Subscribers Only

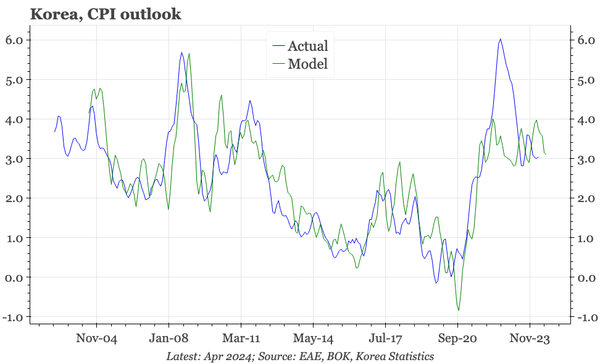

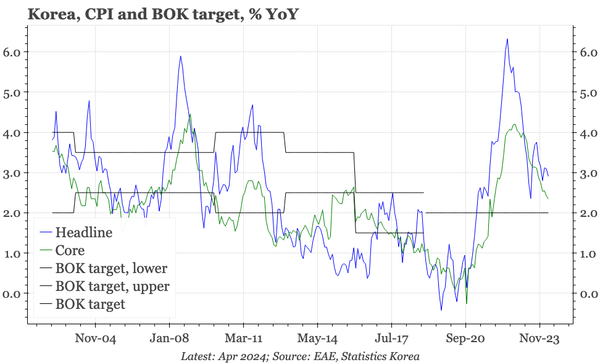

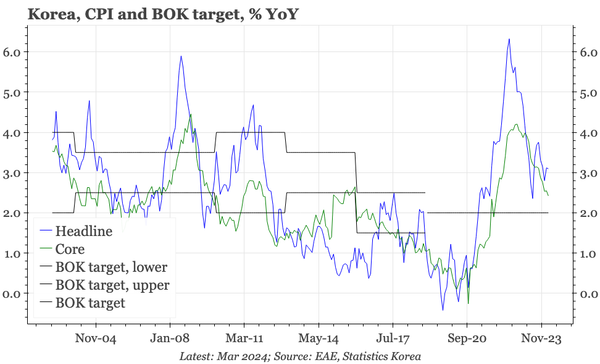

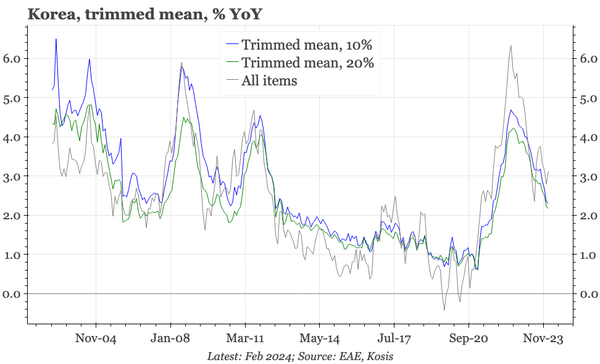

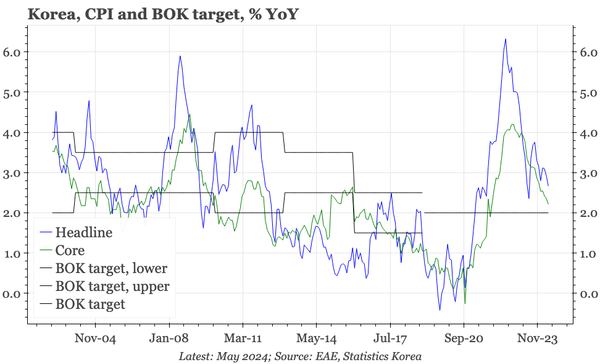

Korea – inflation eases further

There are some signs of stickiness in services inflation, but May data show that, overall, CPI continues to move in the right direction for the BOK.