Public Post

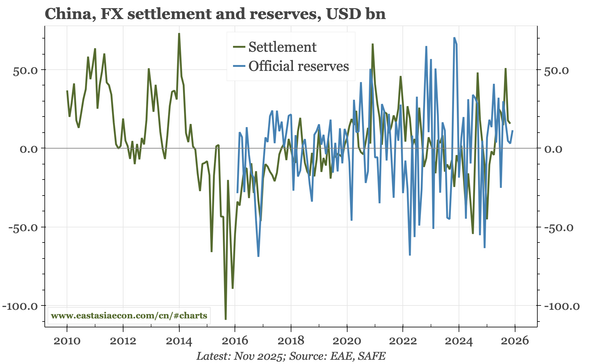

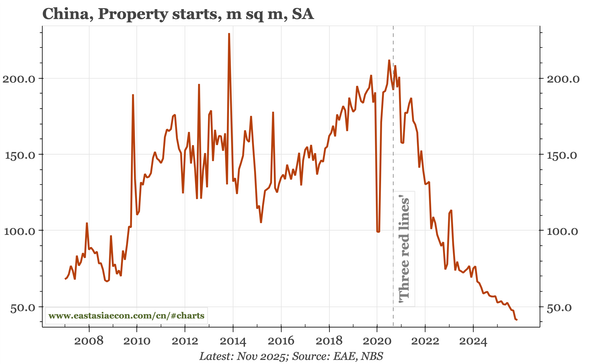

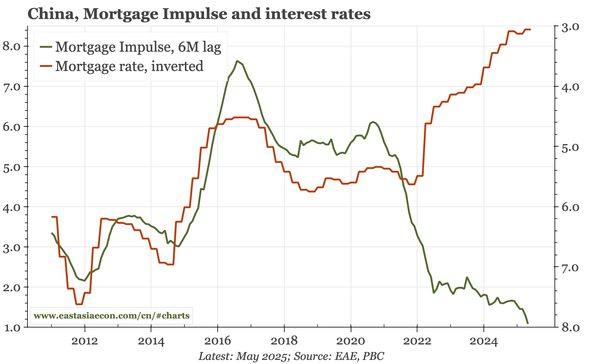

China – the case for a floor

My latest video, discussing the lessening of deflationary pressure, whether that can continue, and what the implications are for markets.