Subscribers Only

Japan – EW and wages remain firm

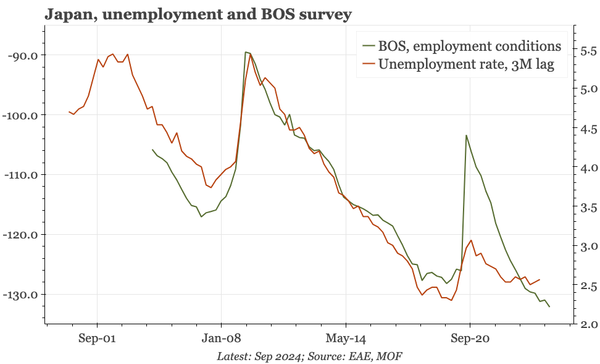

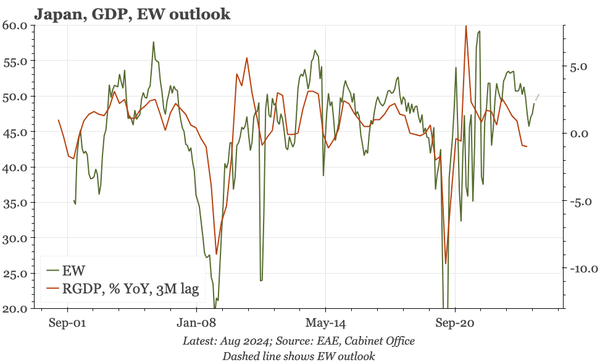

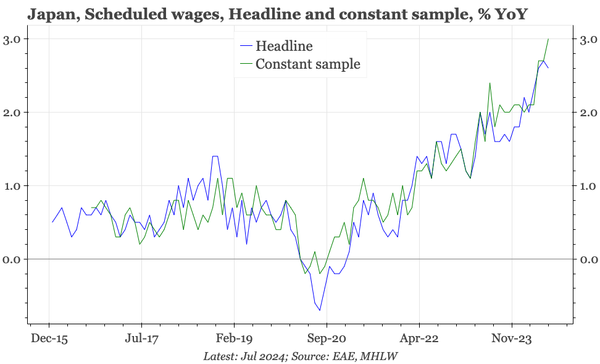

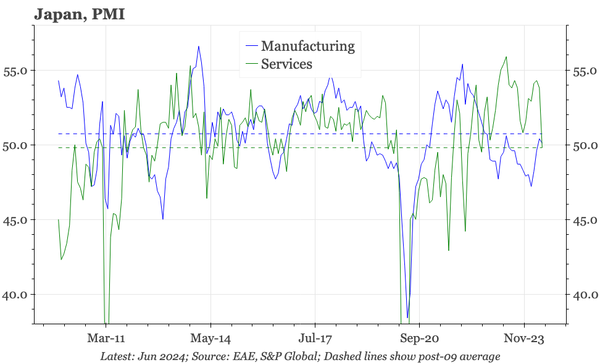

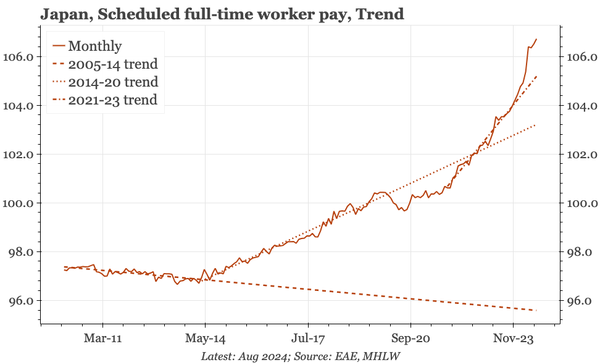

Data continue to show little change in the constructive economic assessment that the BOJ was talking about in 1H24. The Economy Watchers survey for September ticked down, but is well above the LT average, and the outlook score is higher still. Growth in underlying wages remains firm.