Subscribers Only

Last week, next week

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

The platform for tracking and understanding East Asia macro

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

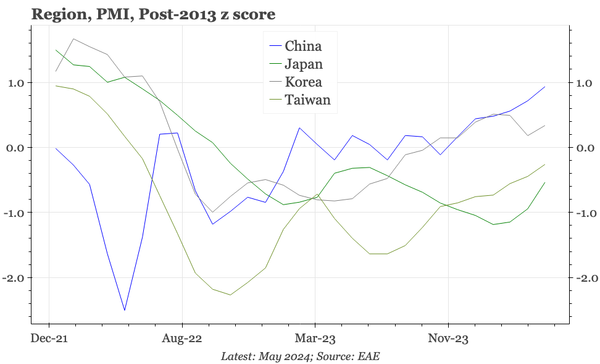

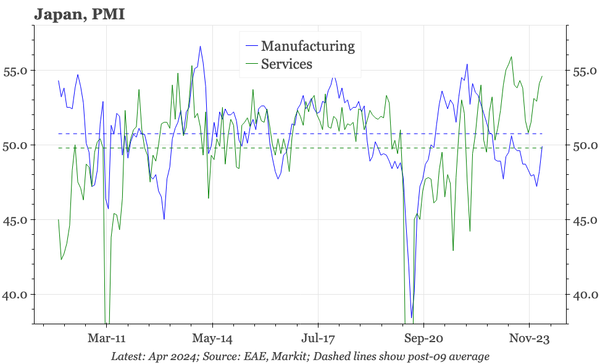

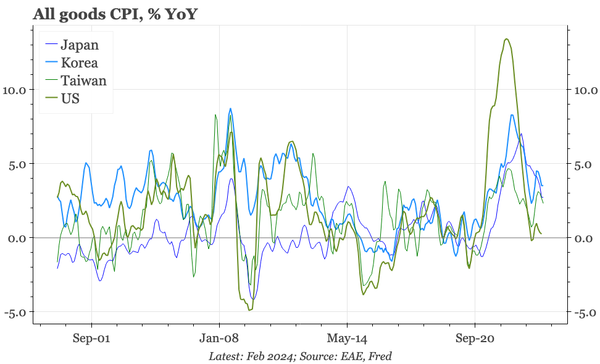

The regional mfg cycle is recovering, but gaps between official and S&P PMIs mean it is difficult to gauge strength. However, all surveys do point to a broad-based firming in input price inflation.

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

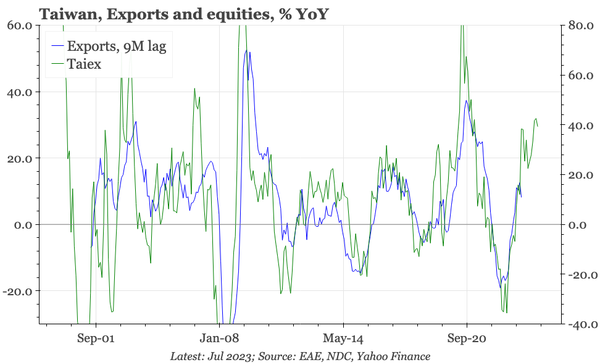

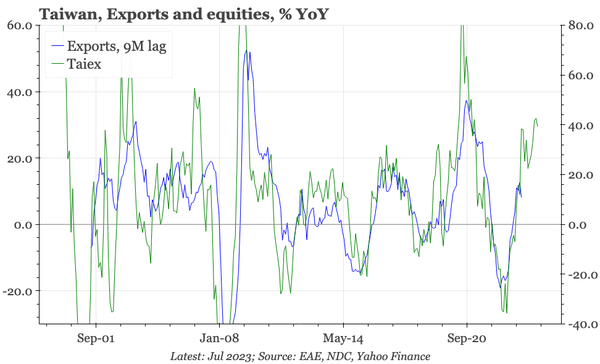

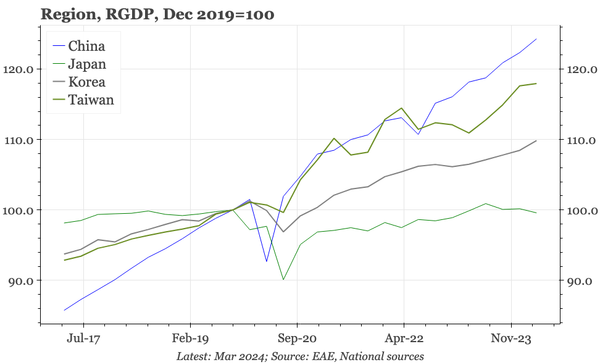

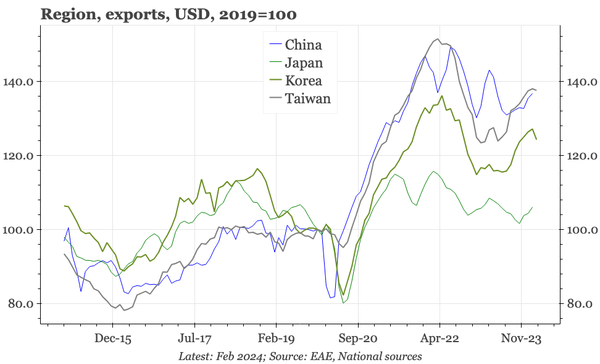

In slides laying out a comparison with Korea, we argue that Taiwan's macroeconomy is close to a structural break to the upside. An export recovery that is as strong as has been priced in by equities would likely be the tipping point.

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

Our monthly chart pack. Three themes stand out: the confidence of the BOJ; the significance of policy that tackles property inventories in China; and Taiwan remaining as the big post-covid winner.

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

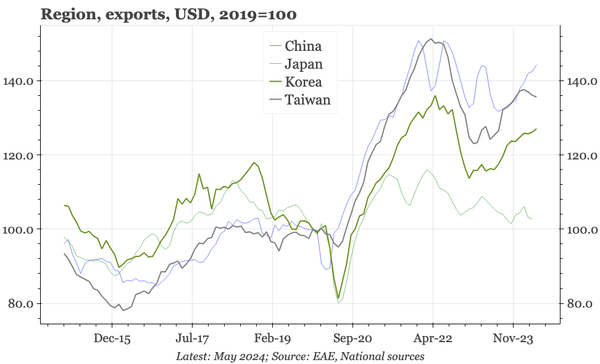

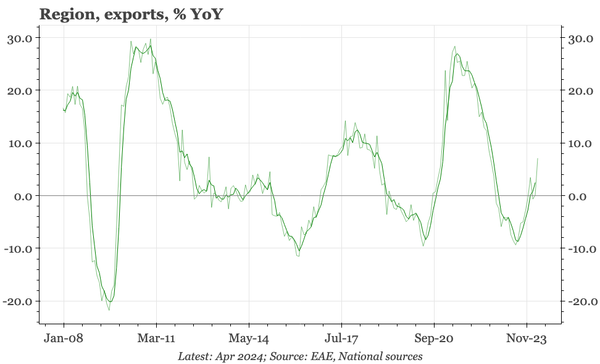

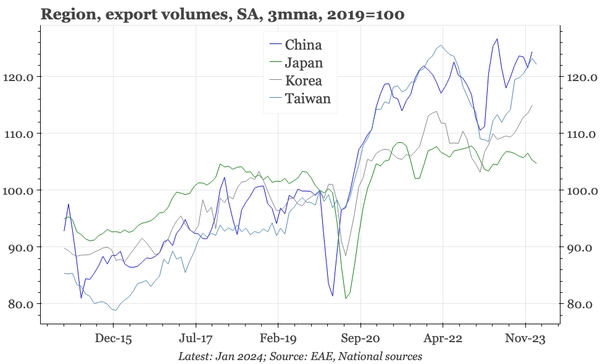

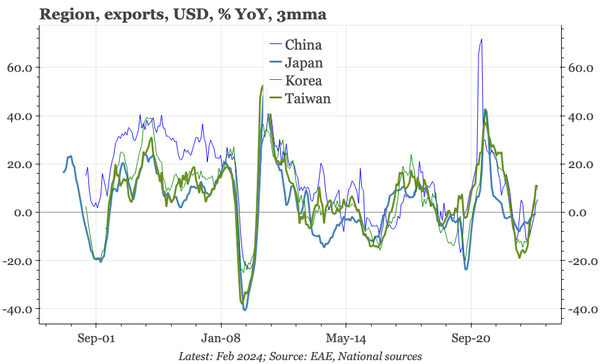

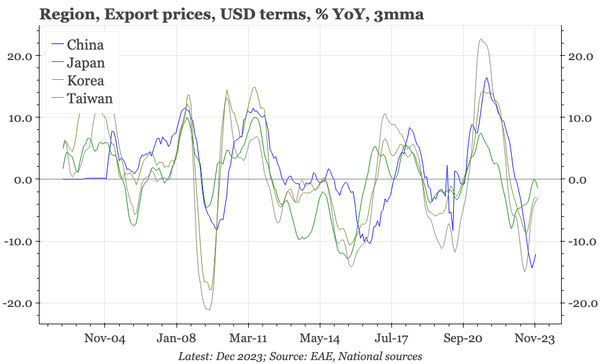

The export cycle is recovering, but more in volume than value terms, and in Taiwan and China than Korea. This won't remove worries about weak consumption in Korea and China. But it likely is sufficient to keep Taiwan's economy tight, and the CBC will likely be hiking again if exports rise more.

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

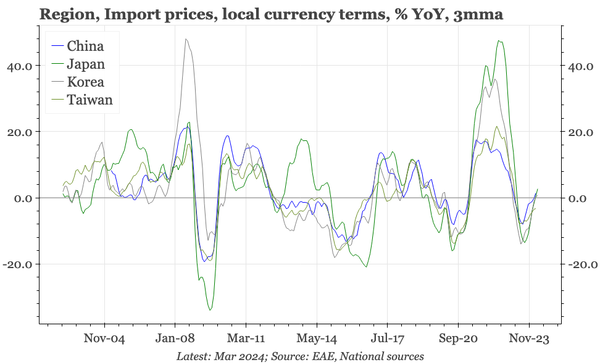

We are getting near a test of our thesis that PPI deflation in China is mainly cyclical, with global commodity prices suggesting a PPI recovery.

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

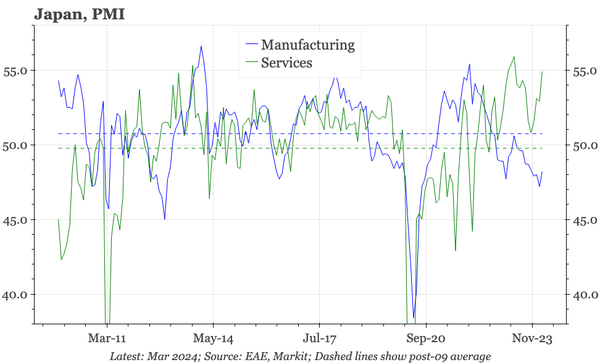

Not just in Japan but Taiwan too, there are signs of a structural break from persistently low wage inflation. The implication is that the gap between nominal monetary settings between both and the US is likely to be narrower in the future than it has been in the past.

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

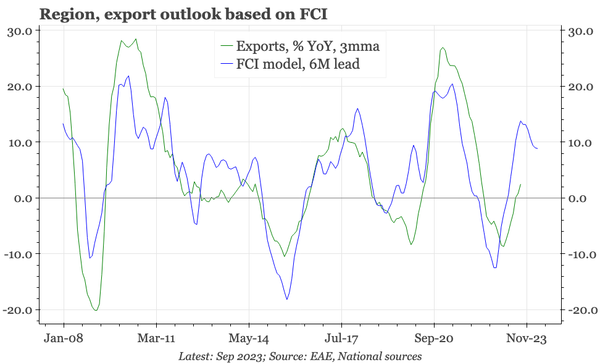

It is always tricky to get a real sense of the manufacturing cycle early in the year when the data are so distorted by the LNY holiday. From what we can tell, it doesn't look like there's been a big pick-up yet, though leading indicators continue to point to upside ahead.

Our opinion piece today from Nikkei Asia.

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

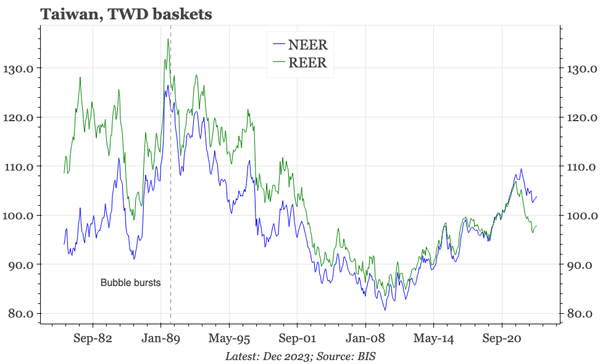

A chart pack presenting a framework for regional currencies. We use secular JPY and TWD depreciation to lay out the framework; apply that to the CNY today; and finally, argue that there are reasons to think the structural weakening of the TWD and JPY is likely ending.

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.