Subscribers Only

Last week, next week

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

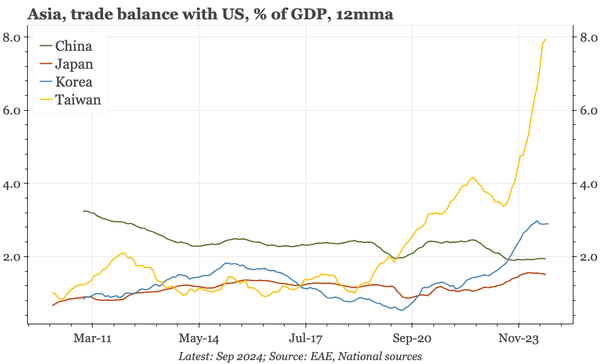

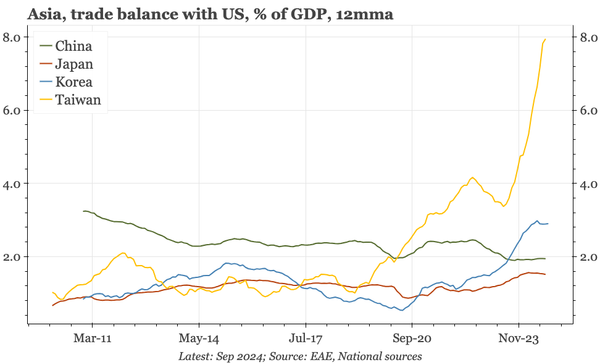

Today's October FDI data once again illustrate the big reorientation of Taiwan's investment and trade flows away from China and towards the US. For FDI that's been encouraged by Biden subsidies, but Trump doesn't like those, nor the big trade surplus that Taiwan now runs with the US.

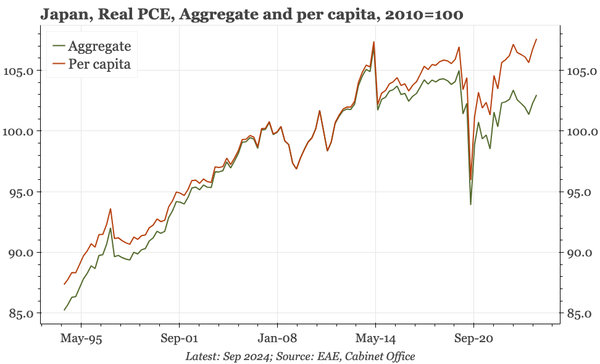

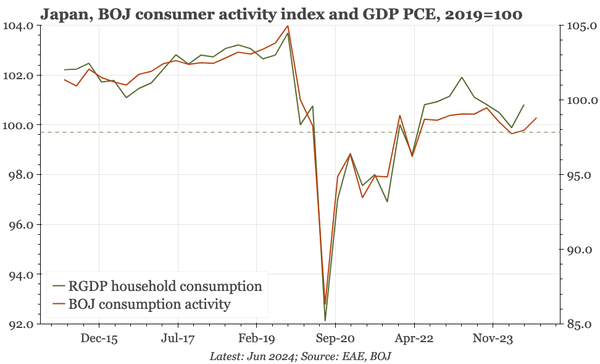

GDP grew again in Q3. Much of the rise since Q2 is because of a recovery in consumption, but that continues to be much more visible in per capita terms: aggregate consumption is still below the pre-2020 highs, dragged down by a fall in the population, a decline that the BOJ obviously can't address.

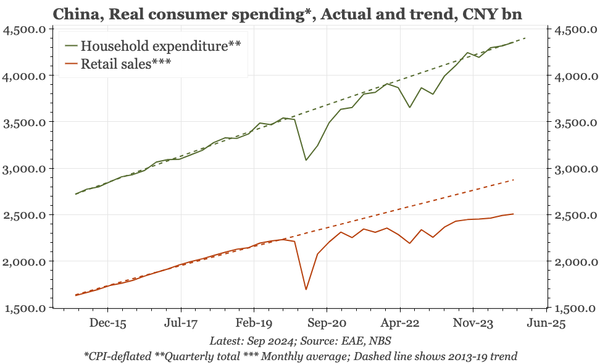

With a bounce in reported retail sales, it looks like economic growth in October got back to the government's 5% growth target. Overall, though, the tone of the data was rather mixed, with real estate activity in particular still extremely weak.

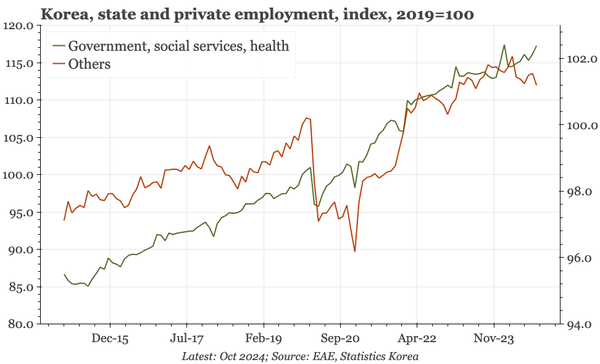

The headlines don't show much change in the labour market in October, with the unemployment rate still comfortably below 3%. But while employment overall was stable, that was because of government jobs. Employment in the private sector fell again and is now the lowest since July 2023.

In recent years, trade and FDI flows from Taiwan and Korea have clearly shifted from China to the US. That's what Trump One and Biden wanted, but Trump Two won't like the rising trade deficits, or the CHIPS and IRA subsidies. If he threatens tariffs, will Taiwan offer a stronger TWD in response?

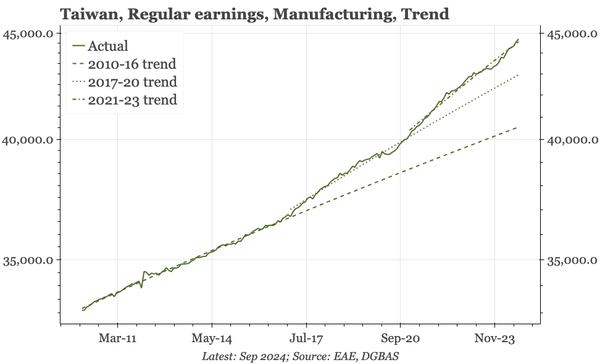

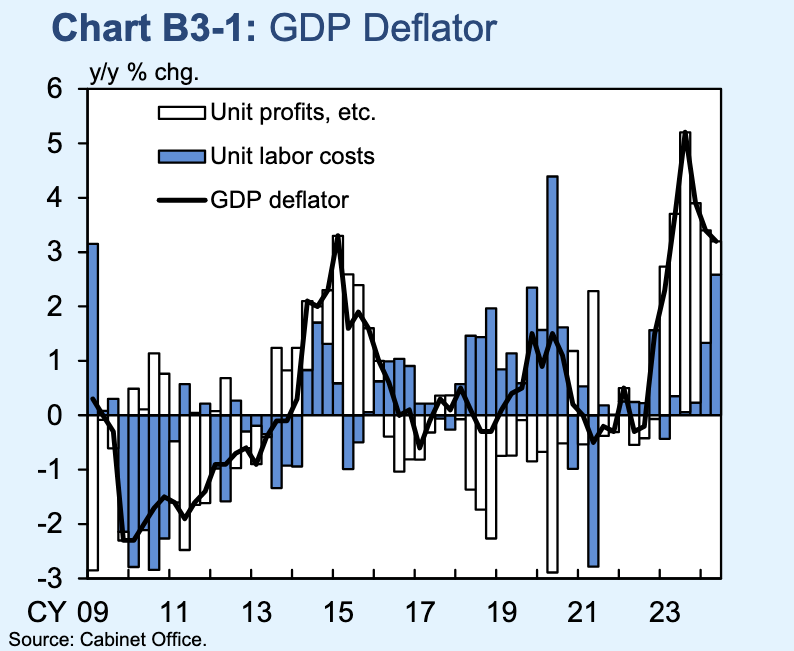

The post-2020 rise in wage growth is holding in manufacturing. In services, it is less obvious, but for the economy overall, the trend in wage growth is still comfortably above 2% YoY, whereas in the 15 years from 2003 it was closer to 1%. This rise, in turn, should raise the floor for inflation.

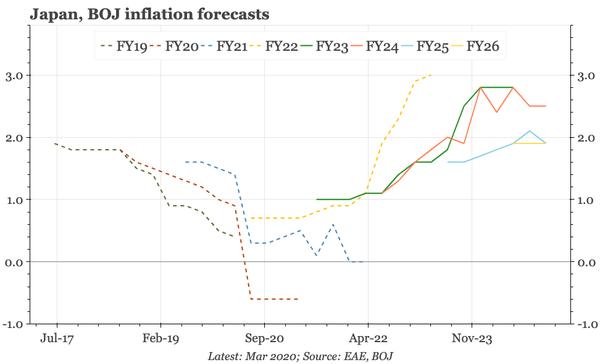

The opinions from the October BOJ meeting show a bit less concern about US uncertainty. That seems premature, given the election, but comments on the domestic economy also don't suggest any change in the bank's fundamental view. Survey data have been a bit softer, but not yet uniformly.

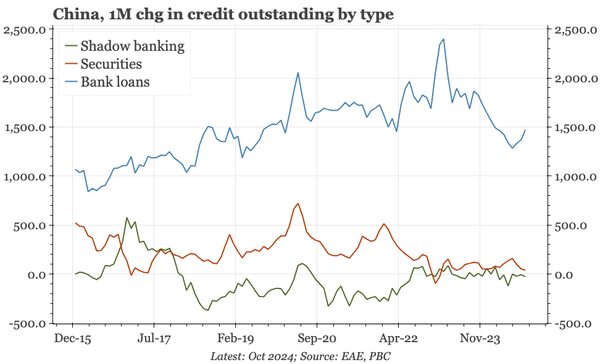

Including CGBs, the credit impulse is weak, but not terrible, and there's been a tick-up in bank lending and mortgages since August. However, there's nothing to suggest any real momentum in the credit cycle. At the same time, the deflationary move into time deposits continues.

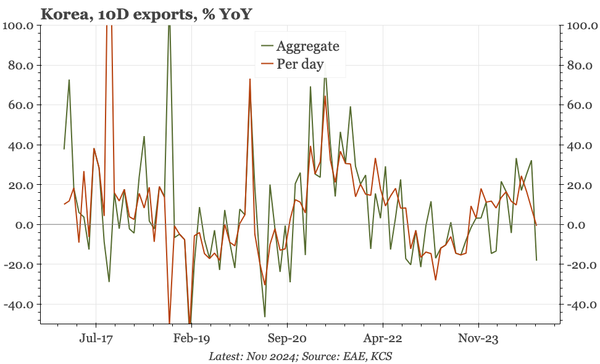

Export growth in the first ten days of November fell to zero. And while the small number of days make this data set volatile, it comes after weakness in broader data for October, both full-month trade, and the PMI. The weakness in exports is a big deal for the BOK when domestic demand is also soft.

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

The bond swap does represent substantive policy. But there still isn't support for consumption, so this does look like an effort to put a floor under growth, rather than produce a new upcycle. And while that will probably be successful, stability will be endangered by a new round of Trump tariffs.

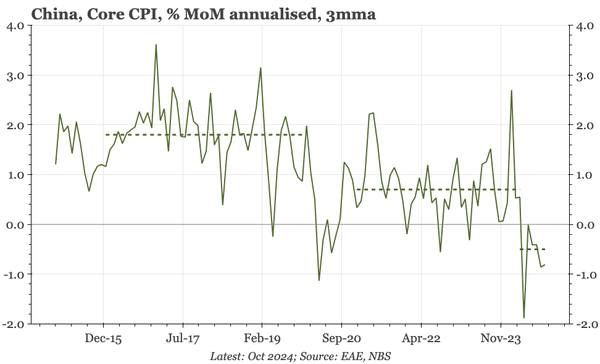

There might be some signs of better sentiment feeding into prices, but they aren't strong. Core sequential CPI inflation did get back to zero in October, but the 3mma remains negative. Despite the jump in PMI input prices last month, PPI also continues to fall.

Today's release from the BOJ of consumption activity through September is so-so, with a further moderation from the pick-up seen in June and July. As such, it isn't suggesting a repeat of the pick-up in household consumption that boosted Q2 GDP.

A chart pack arguing that consumption hasn't been as weak as is often imagined, but that downside risks are growing as wage and property income falls. Policy solutions need to overcome the weakness of non-wage incomes, the strength of savings, and the pro-investment official mindset.

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

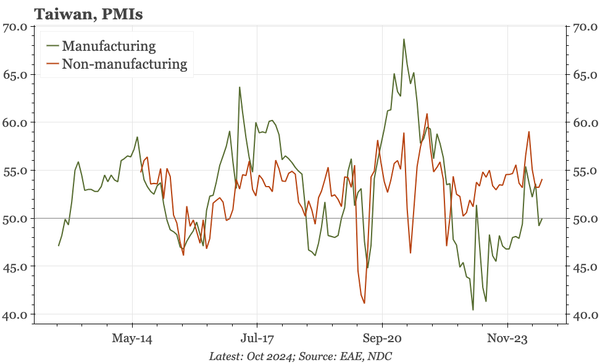

I thought the drop in the mfg PMIs in October might have been noise. But the November data show it is more than that, remaining weak in both Taiwan and Korea. Korea's exports today fell too. That makes the domestic cycle more important, and in Taiwan, that looks more resilient than Korea.

The boxes in the BOJ's full outlook report that look at the labour market and wages don't suggest any weakening of the bank's underlying confidence – increasingly evident before July – that Japan's inflation is sustainable. The implication is that rate hikes remain on the agenda.

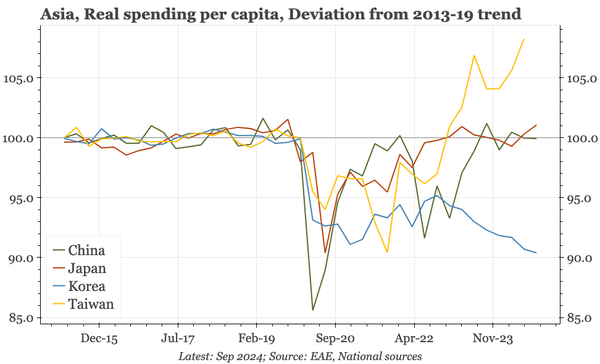

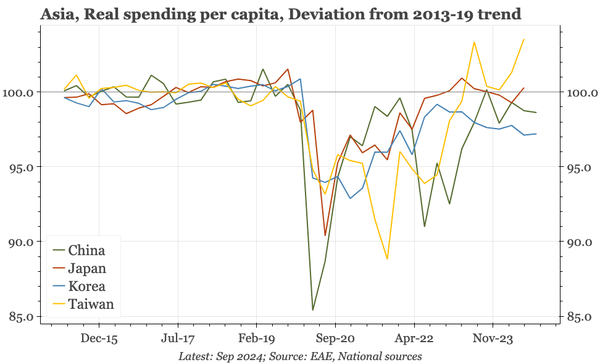

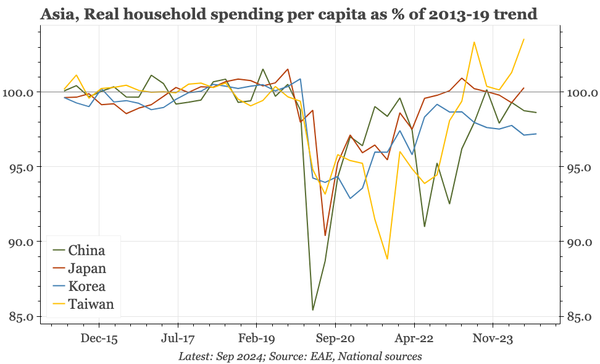

Some analysis of the weakness of consumption in Asia. As the opening chart suggests, the big underperformer isn't either China or Japan, but rather Korea. The clear outperformer is Taiwan.

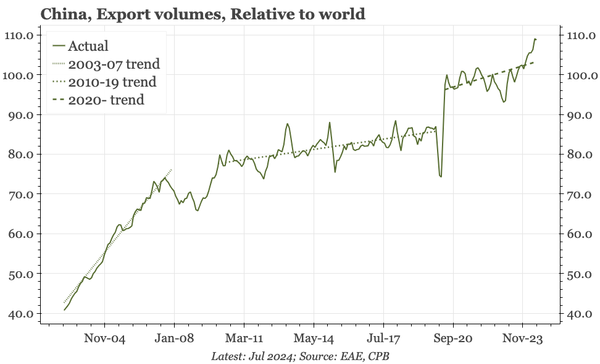

More evidence today that the export cycle has at least peaked, with a sharp slowdown in shipments in October, and another weak PMI. Equity market performance points to there being worse ahead.

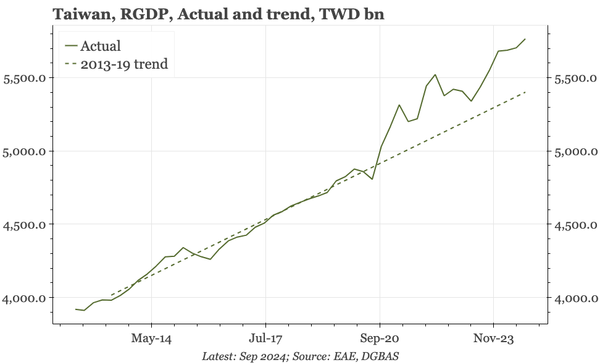

While consumption and the leading indicator have warned of cycle moderation, today's data show GDP growth ticked up QoQ in Q3, led by capex. With TSMC still bullish, Taiwan continues to have one of the strongest cycles, making it unlikely the central bank follows the global trend of rate cuts.

No surprises from the BOJ (yet): the July forecast for underlying inflation to remain around 2% was maintained, as was the policy caution since August that stresses uncertainty in outlook for the US. There's still the press conference and full outlook report to come.

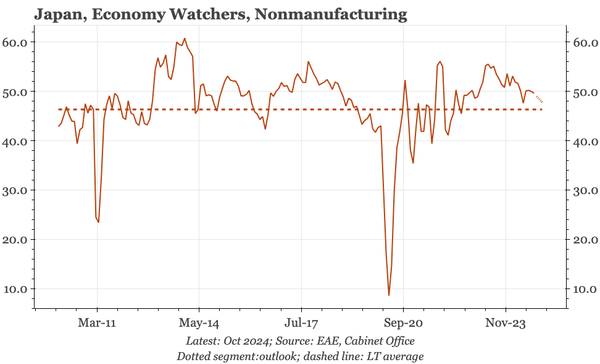

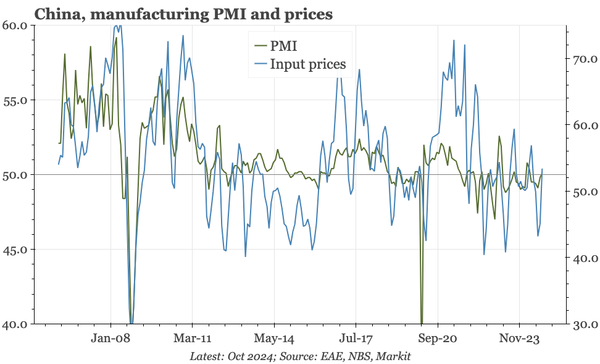

Likely driven by the sentiment-driven rise in prices, the manufacturing PMI bounced back above 50 in October. But there was barely any change in either the services or construction, PMIs, and both will need to improve to think that the economy really is turning around.

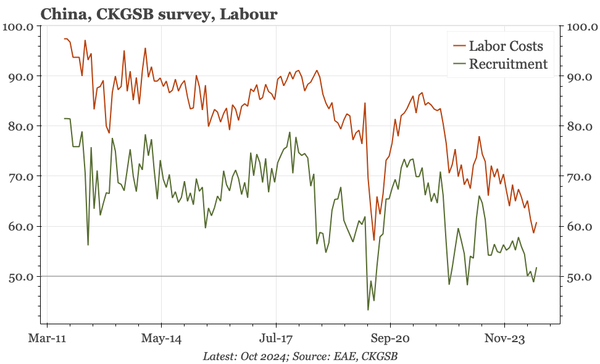

We'll find out more with tomorrow's official PMIs, but while the CKGSB survey for October does show an uptick in overall sentiment, the measure for employment remains very weak. With profits terrible in September, it is clear policy needs to do a lot to turn the cycle around.

Headline consumer confidence ticked down in October, led by pensioners. But the overall survey continues to send a constructive message for the BOJ. That's because consumer confidence remains relatively firm, even as inflation expectations show no sign of receding.