East Asia Today

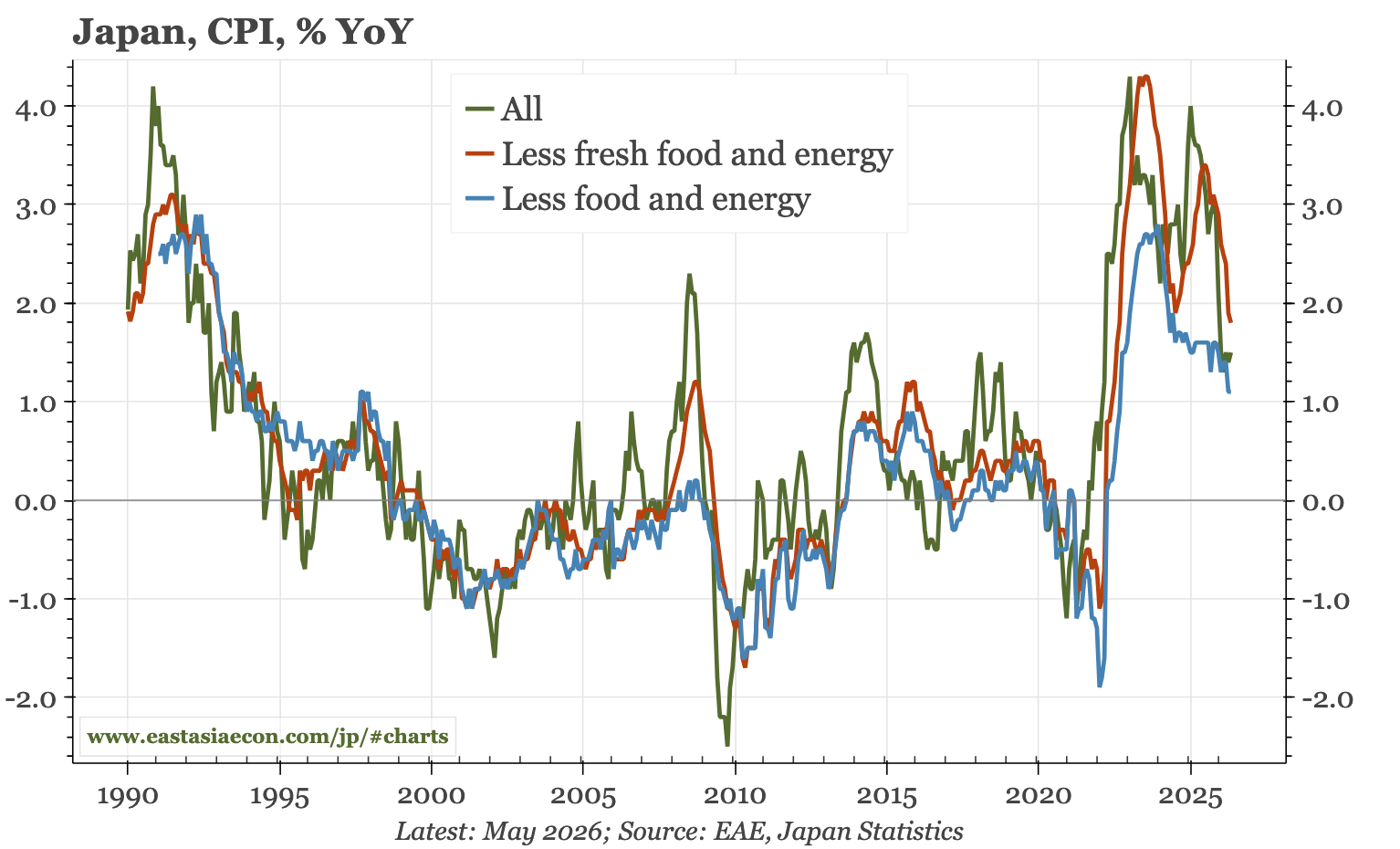

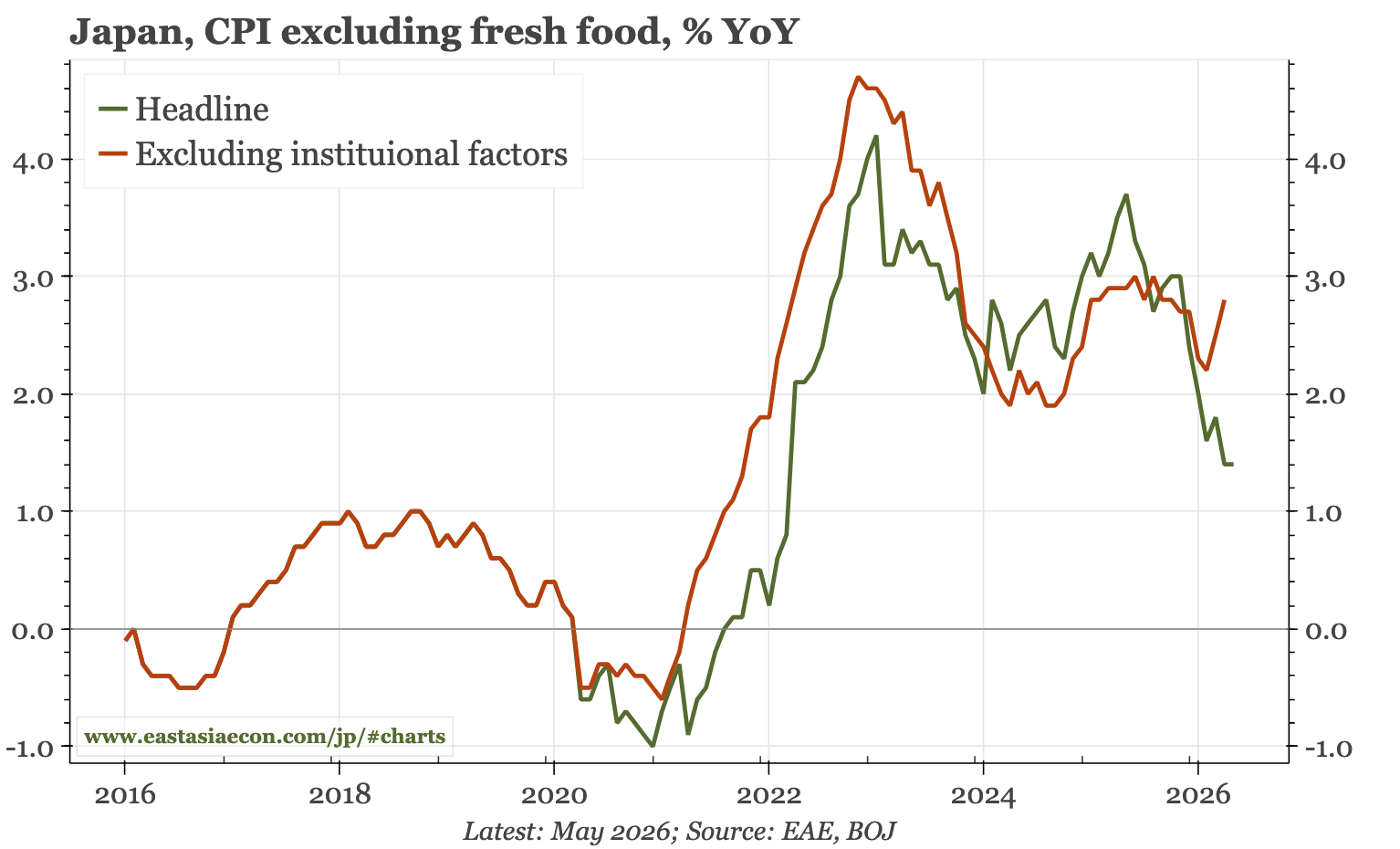

A new video laying out my argument for stabilisation in China. In terms of the data flow, Japan's inflation was modest in May, but that was because of subsidies, and further JPY depreciation will push up prices again. Korean PPI inflation accelerated, with the jump most obvious in services.

Thematic – is (it still possible) the worst is over? My latest video, making the case for a bottoming of China's economy. In light of this week's poor official data, the argument might look off-base, which means it should at least be interesting. I do think the logic holds up, but as discussed here, there are reasons I could be wrong.

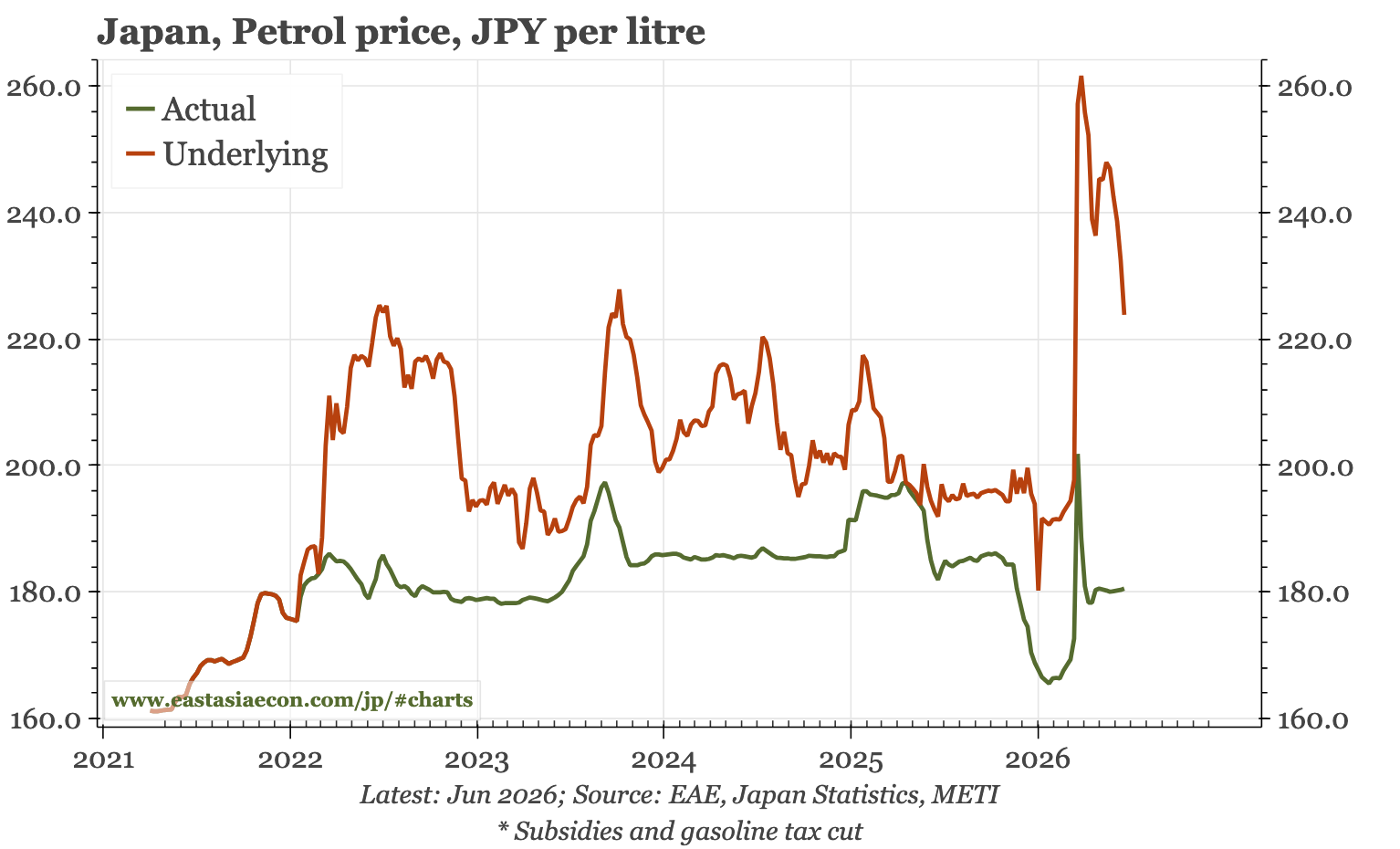

On official measures, inflation remains modest. But the numbers are being dragged down by subsidies from the government. The big one is the ceiling on the pump price, which means consumers won't see much direct benefit from the fall in global oil prices. The decline in energy prices will help the government's budget, though some of that boost will be taken away if official intervention doesn't prevent the JPY's permanent break though 160 and the currency depreciates yet further.

If you aren't yet a subscriber, please consider becoming one! This daily product is designed for individuals, but we also have data services and a much more comprehensive offering for financial institutions. If you have any questions or feedback, please get in touch with me directly.

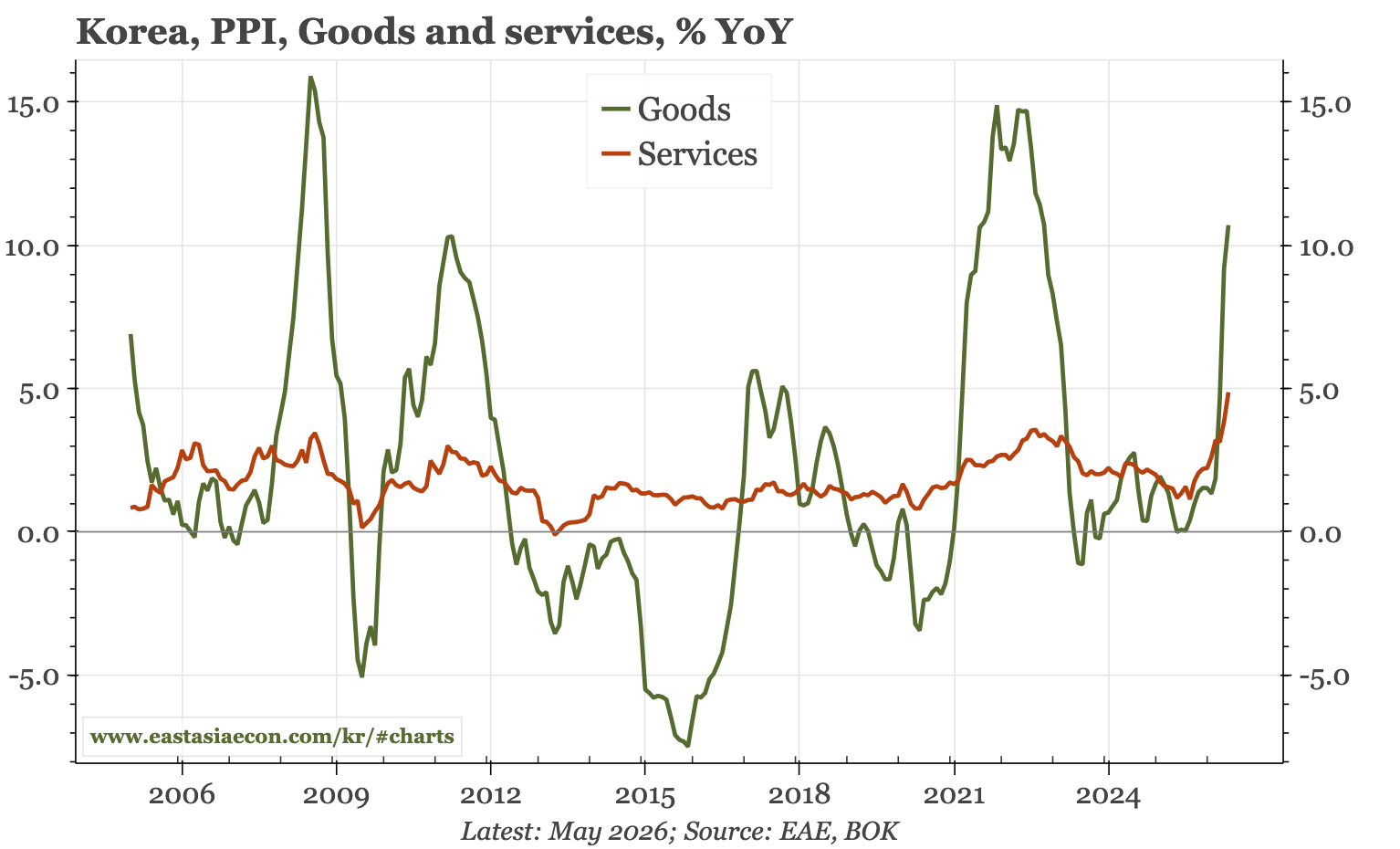

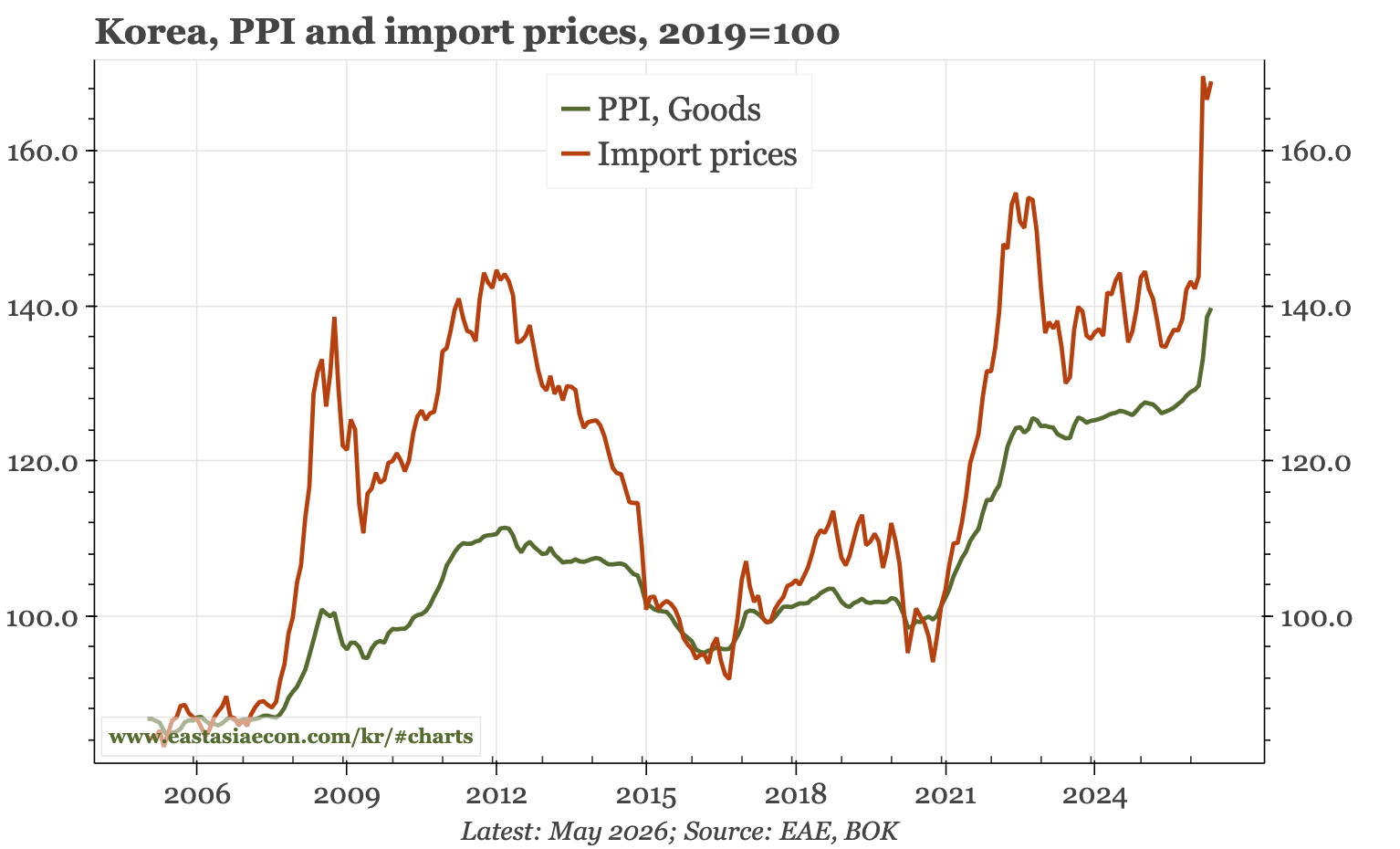

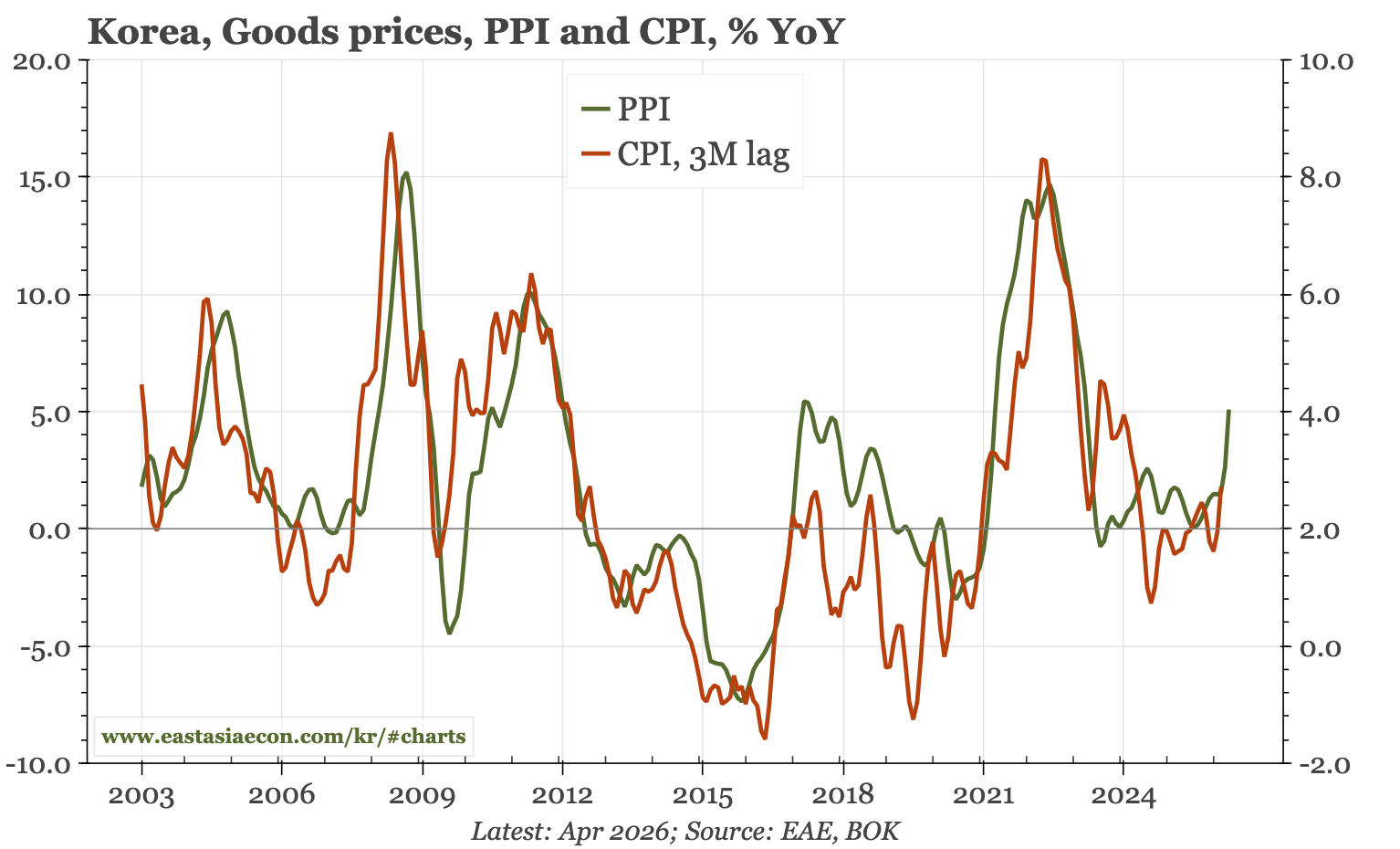

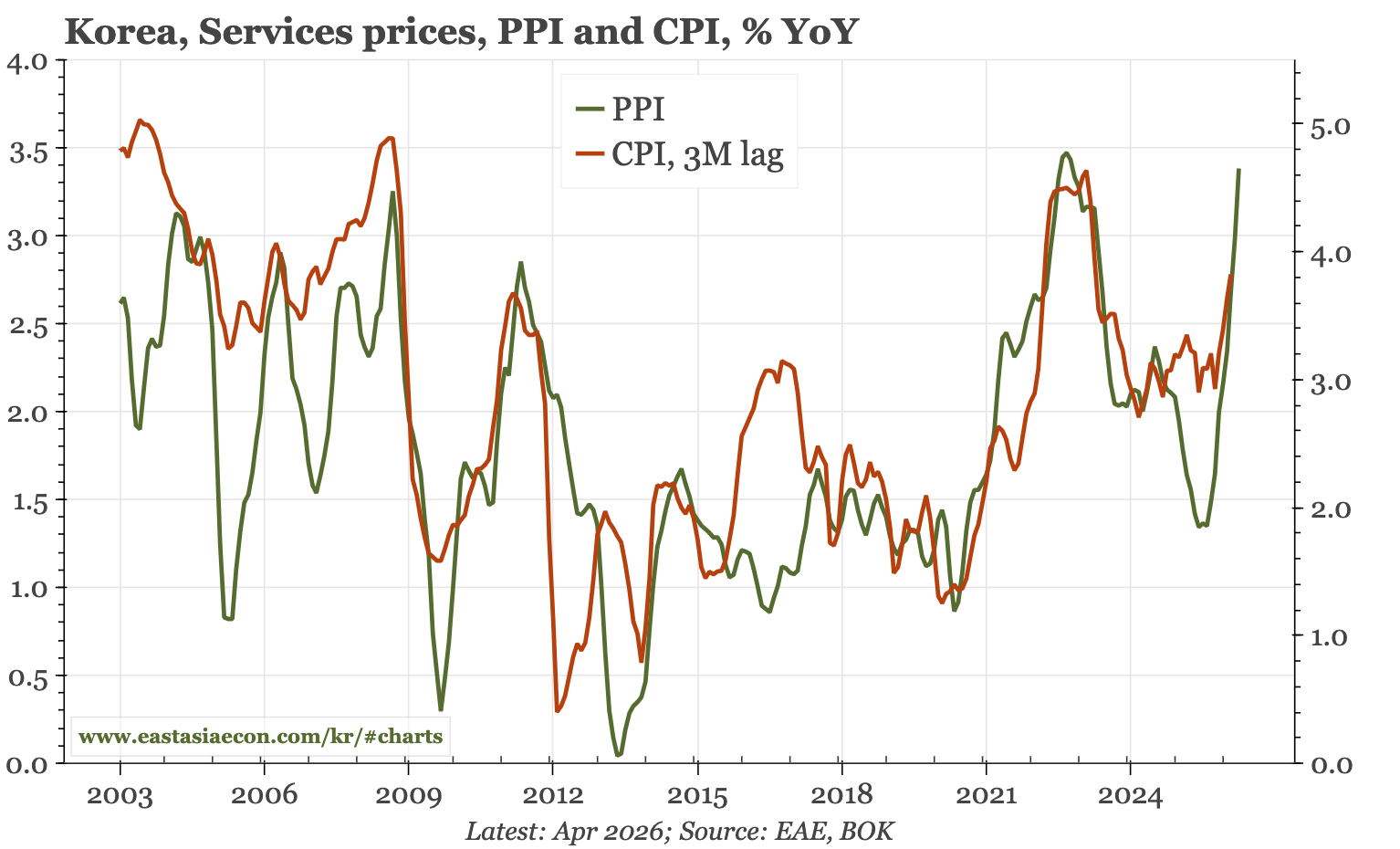

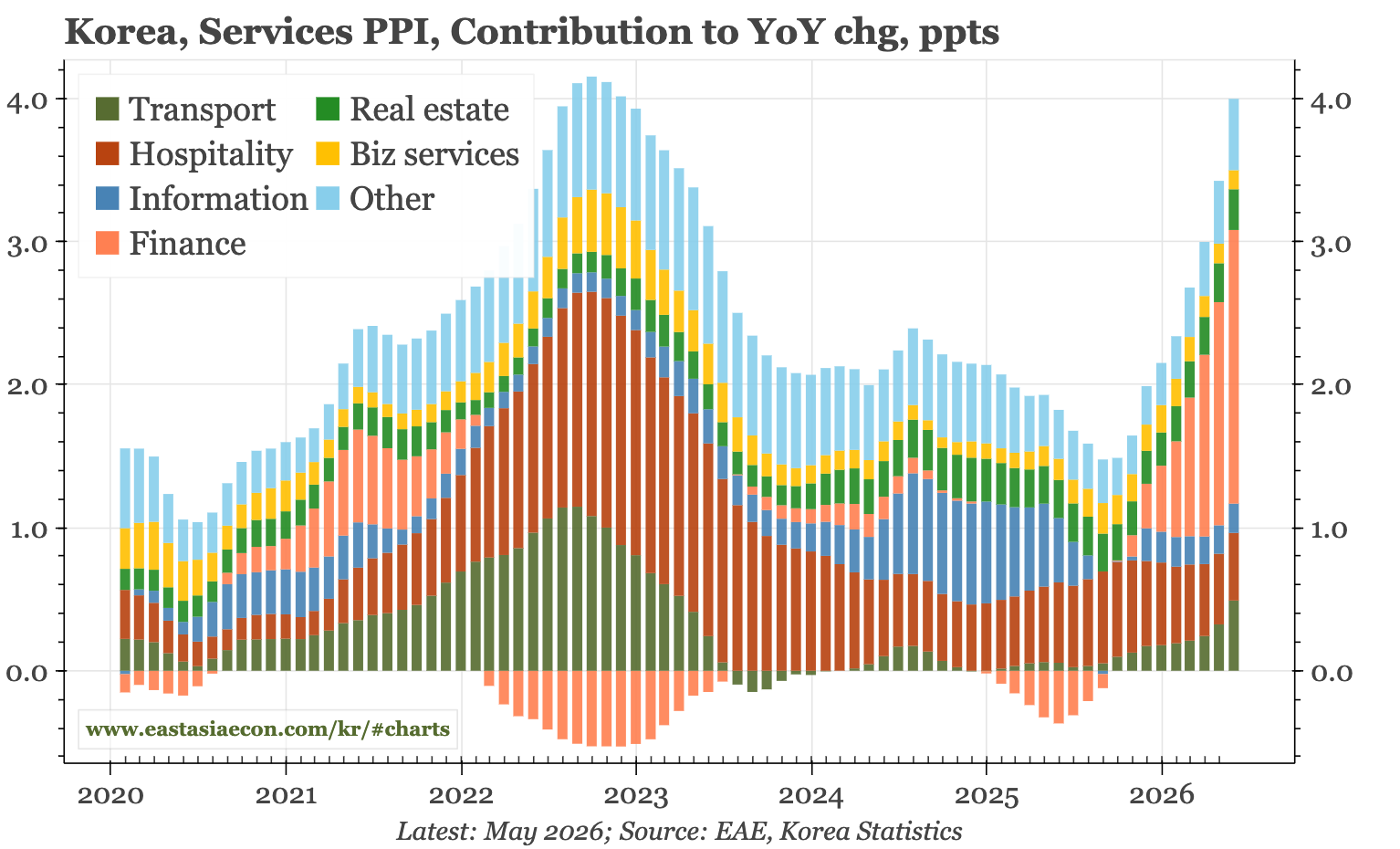

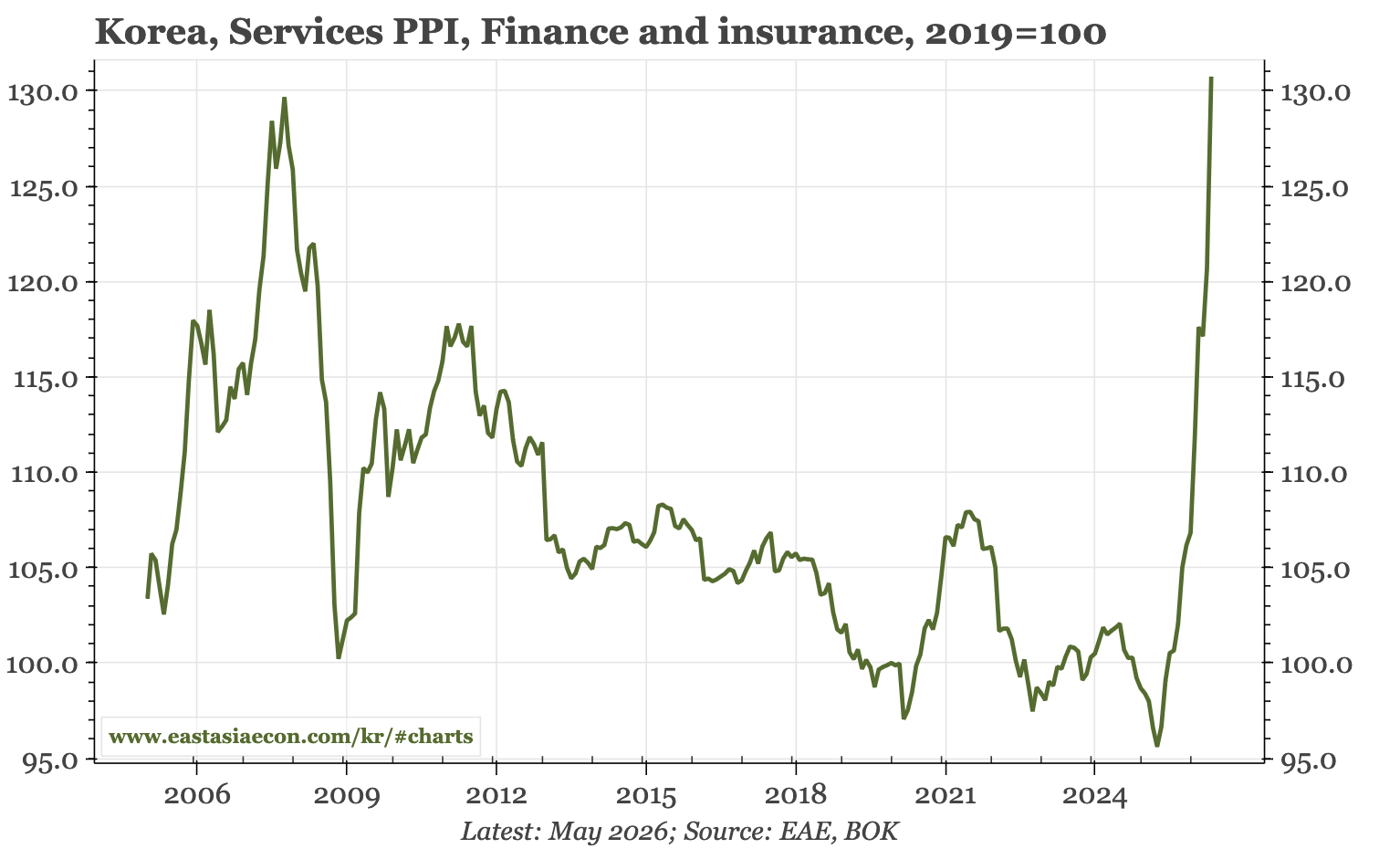

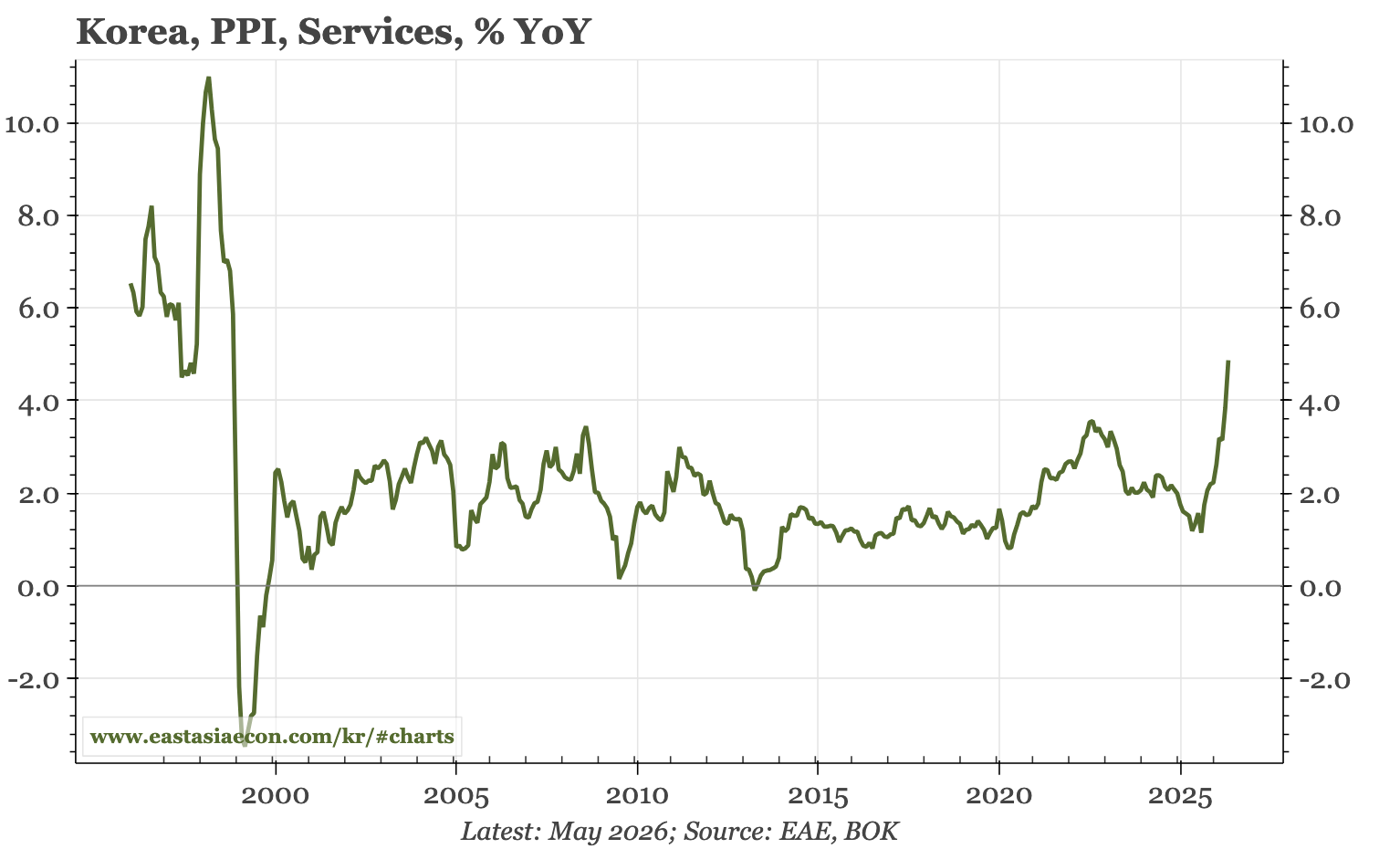

PPI accelerated to 8.5% YoY in May. With the rise in import prices already reported for May, it was no surprise that goods price inflation accelerated again, rising to over 10% YoY for the first time in 2022. However, relative to history, it is services PPI inflation that is stronger. That reached 4.9% YoY, higher than any time since the Asian financial crisis in the late 1990s. That suggests quite broad-based inflationary pressure. The complication is that a lot of the rise in services PPI, as with services CPI, is being generated by one sector, namely insurance.