Last week, next week

I'm taking a few days off next week, so you won't hear from me again until Monday 17th. Meanwhile, this is what happened on East Asia Econ this week.

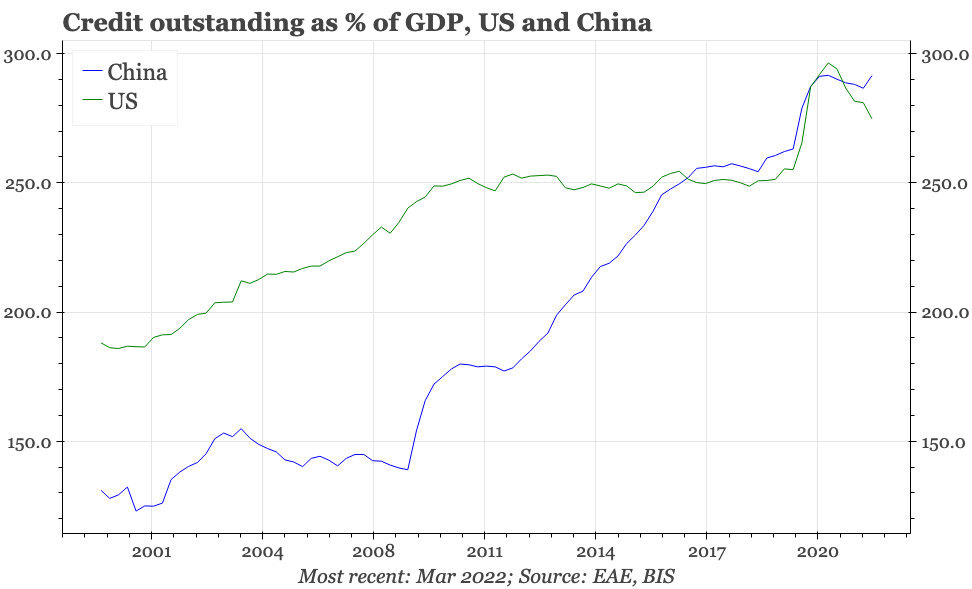

While they are a bit lagging, the Bank of International Settlements publishes the most authoritative cross-country data on global credit ratios. The Q122 data, released in September, showed that credit relative to GDP in China is once again rising, while it is falling quickly in the US. Of course, for the US, this is due to high inflation. But still, the data remain striking given China, unlike the US, has attached a lot of policy importance to “deleveraging”.

Policymakers have blinked, announcing a raft of measures to support property. On their own, these aren't sufficient to have conviction that the economy will turn. But with improvement in the construction PMI, they do suggest that for the first time in a while, not all the cyclical risks are down.

The Q3 Tankan indicates that growth should be just about strong enough to produce a further closing of the output gap. In this sense, while they aren't particularly solid, some foundations are falling into place for a broadening of inflation away from just import costs and goods prices.

Headline inflation is easing, which should start to impact expectations of how much more the BOK will hike from here. But core inflation on a MoM basis remains elevated, supported by rising services prices.

Taiwan's manufacturing PMI softened again in September to 44.9, while exports and inflation also fell. The industrial data from Taiwan are warning of a sharp downturn in external demand, a development that has regional implications. For Taiwan itself, with inflation low, the CBC likely won't be hiking, meaning more cyclical pressure for TWD depreciation.

The biggest event in the region will be the CCP's 20th party congress that starts on October 16th, though that is unlikely to be as important for markets in the short term as China's September credit and export data that will be released in the days before Xi Jinping's big speech. The BOK will likely tighten on Wednesday, and it is probably still a bit early for the country's labour market data on Friday to show much slackening. The Economy Watchers survey and BOJ quarterly consumer survey next week will be useful in assessing whether the gradual warming of Japan's economy can accelerate.