Subscribers Only

East Asia Today

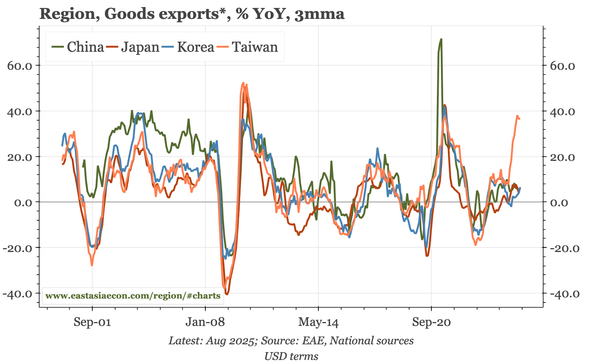

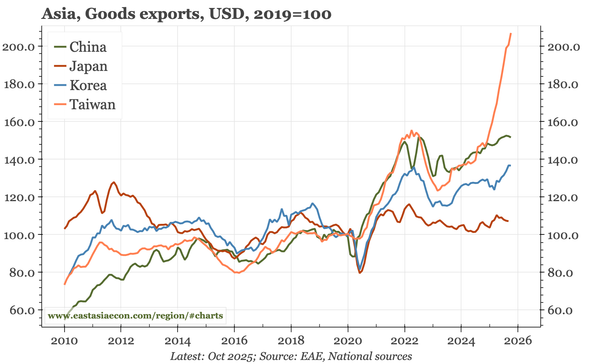

Today's trade data for October were interesting, being stronger in Taiwan, but weaker in China. Taiwan's trade surplus surged again, but despite the narrowing in China, fx reserves rose in October. Also today, a note delving into an under-explored aspect of China's FAI data.