Subscribers Only

East Asia Today

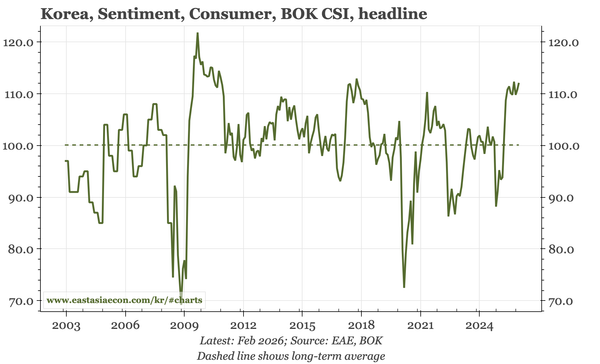

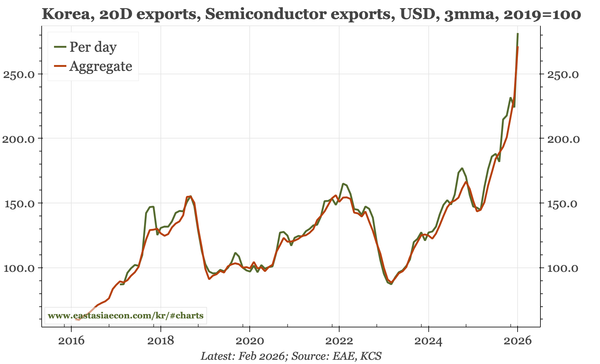

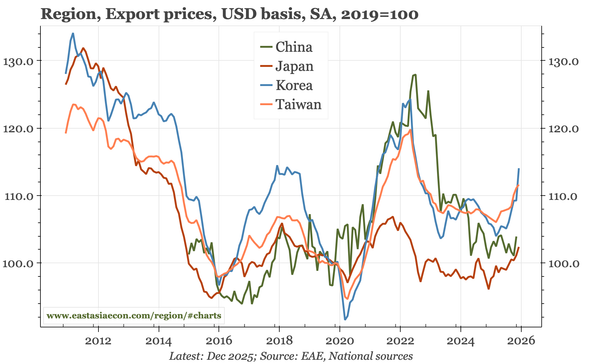

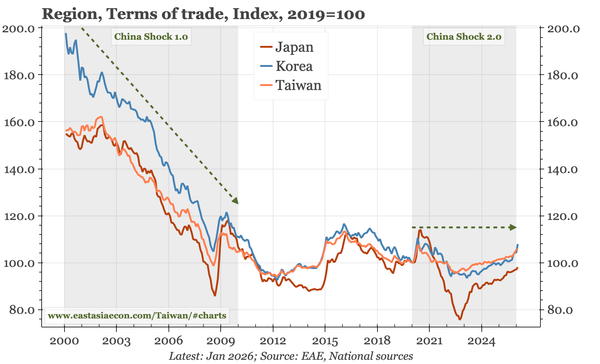

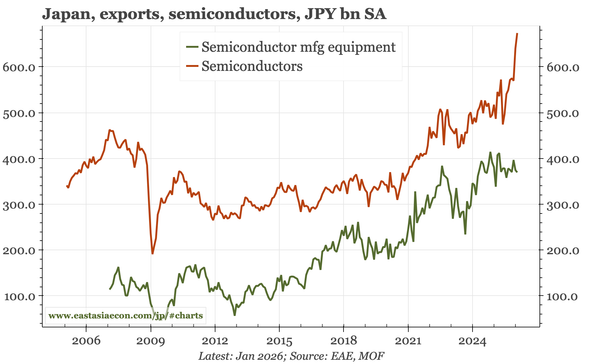

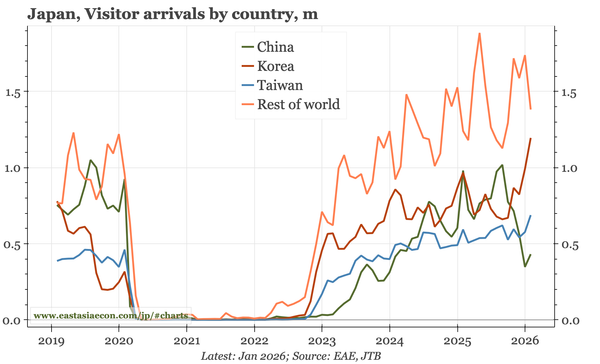

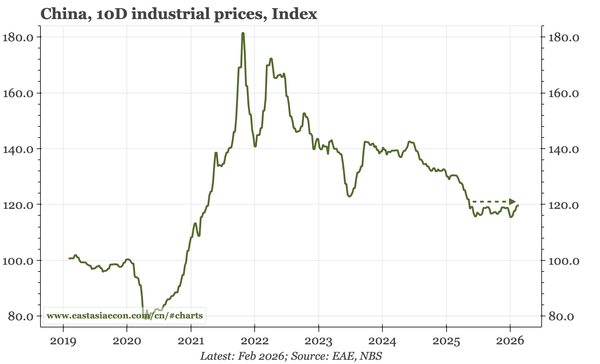

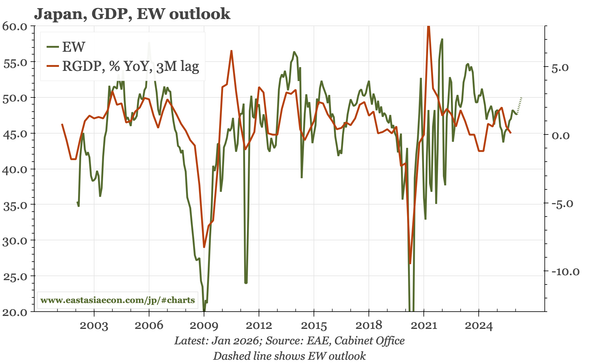

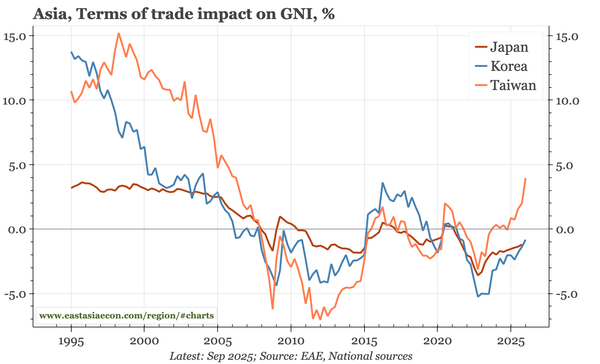

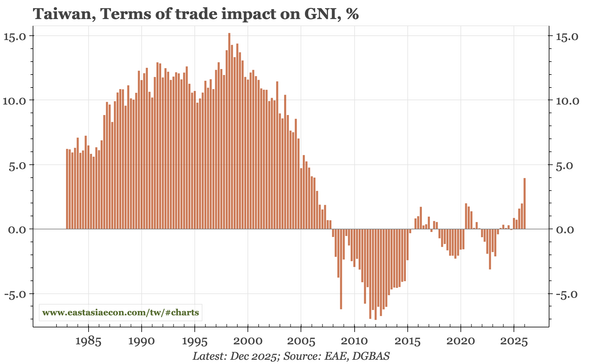

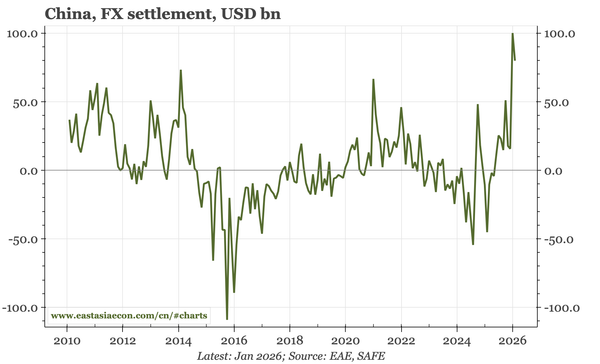

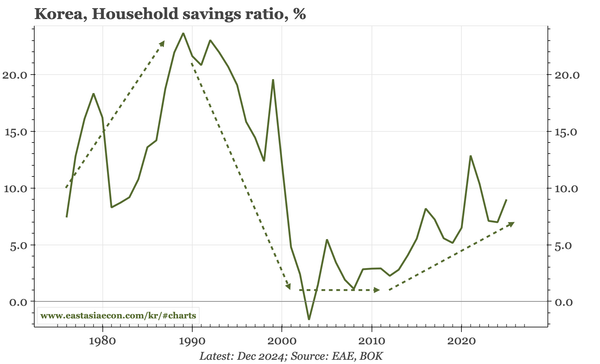

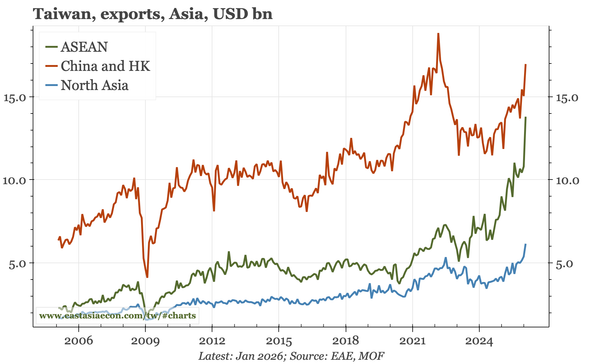

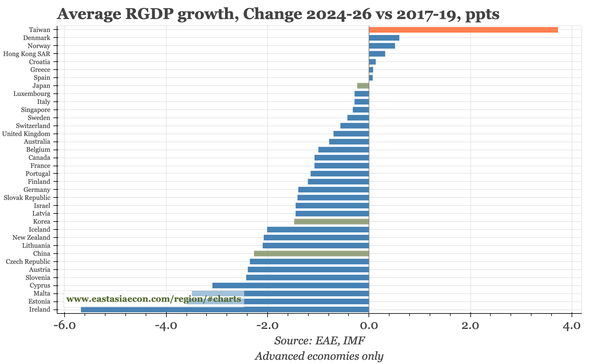

A few charts from a longer slidepack looking at the remarkable changes in Taiwan's economy since 2020, details of consumer confidence and PPI in Korea, and export volume data for Japan for January.