Subscribers Only

Last week, next week

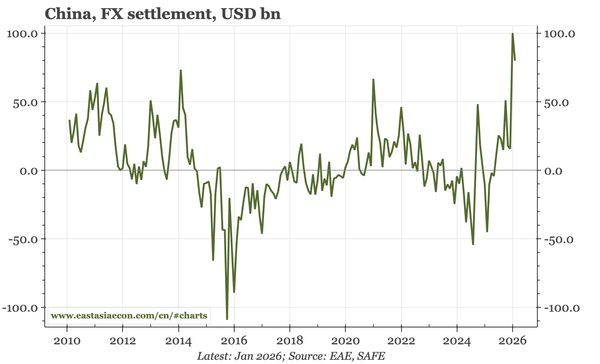

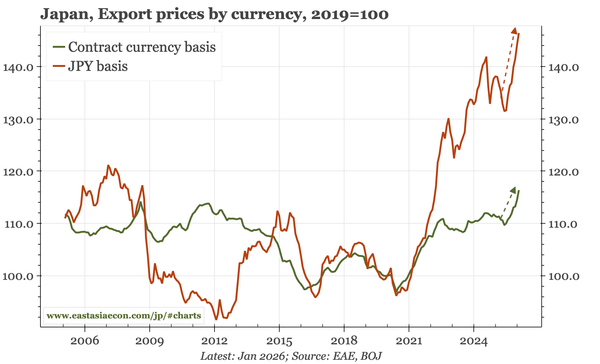

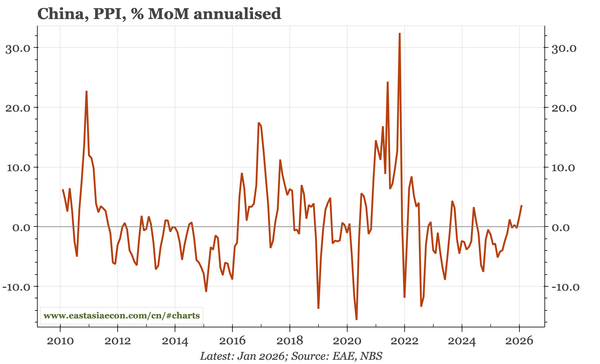

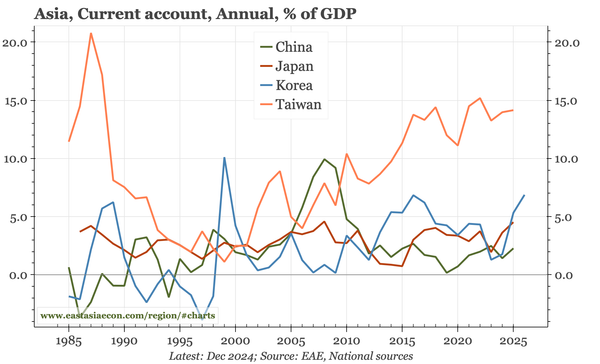

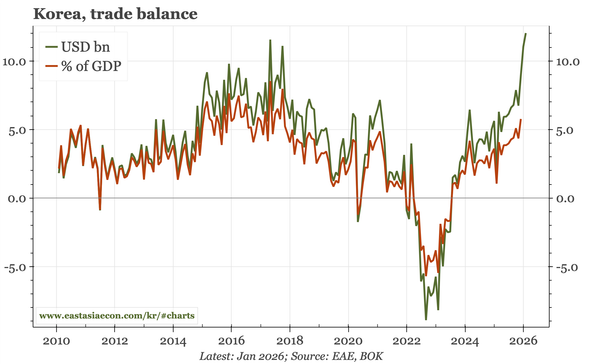

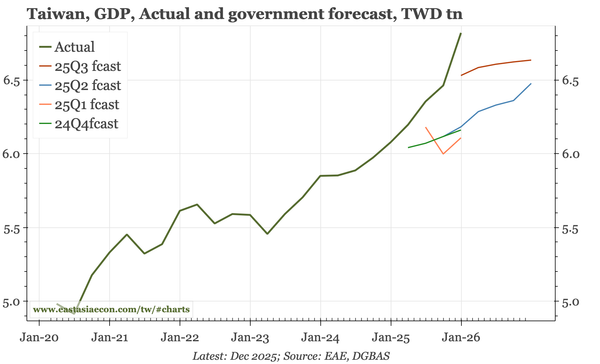

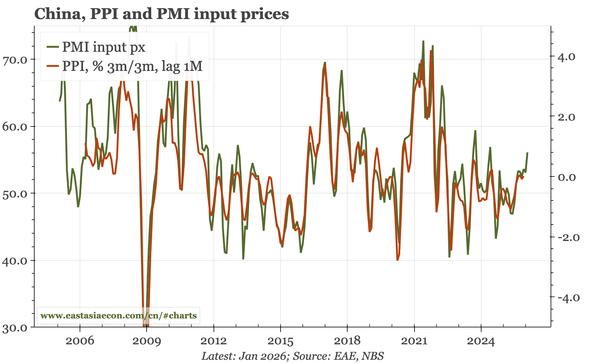

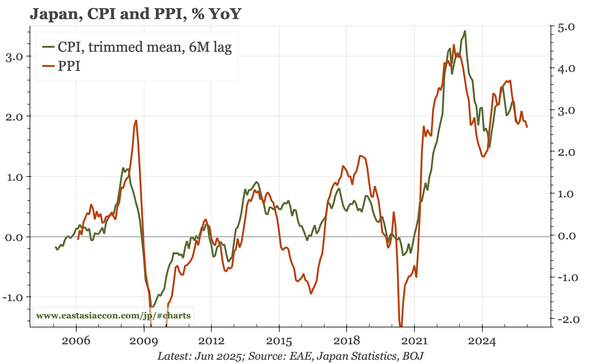

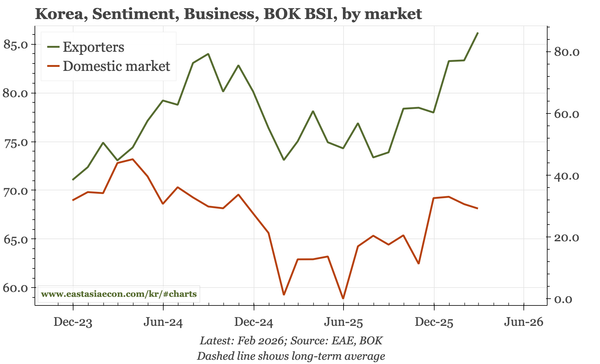

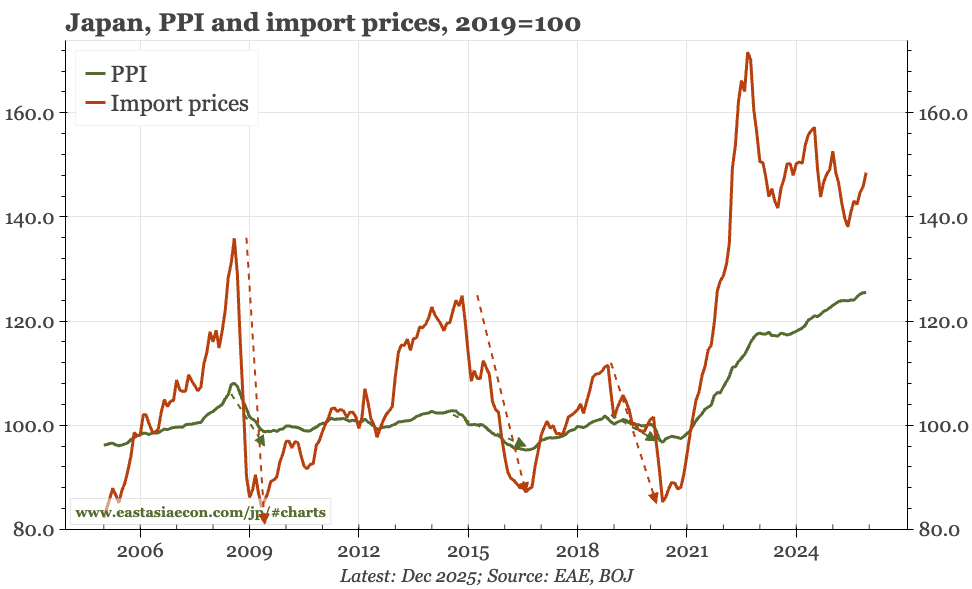

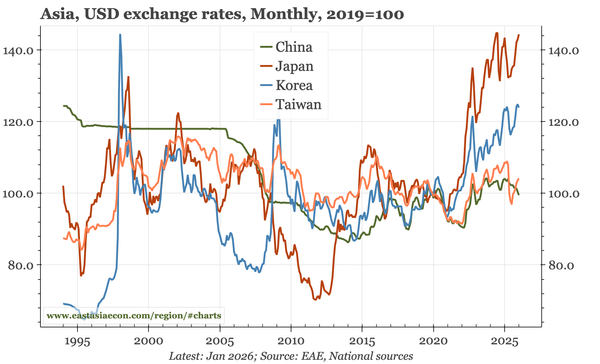

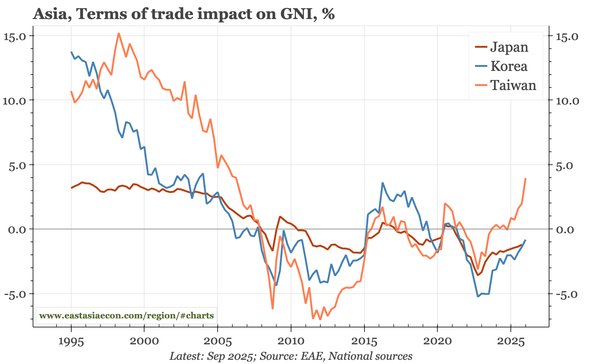

Three themes from last week: improving terms of trade, led by rising export prices; expanding current account surpluses; and growing optimism about the sustainability of AI-related hardware demand that is critical for cycles in Taiwan and Korea. Also, happy year of the (fire) horse.