Subscribers Only

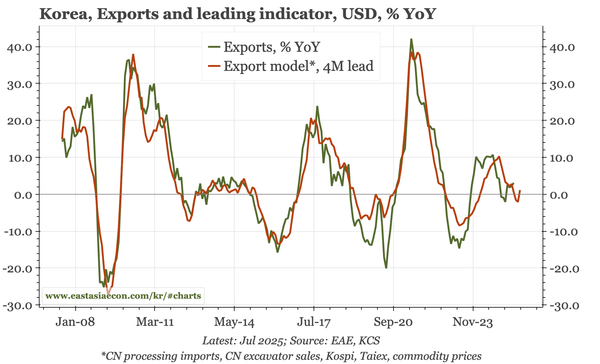

Korea – still the NPS outflow, but also foreigner inflows

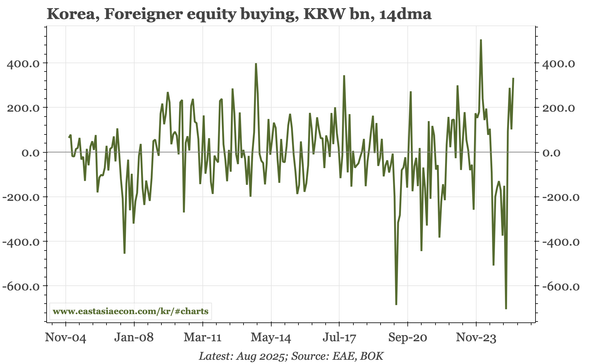

The main flow dynamics didn't shift in June. The CA surplus remained large, while NPS and FDI outflows were solid. But the revival of domestic equities has caused some changes, with less household overseas buying, and more foreigner domestic buying.