Subscribers Only

Korea – further cycle deterioration

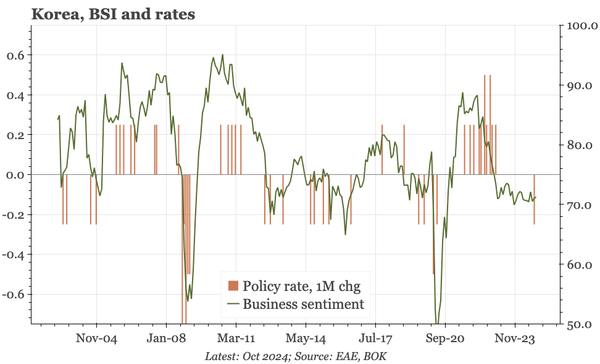

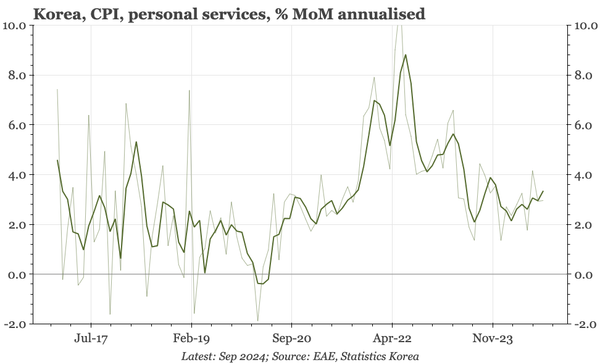

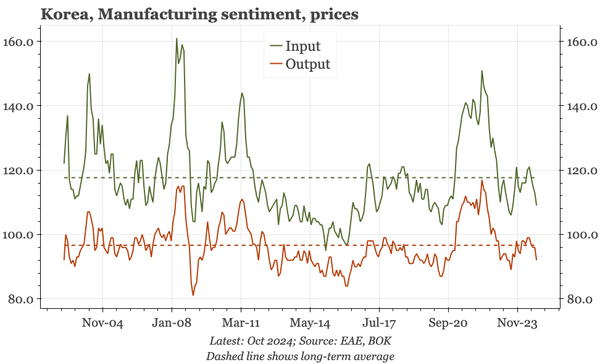

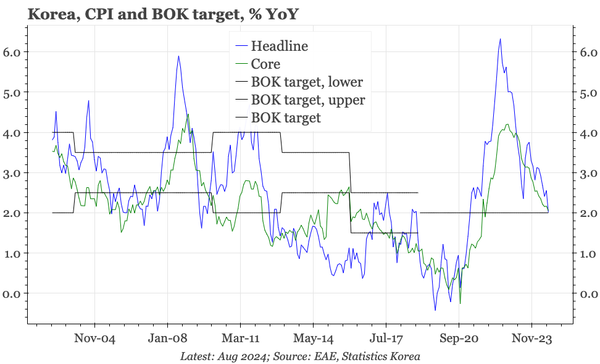

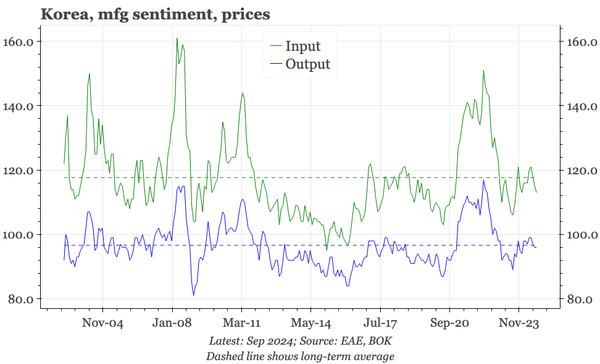

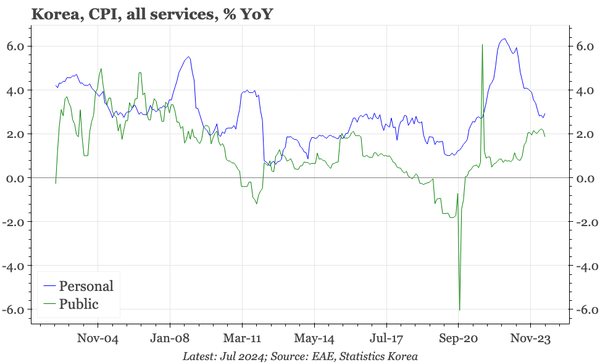

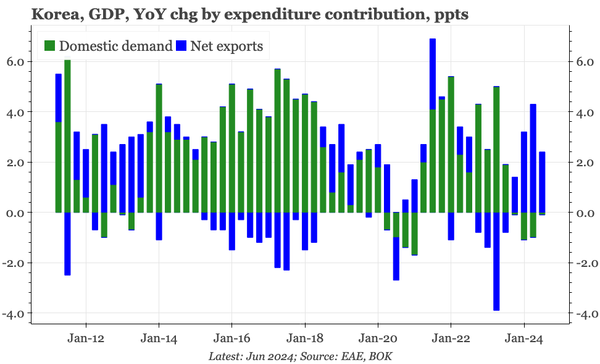

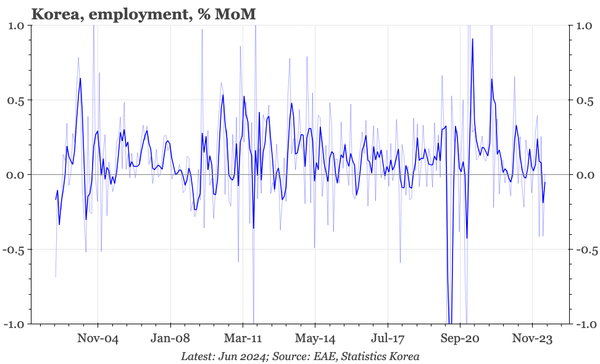

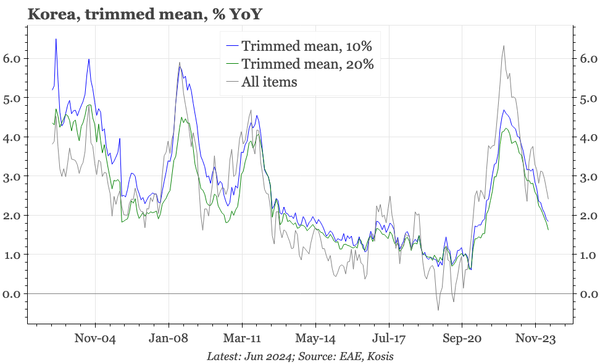

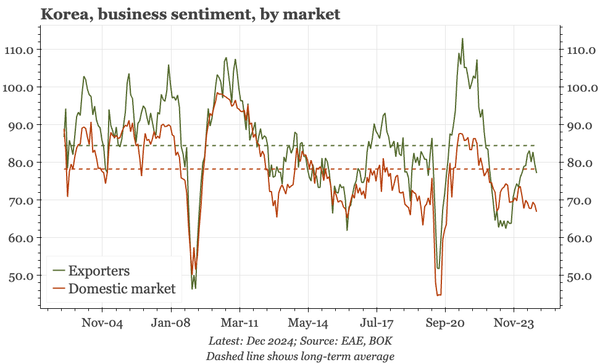

Today's business survey shows activity taking another step-down. The reason is the rolling over of external demand, which matters even more when domestic demand is already so weak. Price data this month aren't so soft, but cycle concerns are likely to become the number one concern for the BOK.