Public Post

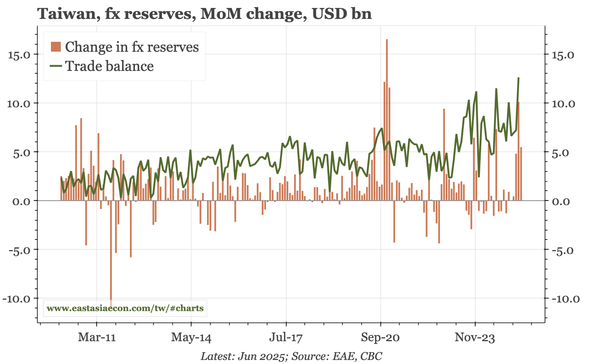

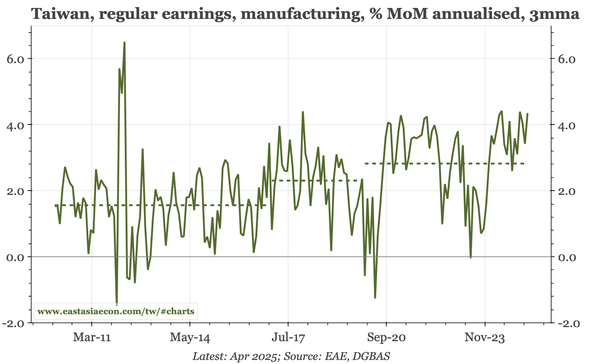

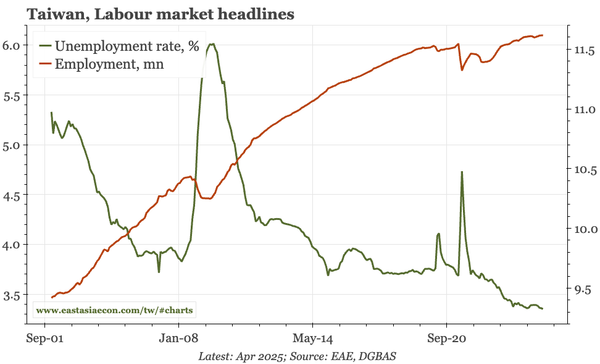

Taiwan – cycle lifting wages and productivity

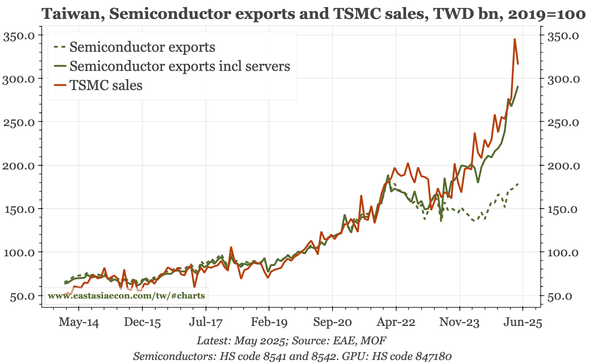

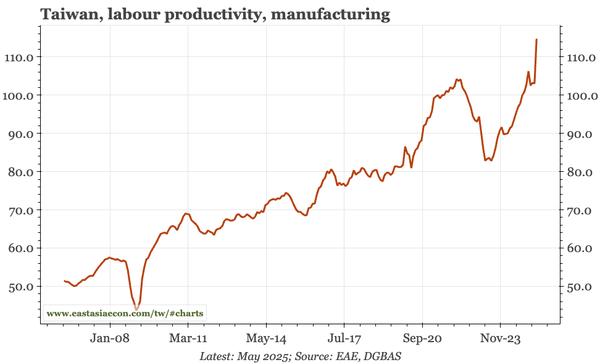

Wage growth slowed in May in manufacturing, but the trend is still up, and in recent months it has been firm in services too. That CPI is slowing is partly due to the TWD, and partly productivity. In separate news, TSMC's sales were softer in June, but financial markets don't seem concerned.