Public Post

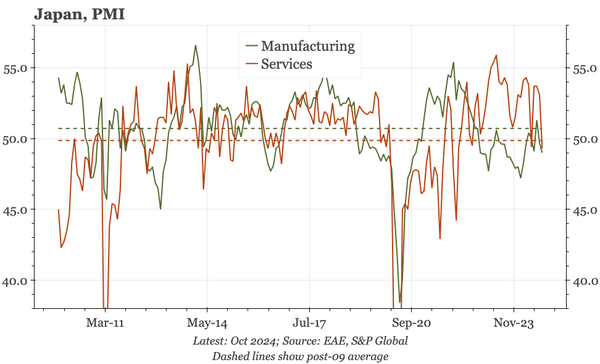

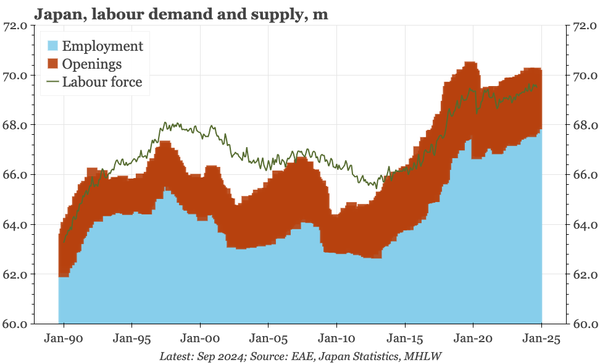

Japan – supply constrains labour demand

UE ticked down in September as the part rate fell. Employment hardly changed at all. There probably isn't much room for changes on the demand-side, as demographic constraints on supply become more binding. A negative shock will show up as rising UE, but firm demand will materialise as higher wages.