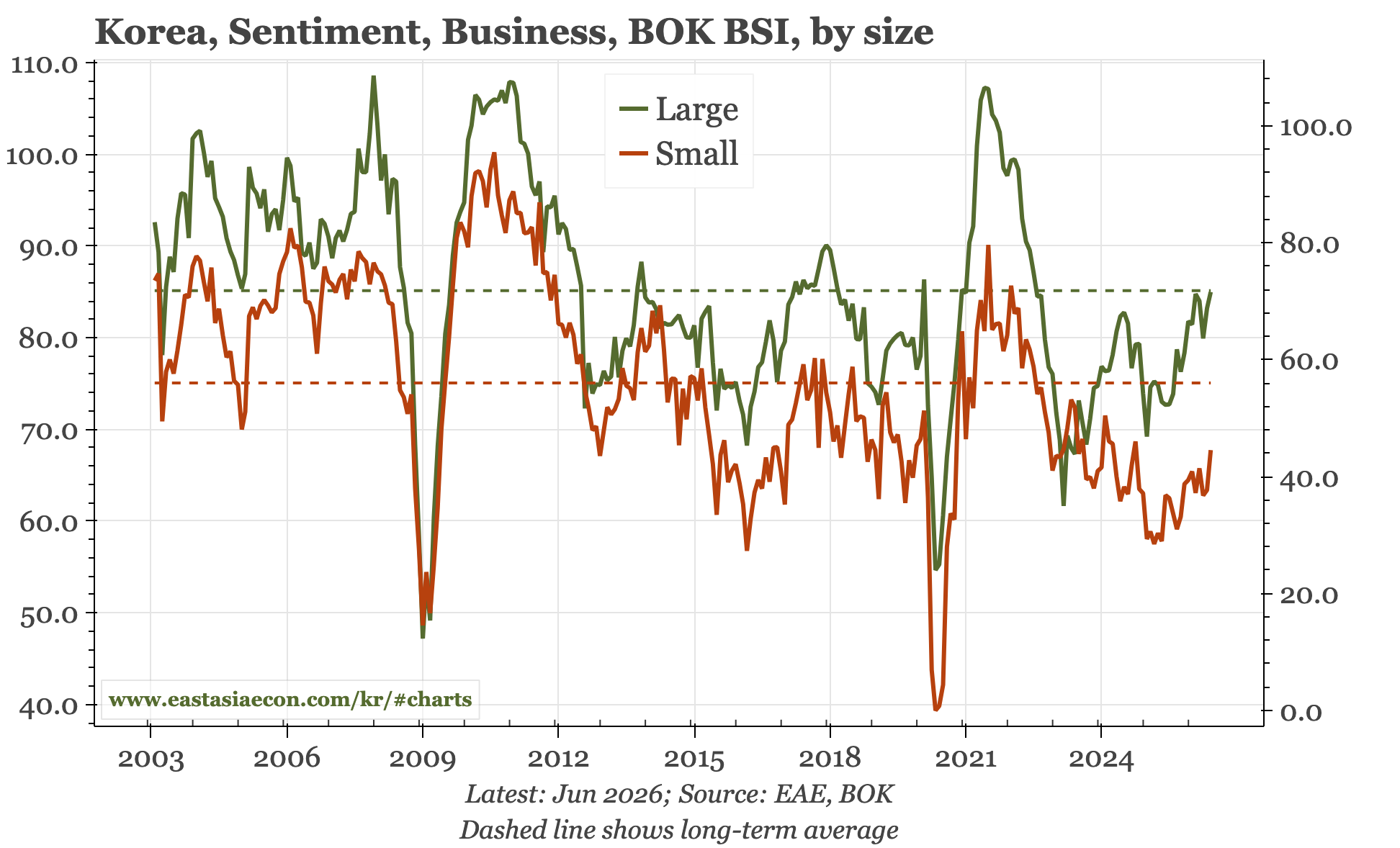

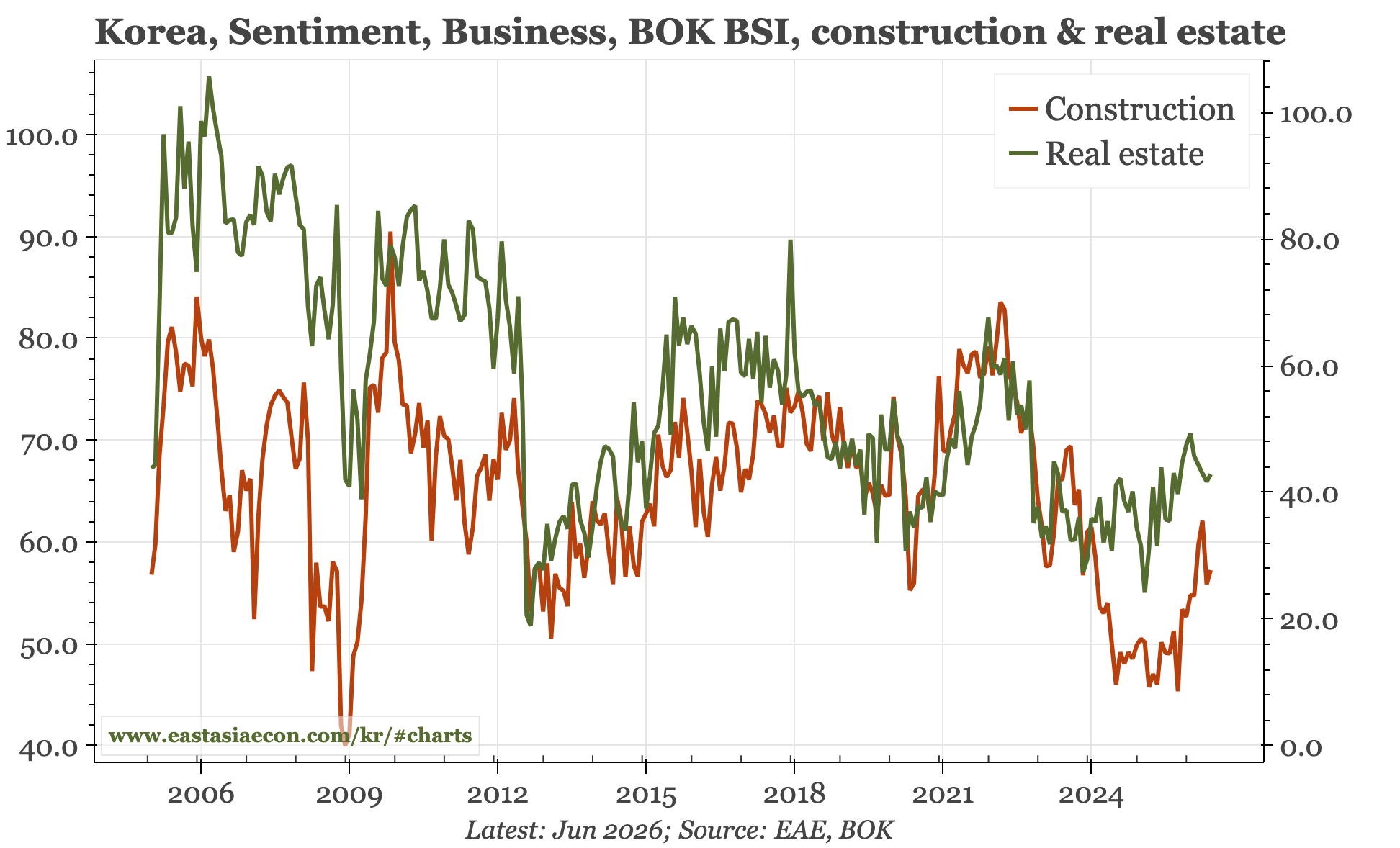

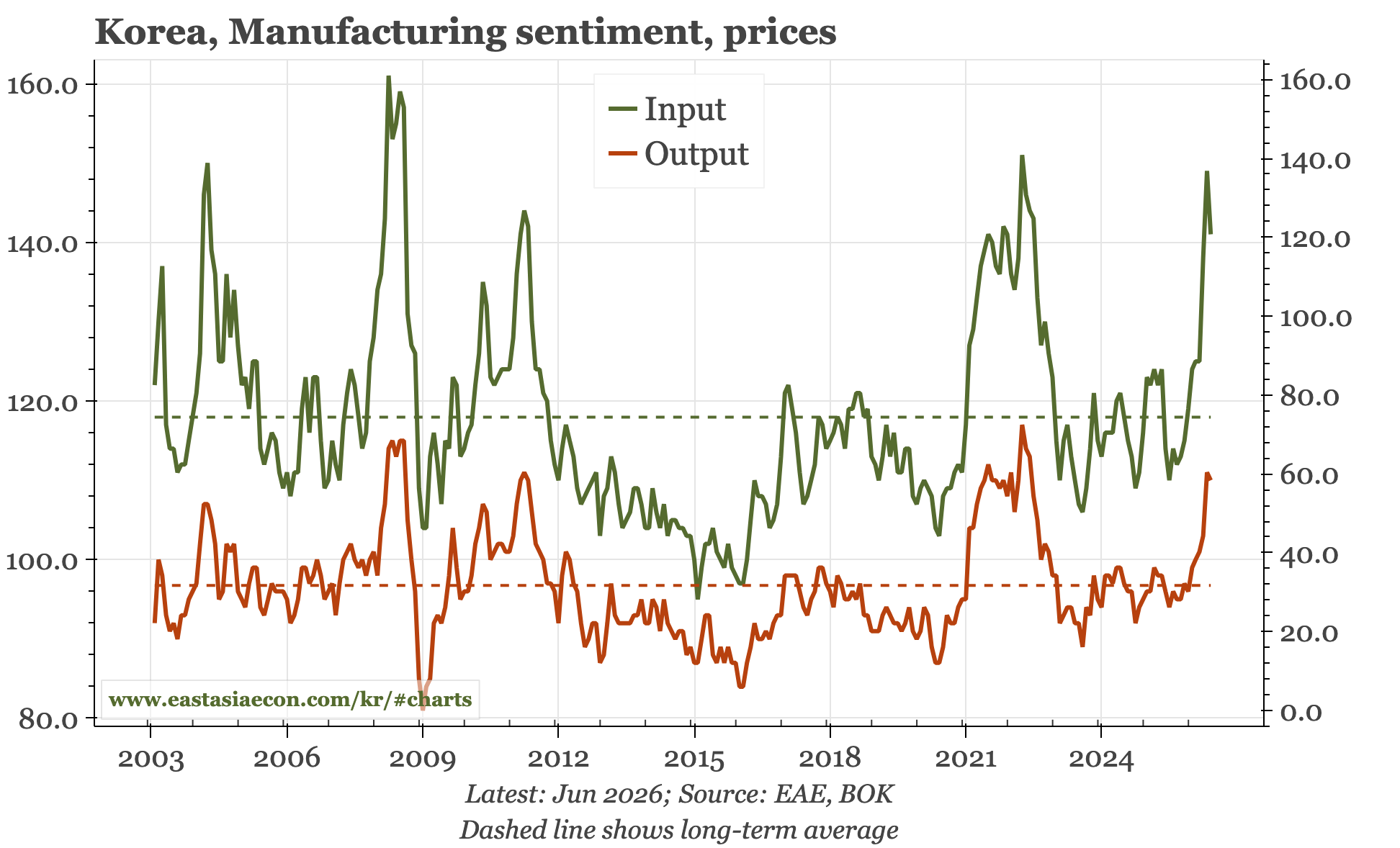

The upgrade to growth would come on the back of strong exports, and today's business sentiment survey showed another improvement in exporter confidence to well above the historical average through June. Domestic sentiment remains weaker, though there has been a clear bottoming out of the construction sector. Both input and output prices in manufacturing remain high, but didn't increase further.

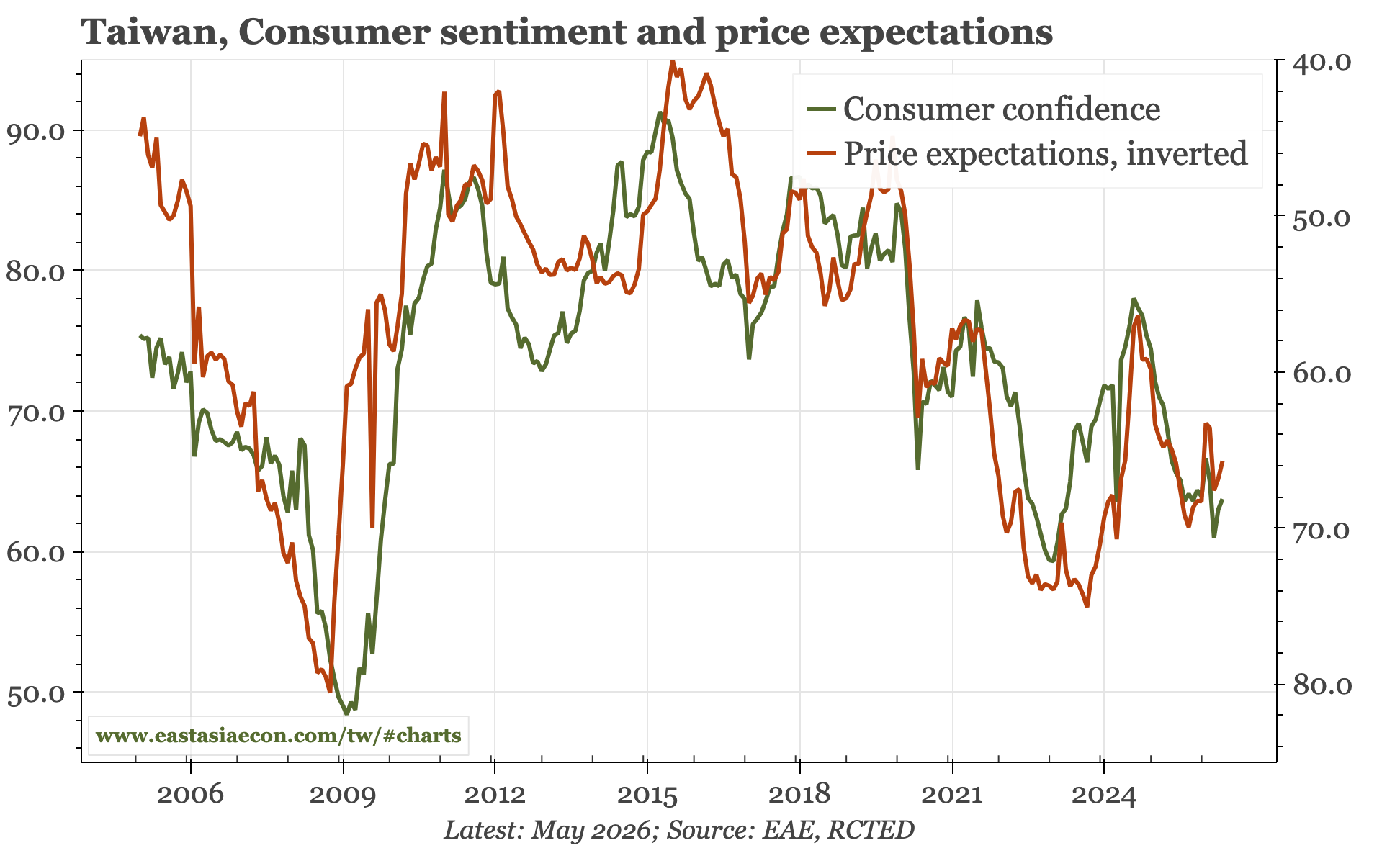

Today's consumer survey in Taiwan also showed a mild softening of the recent increase in inflationary pressure, and that helped support an equally mild rise in consumer sentiment. That still leaves consumer confidence down YoY. While that does warn of softer consumer spending, the relationship between confidence and actual consumption hasn't been particularly tight.