Subscribers Only

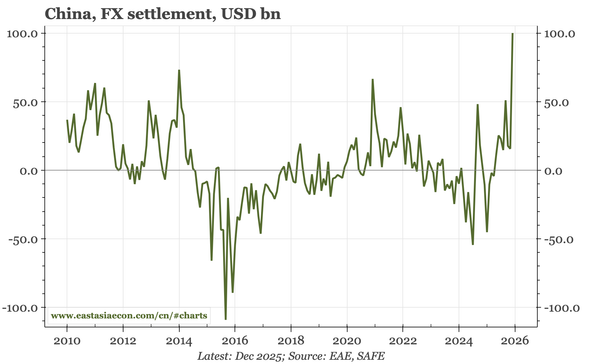

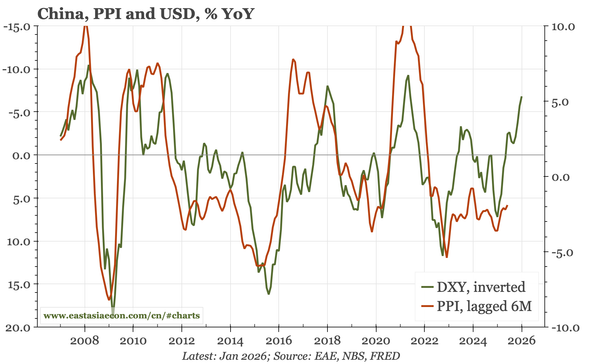

China – domestic so-so, external go-go

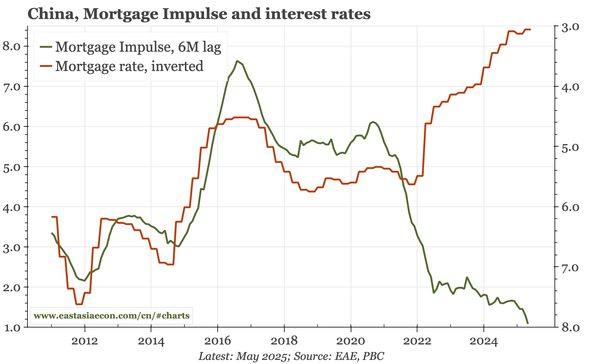

Some of the signs of domestic stabilisation I'd been tracking in 2025 faded into year-end. However, they didn't disappear entirely. China is also starting to benefit from the global tailwinds of weaker USD and rising commodity prices, creating upside risks for China's nominal cycle.