Subscribers Only

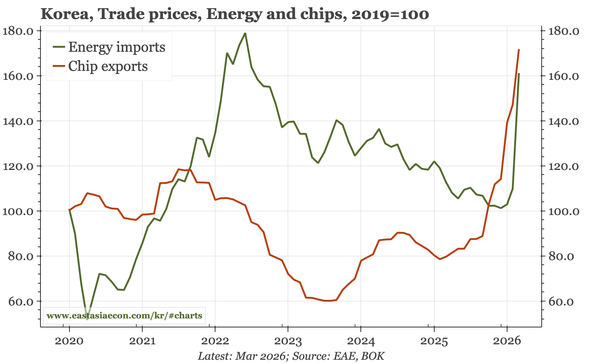

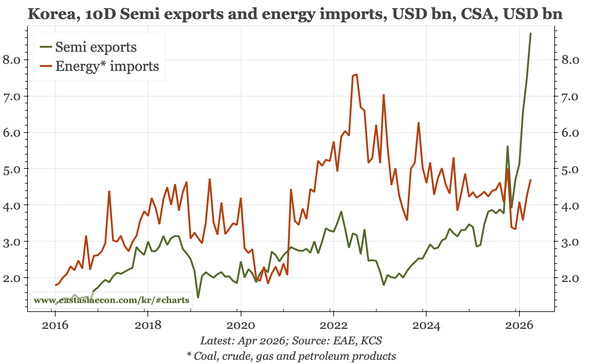

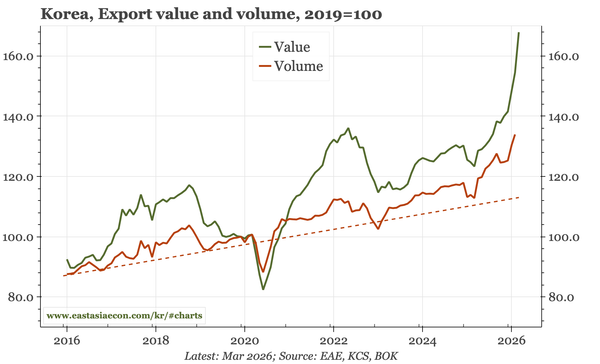

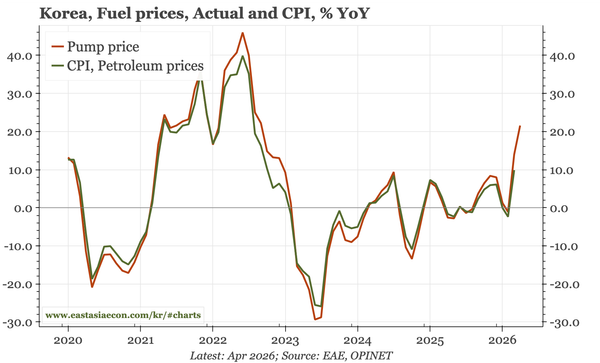

Region – import prices up, export prices up more

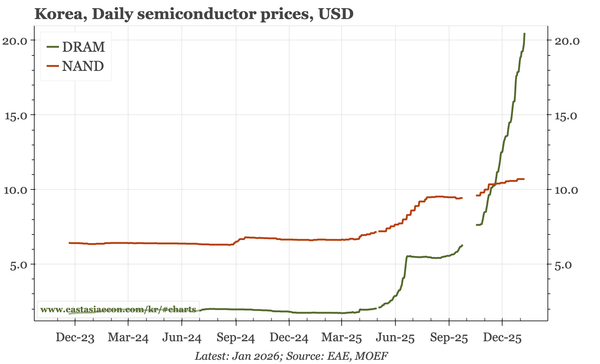

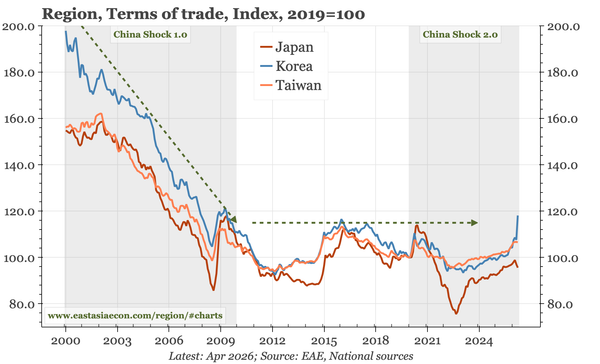

Data today for Japan and Korea show the inflationary impact of the War, with import prices in both economies rising at double-digit rates. However, such rises have been seen before. By contrast, export price inflation is setting records, offsetting the hit from energy prices to domestic growth.