East Asia Today

Lots today: no-change inflation data in China, a strong sakura regional report from the BOJ, Taiwan's foreign trade showing peaky exports but strong capital goods imports, and evidence that the strong rise in nominal GDP growth is boosting tax revenues in Korea.

Thematic – the upside risks to inflation. My latest video, discussing why inflation risks won't end even if the Iran War eventually does. The reasons: both cost-push and demand-pull from the semiconductor boom, dynamics that are being reinforced by the cheapness of currencies.

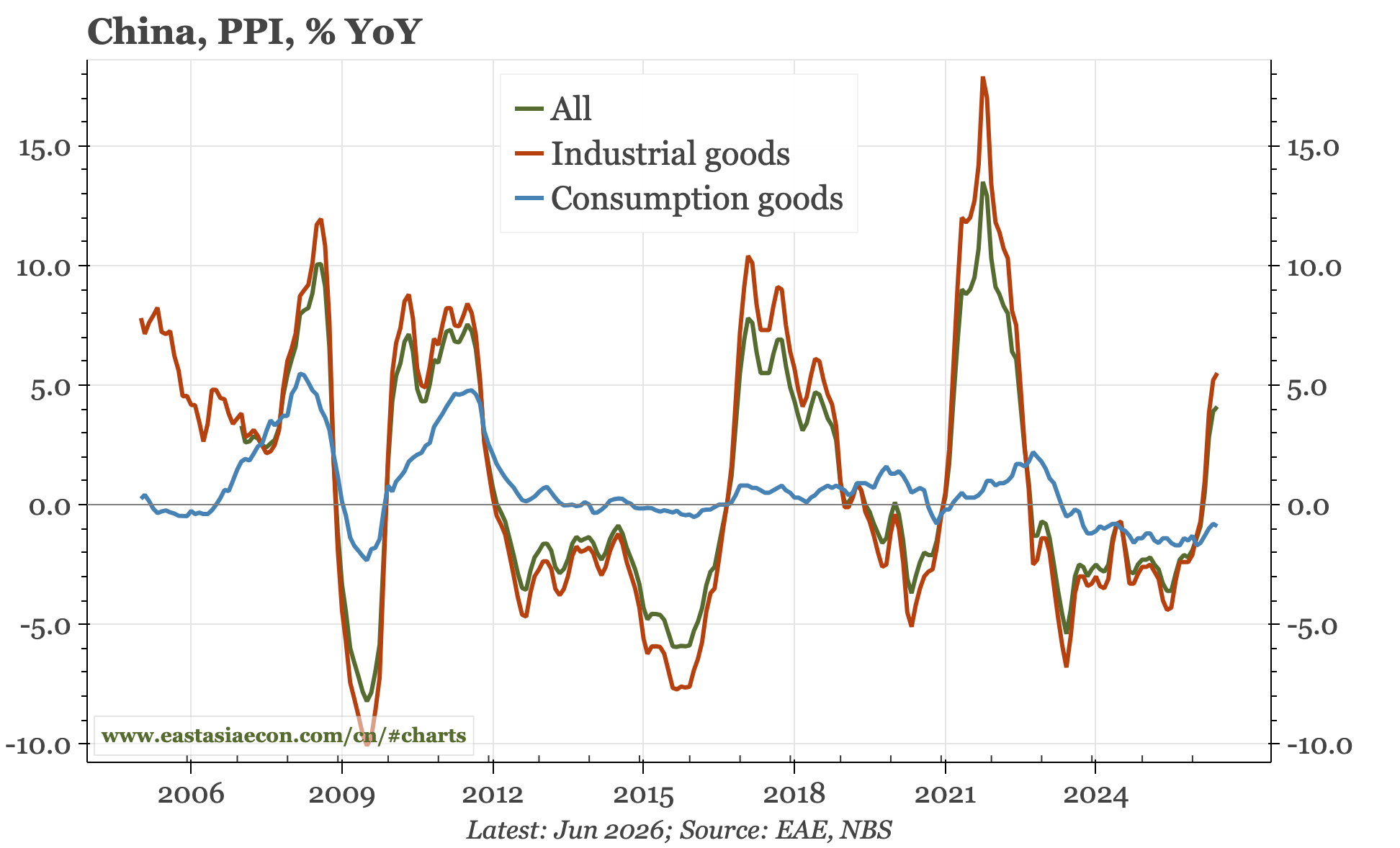

Cycle update – inflation peak. Average CPI and PPI inflation remained relatively elevated in June. However, most of the rise has been because of external factors, and leading indicators show that for now, the peak has likely been seen.

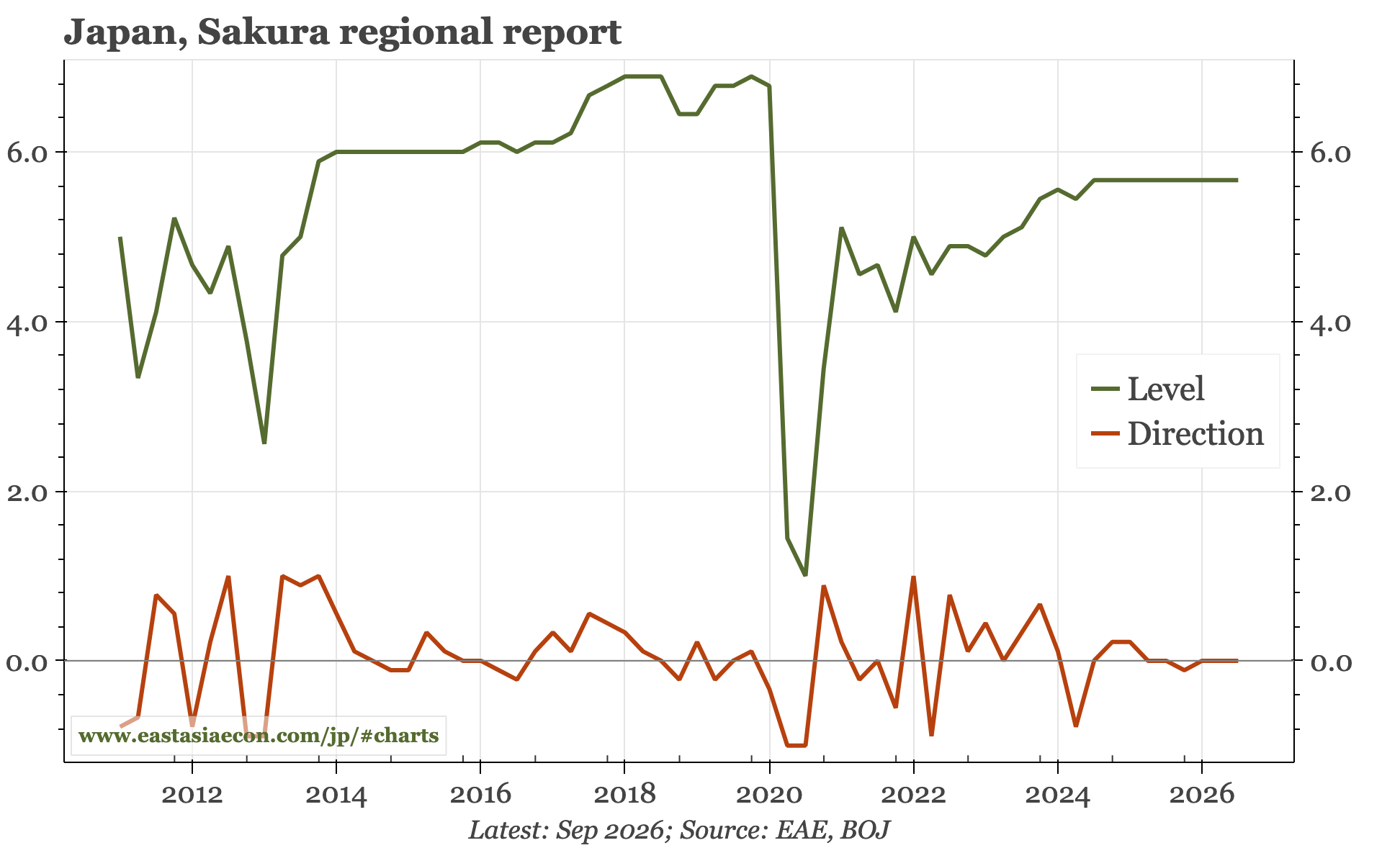

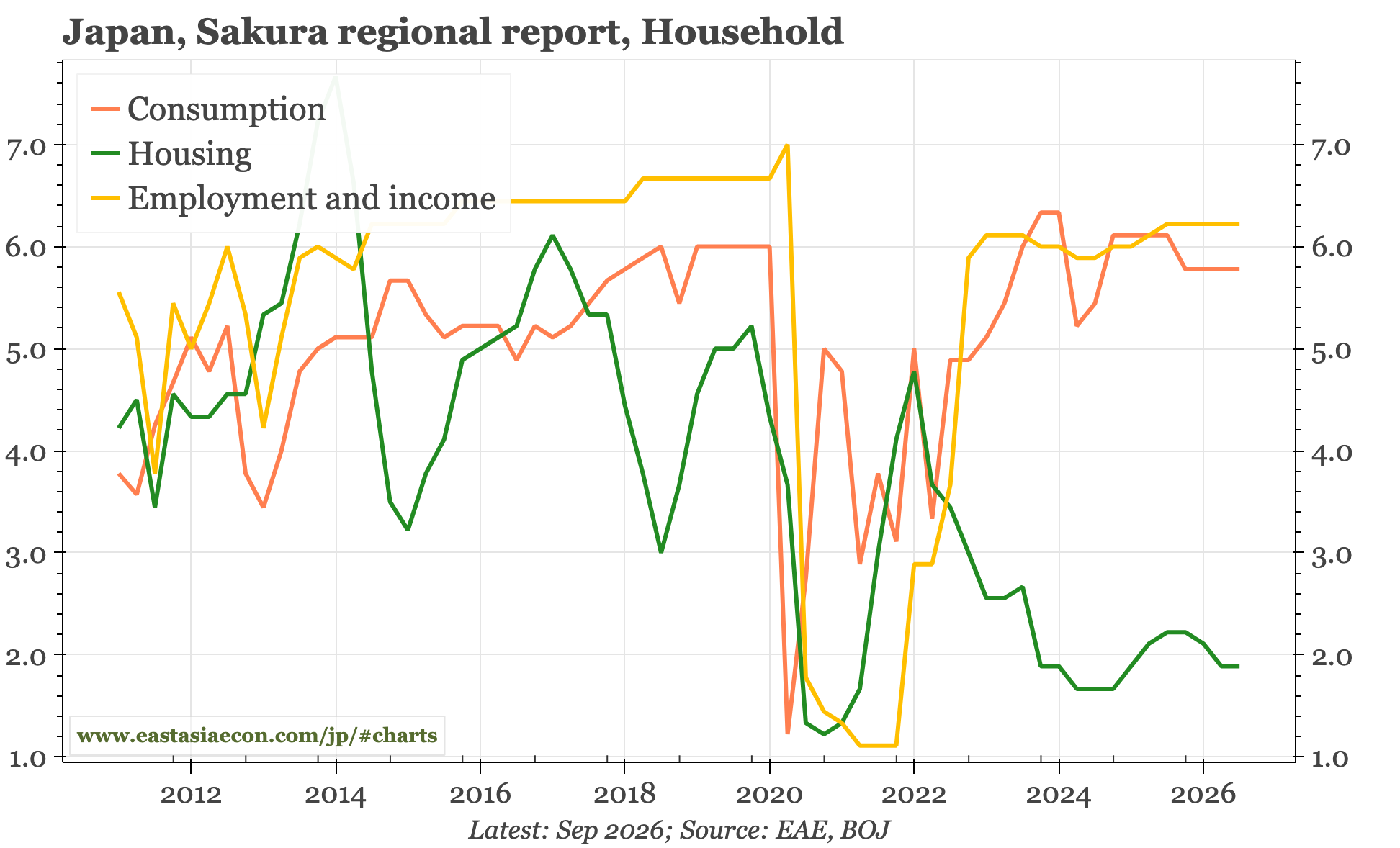

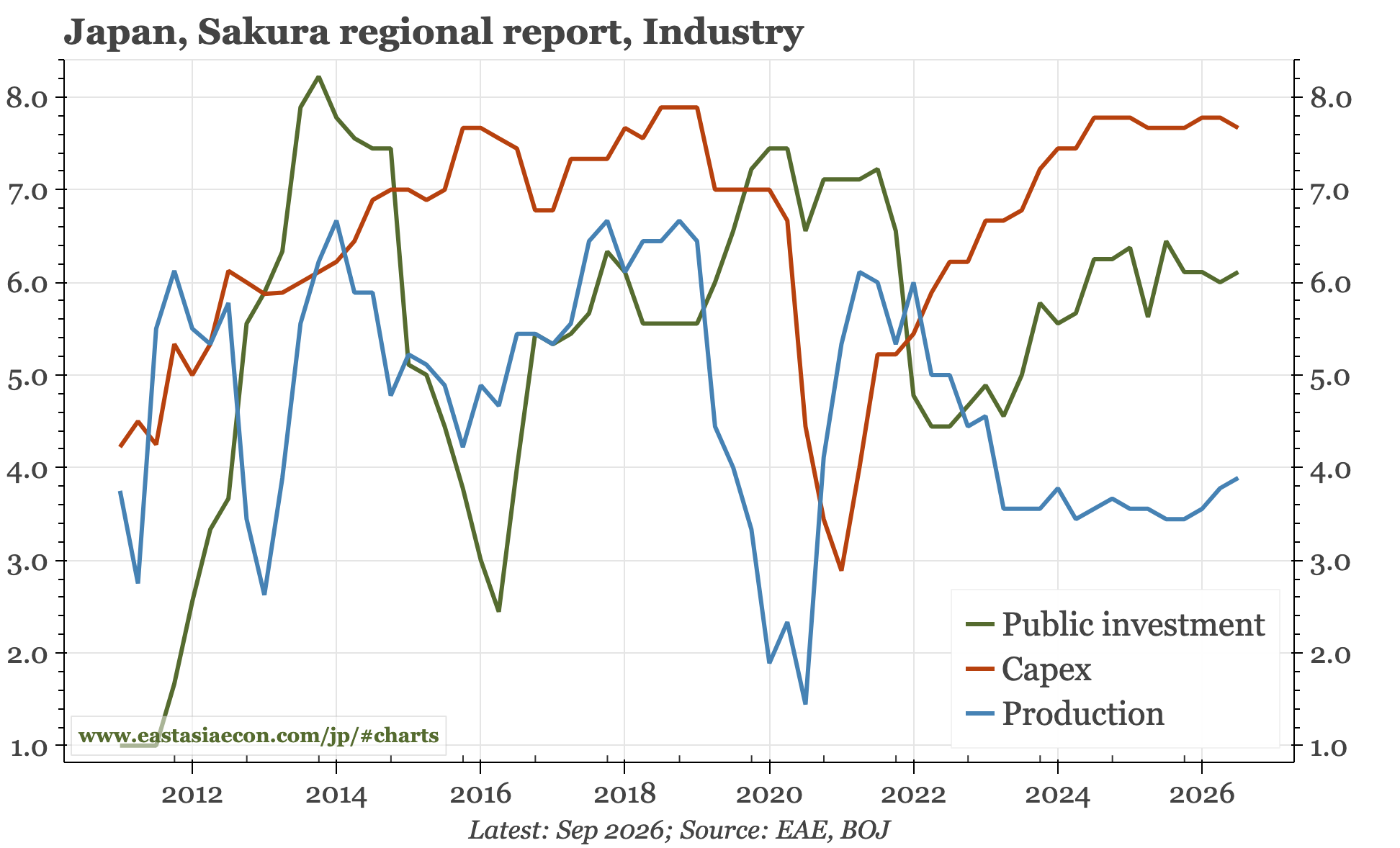

Recent data releases have pointed to a strengthening of both the cycle and inflation in the next few months. Today's sakura regional report from the BOJ sends the same message. According to the BOJ Osaka branch manager who spoke at a press conference, "We might see significant price rises judging from the way price rises have continued for the past few years". On growth, one company was quoted in the report as saying "US demand for products used in AI data centres is so strong we revised up our estimates several times".

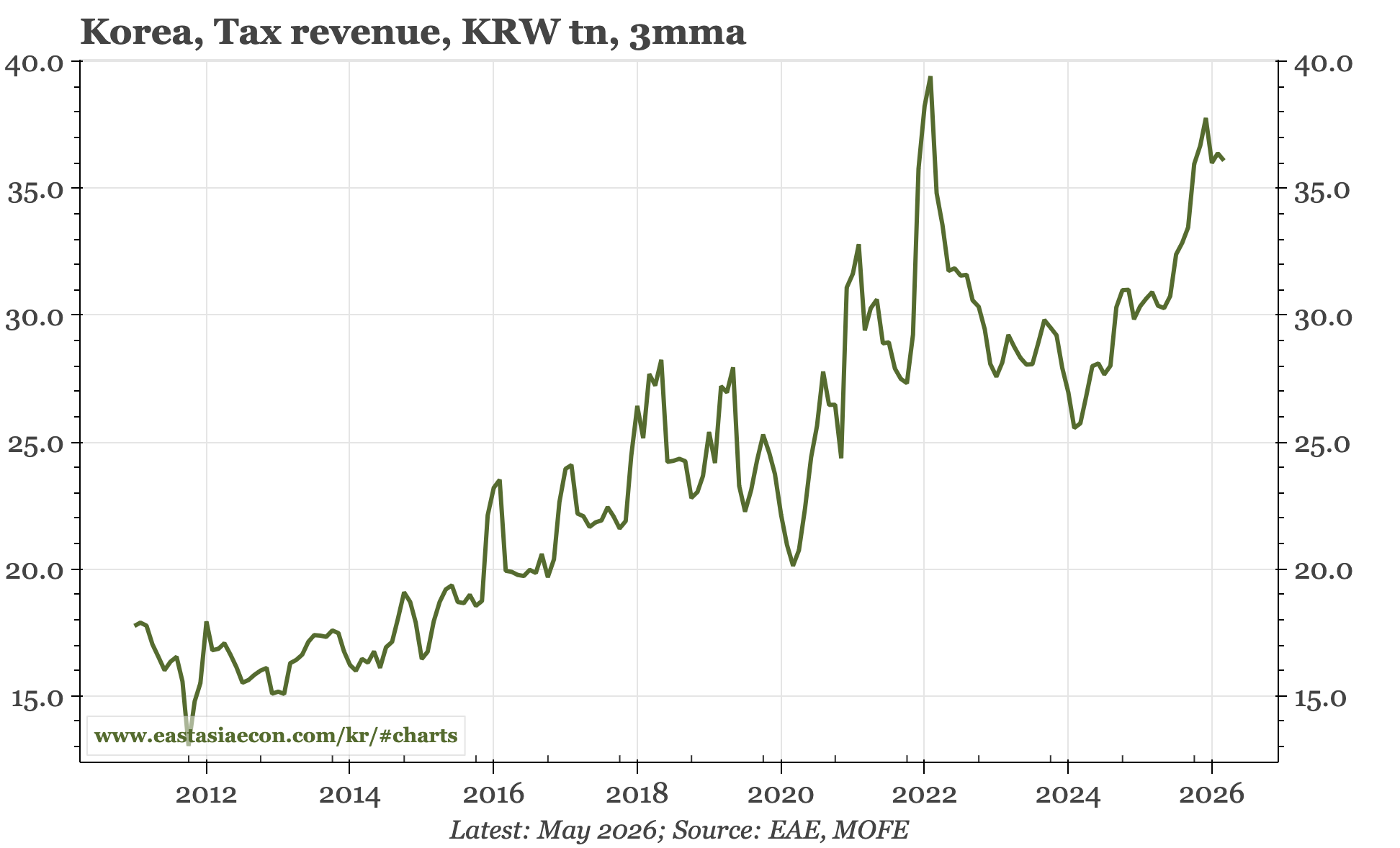

Fiscal policy is one mechanism by which the big increase in national income produced by the semiconductor boom can lift the wider economy. Data today show that tax revenues rose more than 17% YoY in the first five months of this year. According to today's press release (machine translated):

Income tax increased by KRW3.1tn, driven by an increase in capital gains tax due to capital gains from overseas stocks and an increase in housing transaction volume, an increase in earned income tax due to an increase in the number of employed persons and total salary payments

Securities transaction tax increased by KRW1tn due to the increase in securities trading volume, tax rate reversal

Corporate tax increased by KRW0.7tn due to factors such as an increase in instalment payments reported by December-closing corporations following improved corporate performance, and an increase in withholding tax on dividends

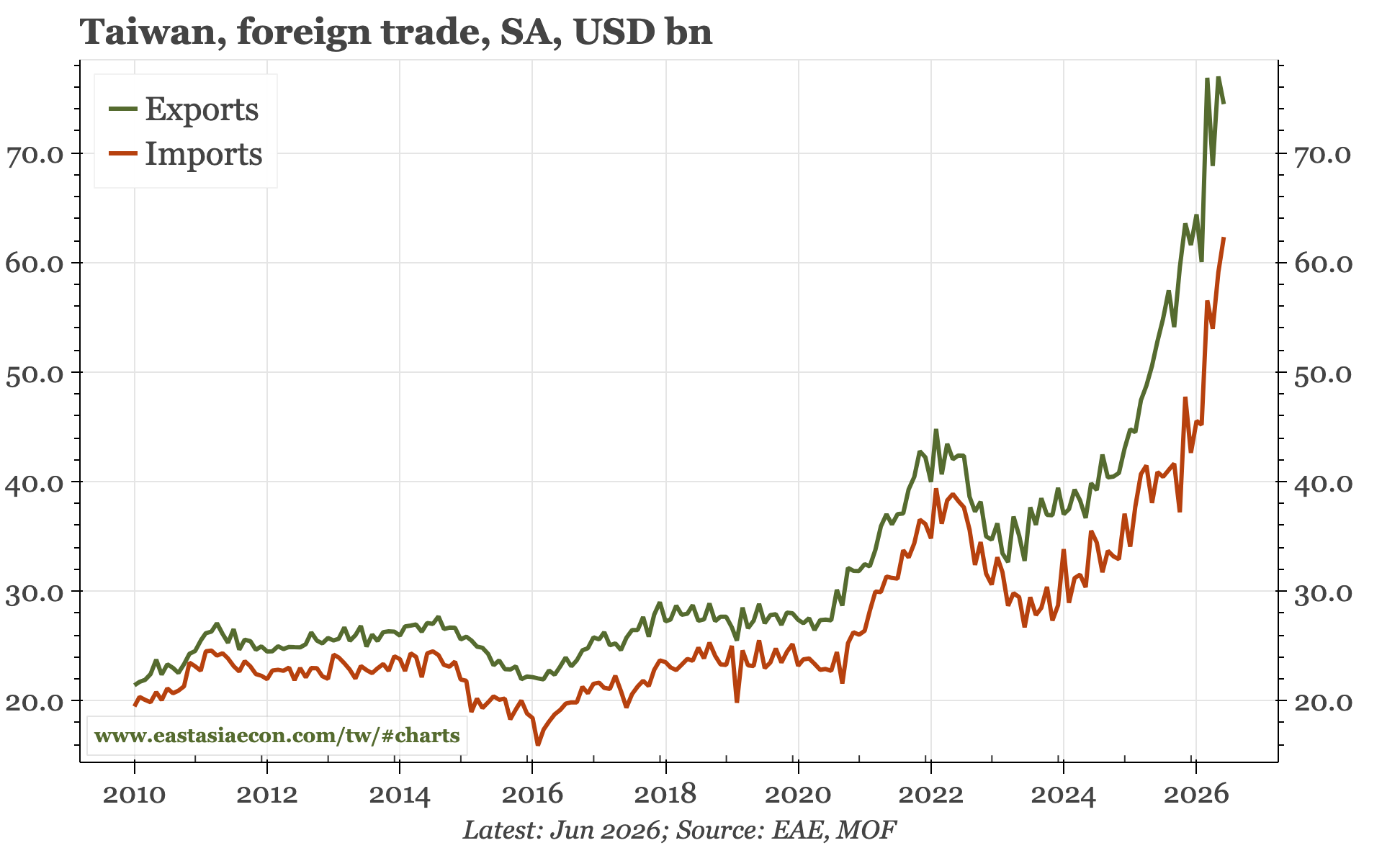

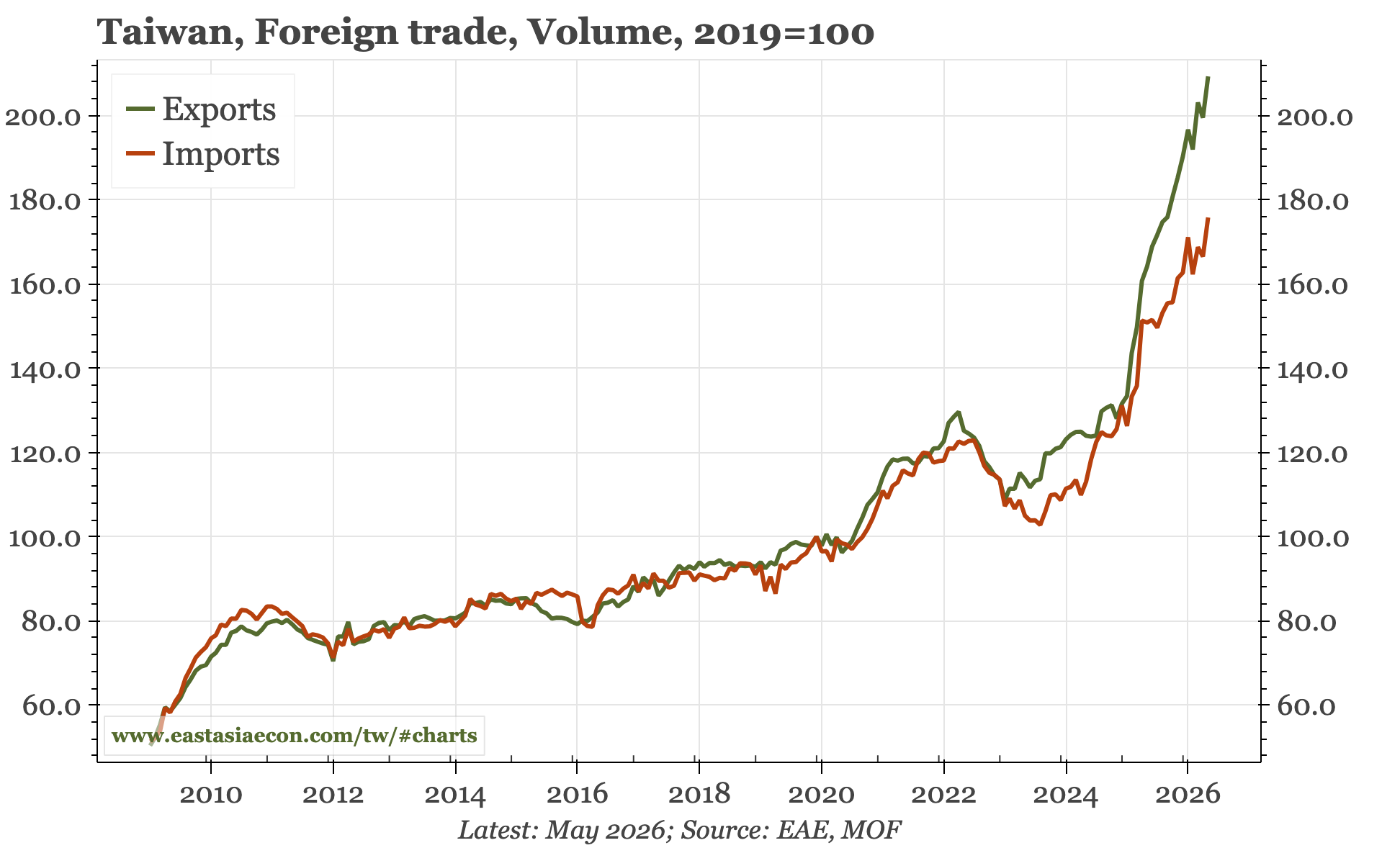

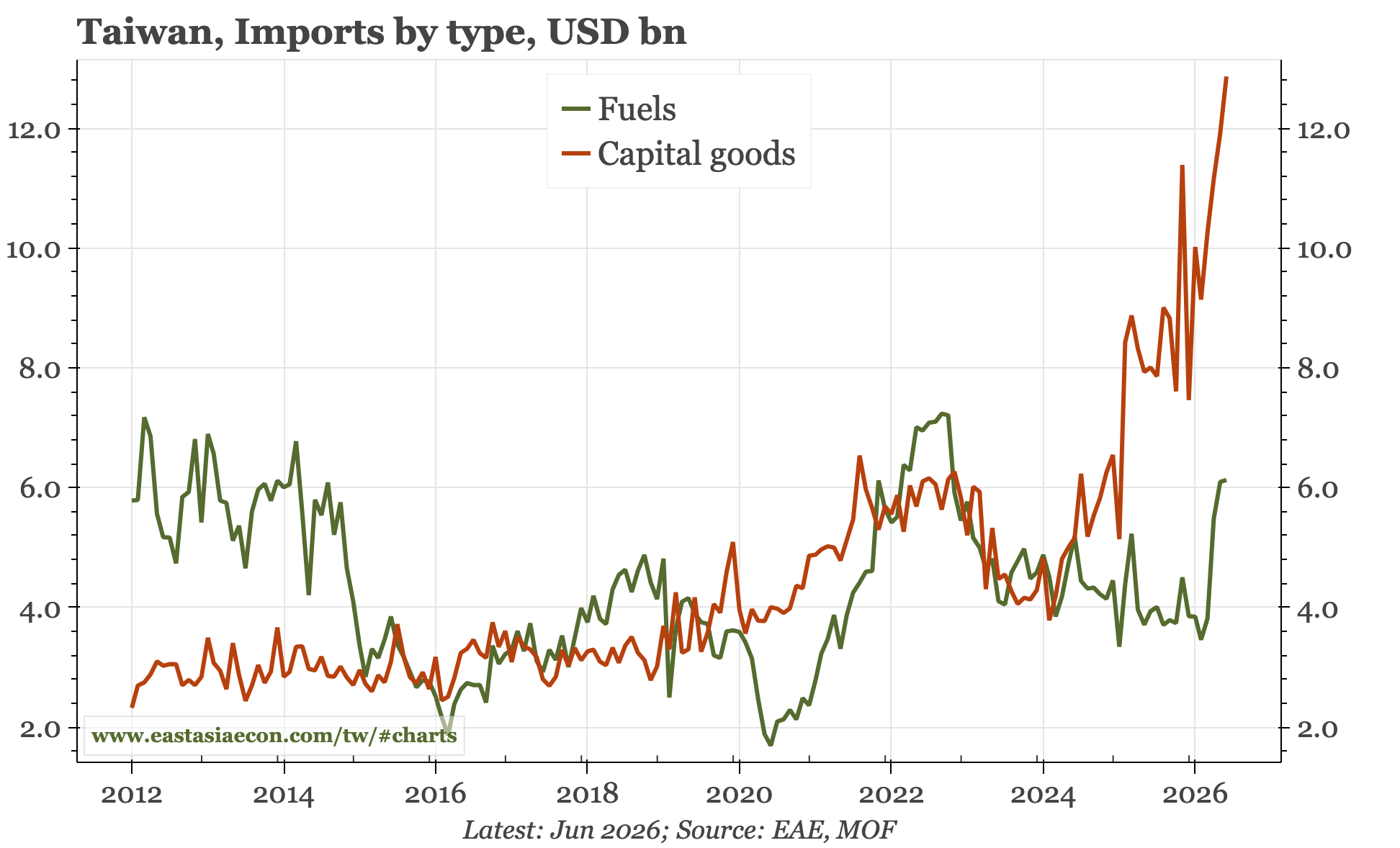

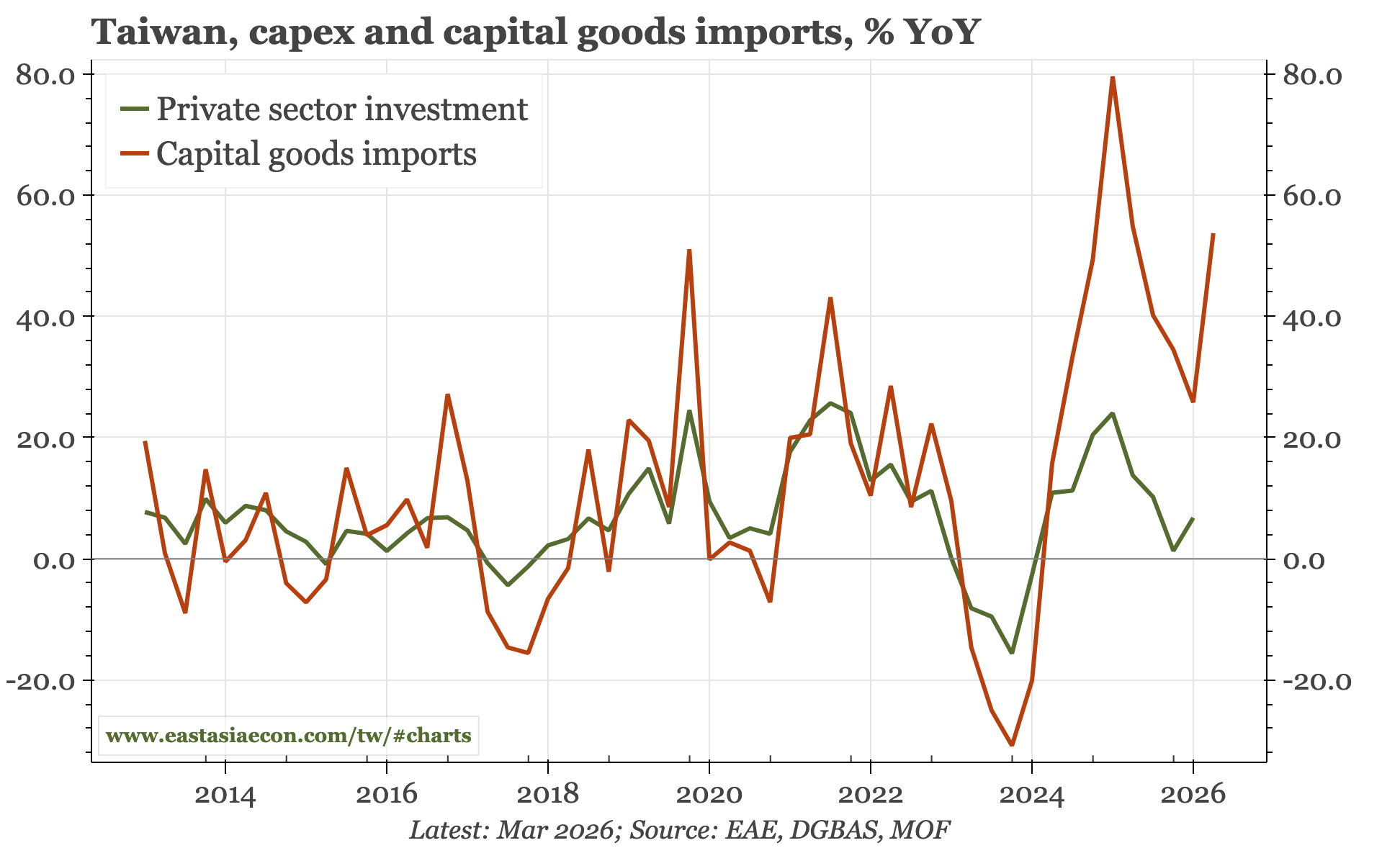

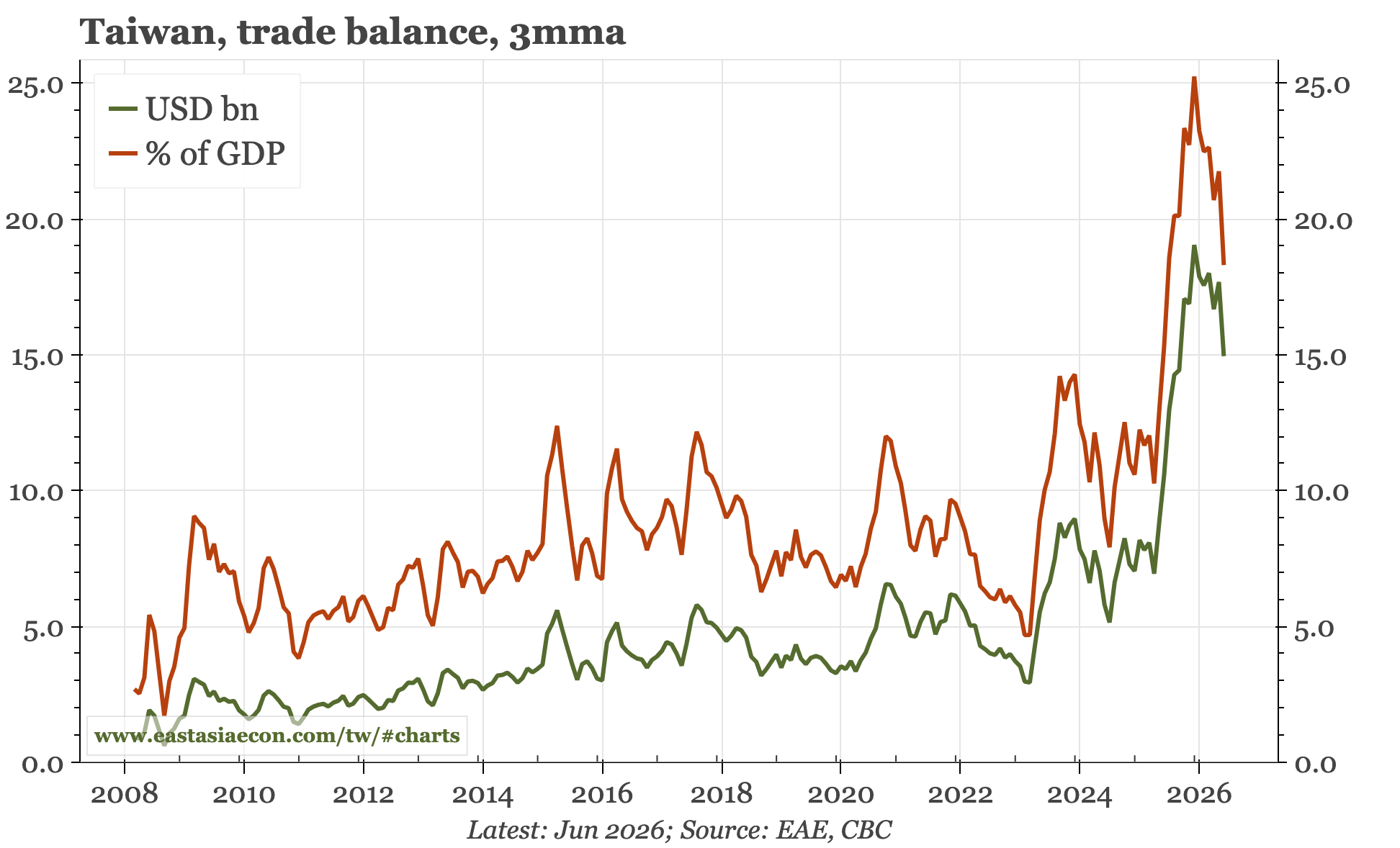

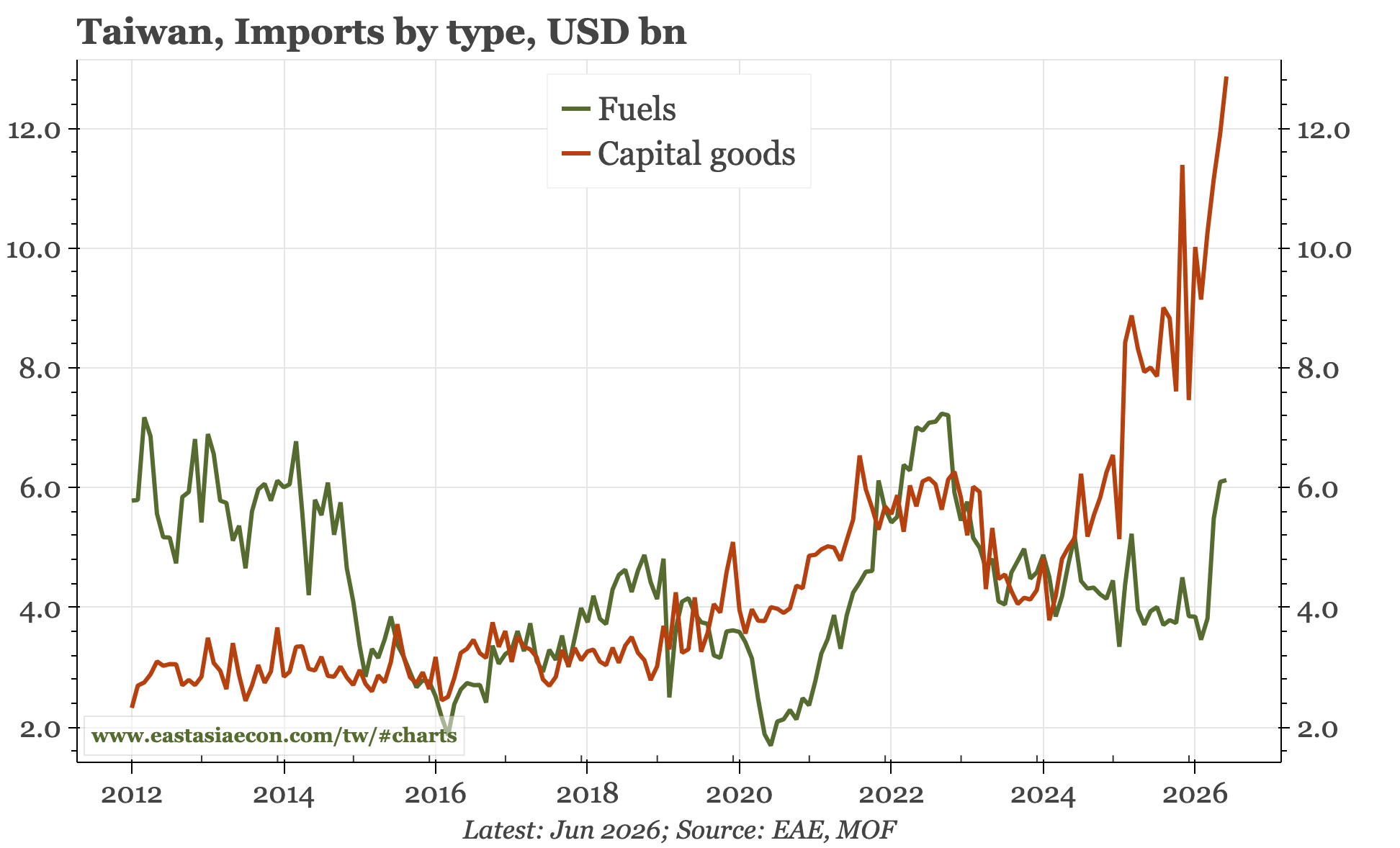

The surge in Taiwan's exports has finally started to lose momentum over the last few months. Some of that, however, is because of prices: volume data (through May) has remained strong. At the same time, while exports look peaky, some of the momentum of GDP growth is switching to capex, with a big rise in capital goods imports in June. It is that, rather than energy, that pushed up the overall import bill last month, but the result is still that the huge trade surplus is starting to narrow.