Subscribers Only

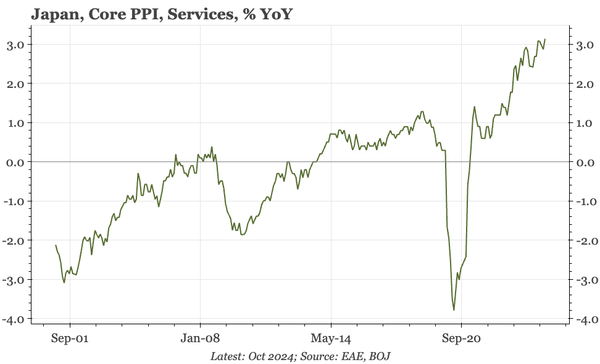

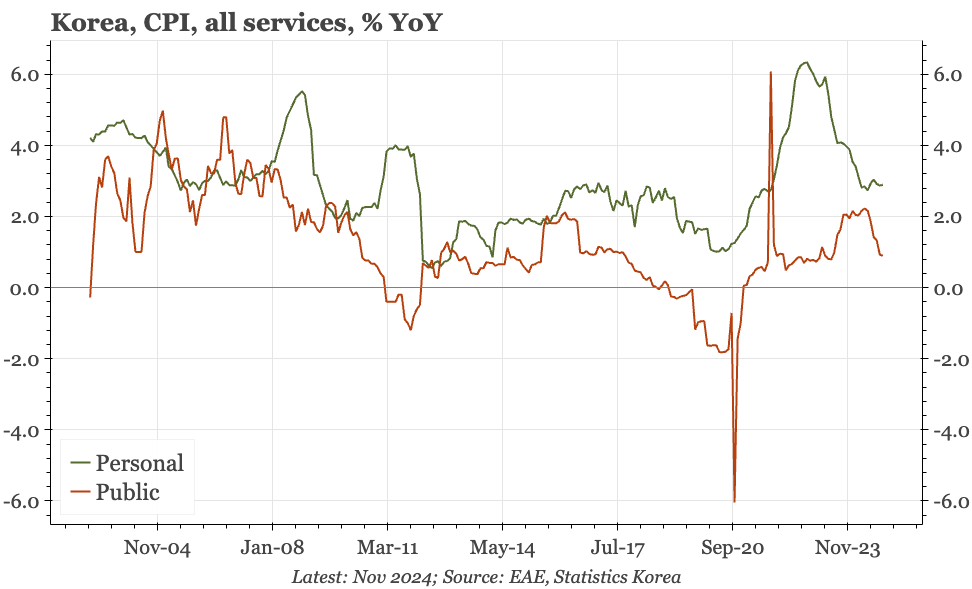

Korea – private services inflation still edging up

Headline November CPI data don't challenge the BOK's confidence that inflation is under control. But private services inflation continues to creep up, with SAAR now above 3%. That core has remained around 2% is because of cheaper public services. With budget tightening, that seems tough to sustain.