Public Post

QTC: China – velocity still falling

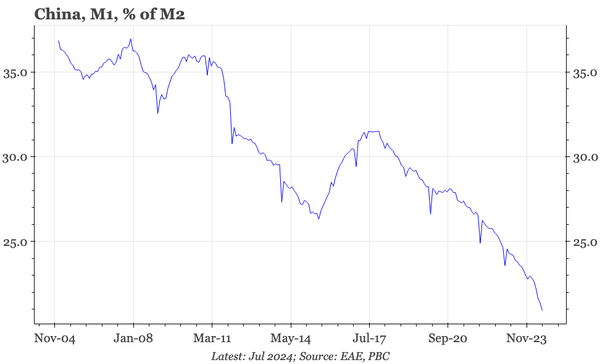

The 6.6% YoY fall in M1 in July is unprecedented. The drop is partly because of regulatory changes, but those don't explain the continued rapid decline in M1 relative to M2, a change that strongly suggests no let-up in the deflationary pressure the economy is facing.