East Asia Today

The big releases today were Japan CPI and trade for October and November PMIs, and Korean October PPI and exports for the first 20 days of November. Also, a longer note on Korean capital flows, and an update of the detailed trade data for China shown in our interactive dashboard.

If you aren't a subscriber yet, please consider becoming one. We have a comprehensive service for financial institutions, but also this daily summary and data products that are more suited to individuals.

Three messages from the detailed trade data for October that were released yesterday:

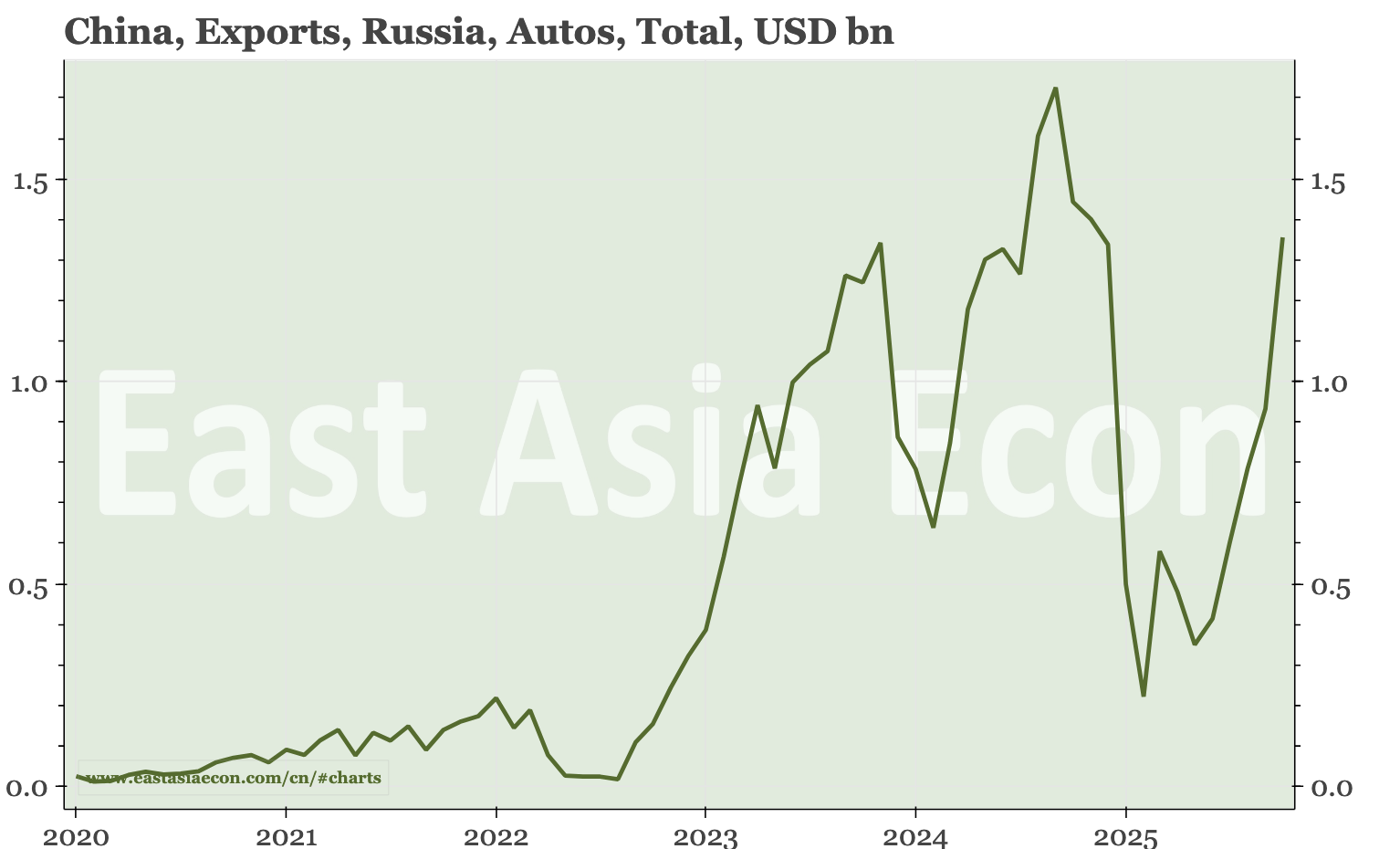

- Russia has once again become China's biggest auto export market. That pushes the mix of China's shipments more towards ICE: unlike Belgium (gateway to the EU and China's second-largest market), Russia imports very few NEVs.

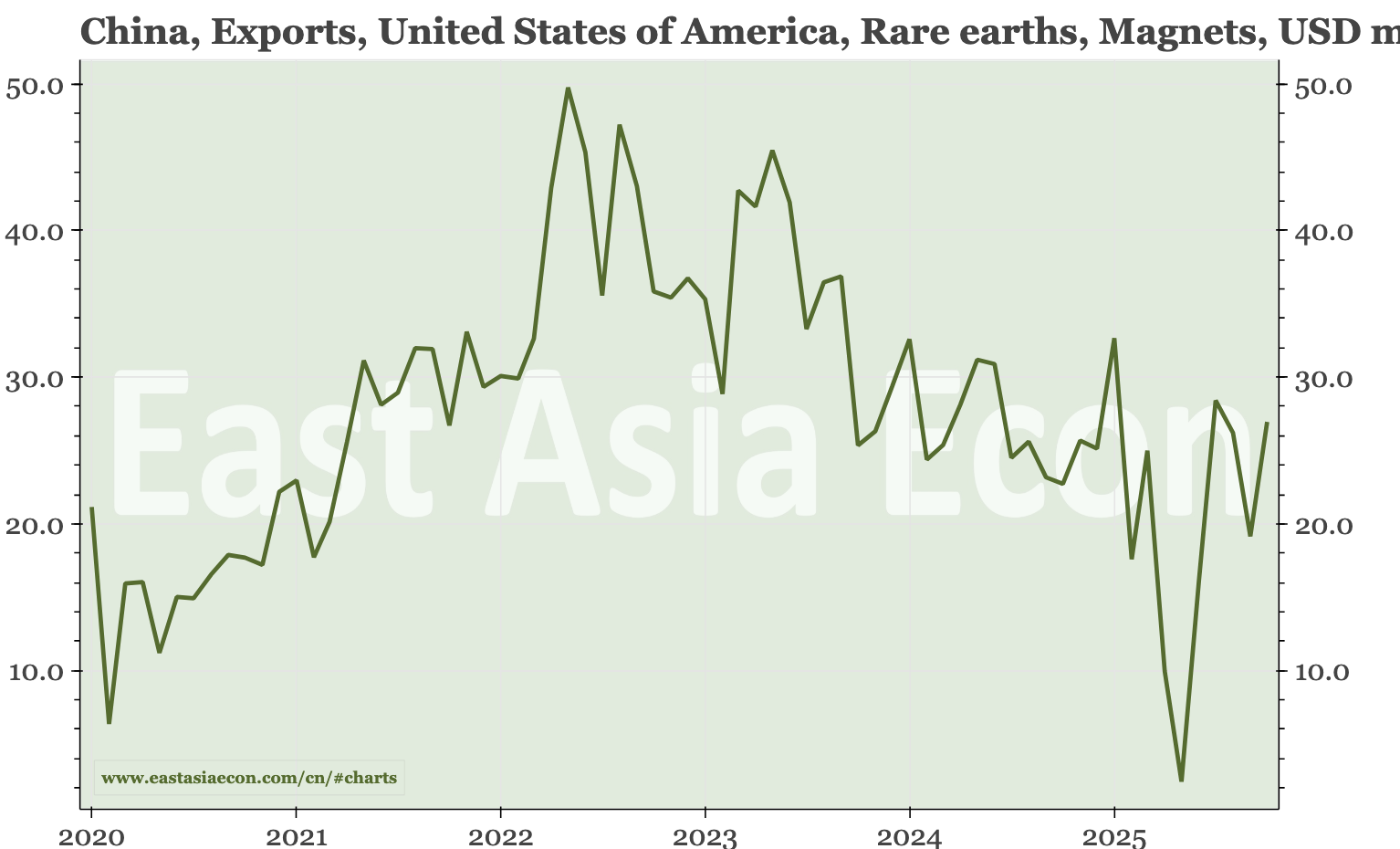

- The post-May normalisation of China's rare earth magnet shipments – to the world, and to US specifically – is continuing.

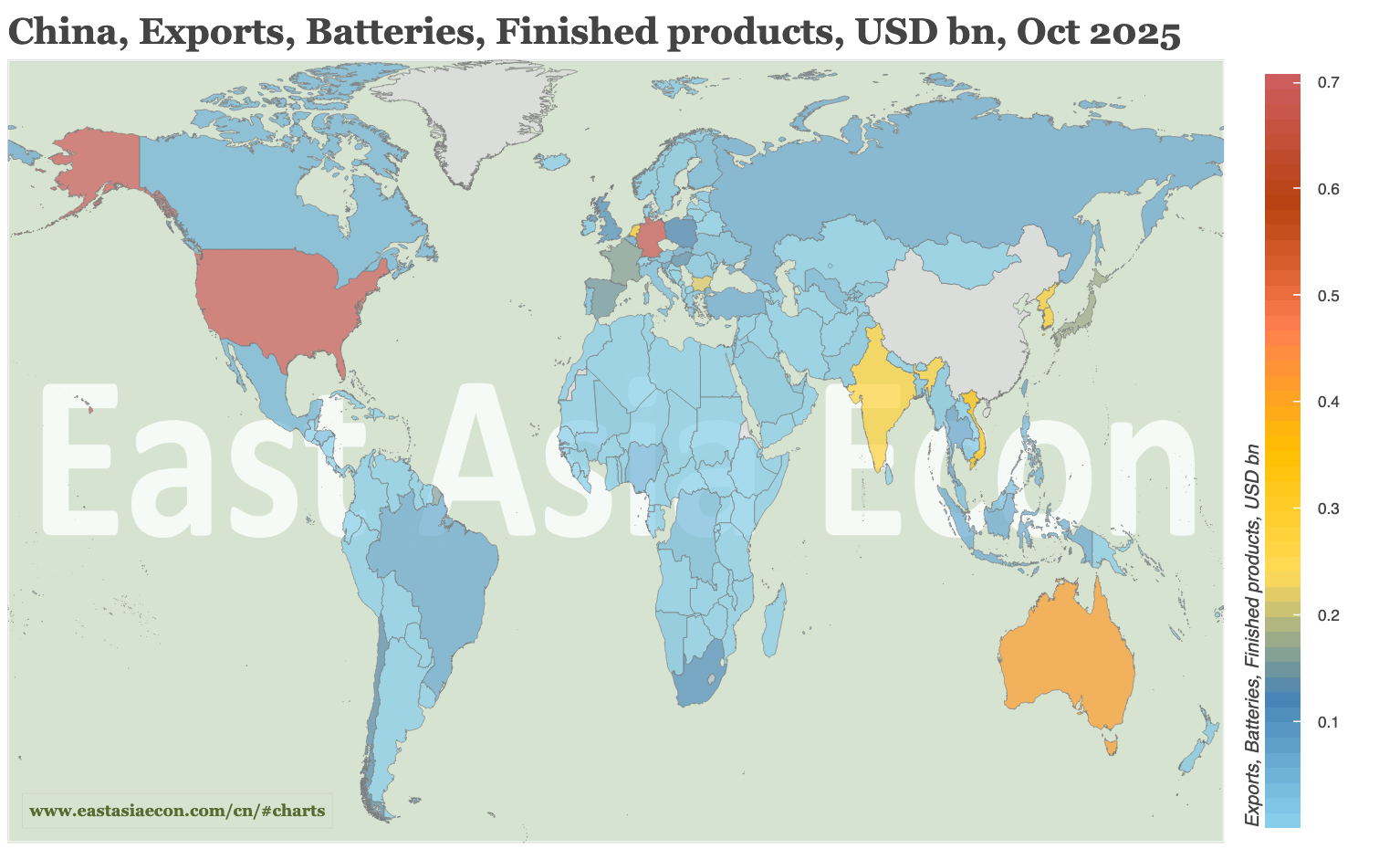

- Exports of lithium batteries eased a bit in October, but remain near record highs, with the biggest markets being the US and Germany.

You can use this dashboard to chart and map China's auto, rare earth and battery exports.

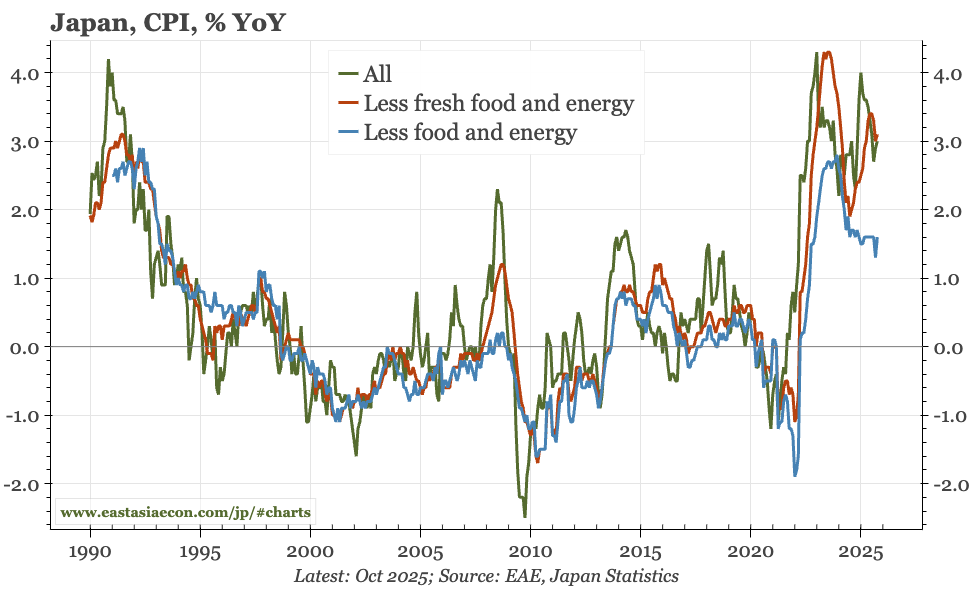

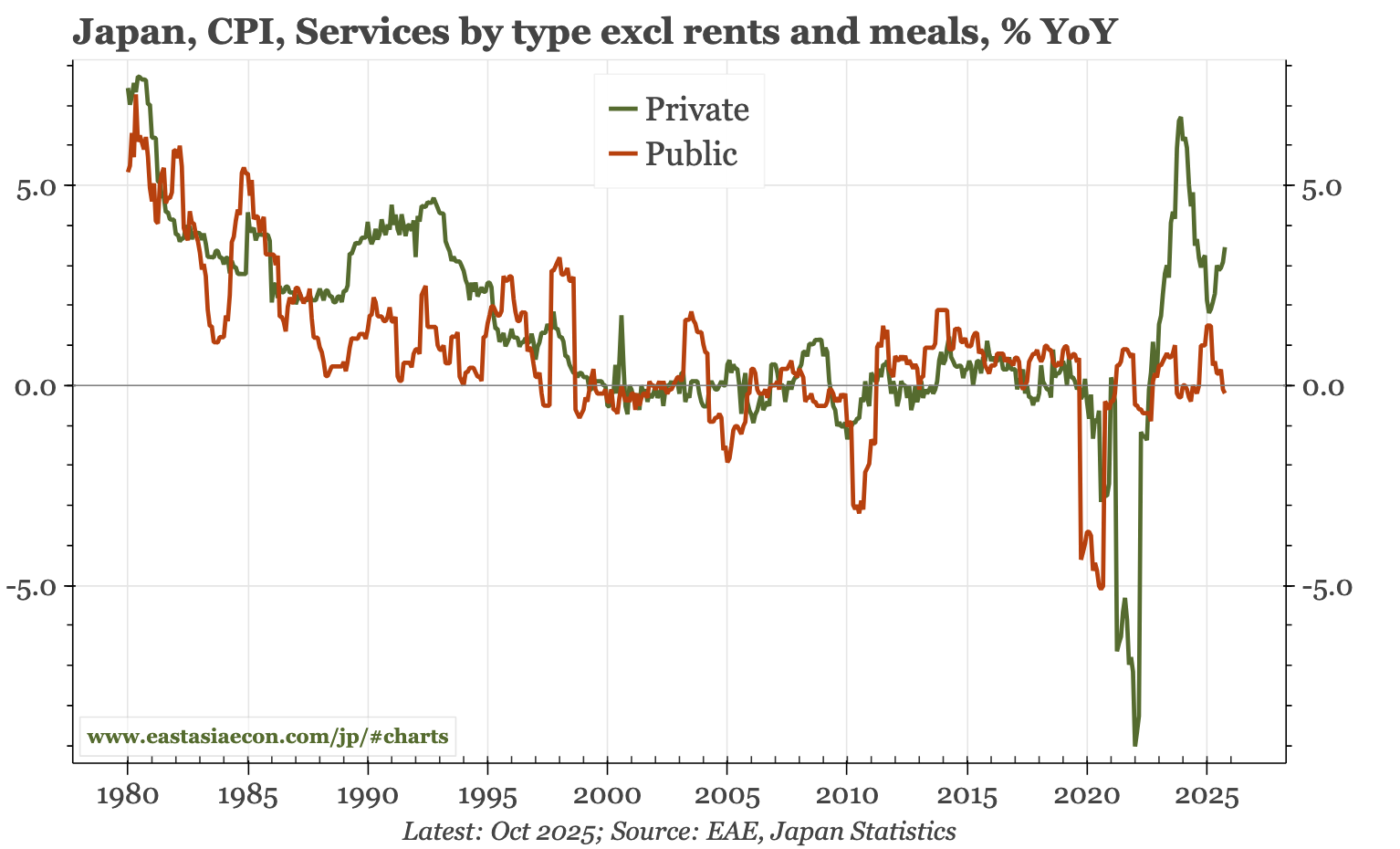

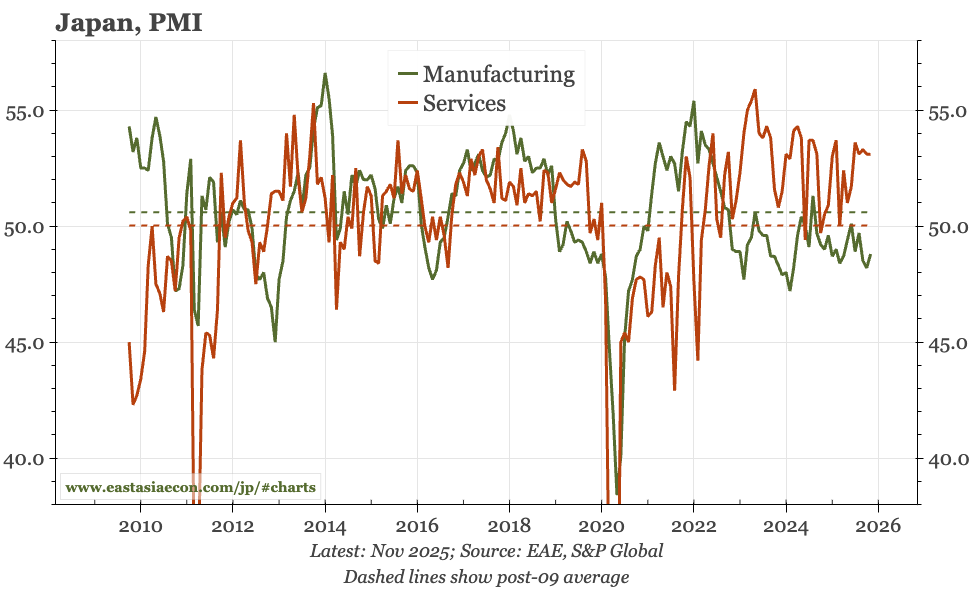

Cycle update – cycle and inflation still ticking the boxes. The BOJ's base case has been that tariffs would slow inflation and growth. Today's data – November flash PMIs, and October trade and CPI data – give no indication that such slowdowns are occurring.

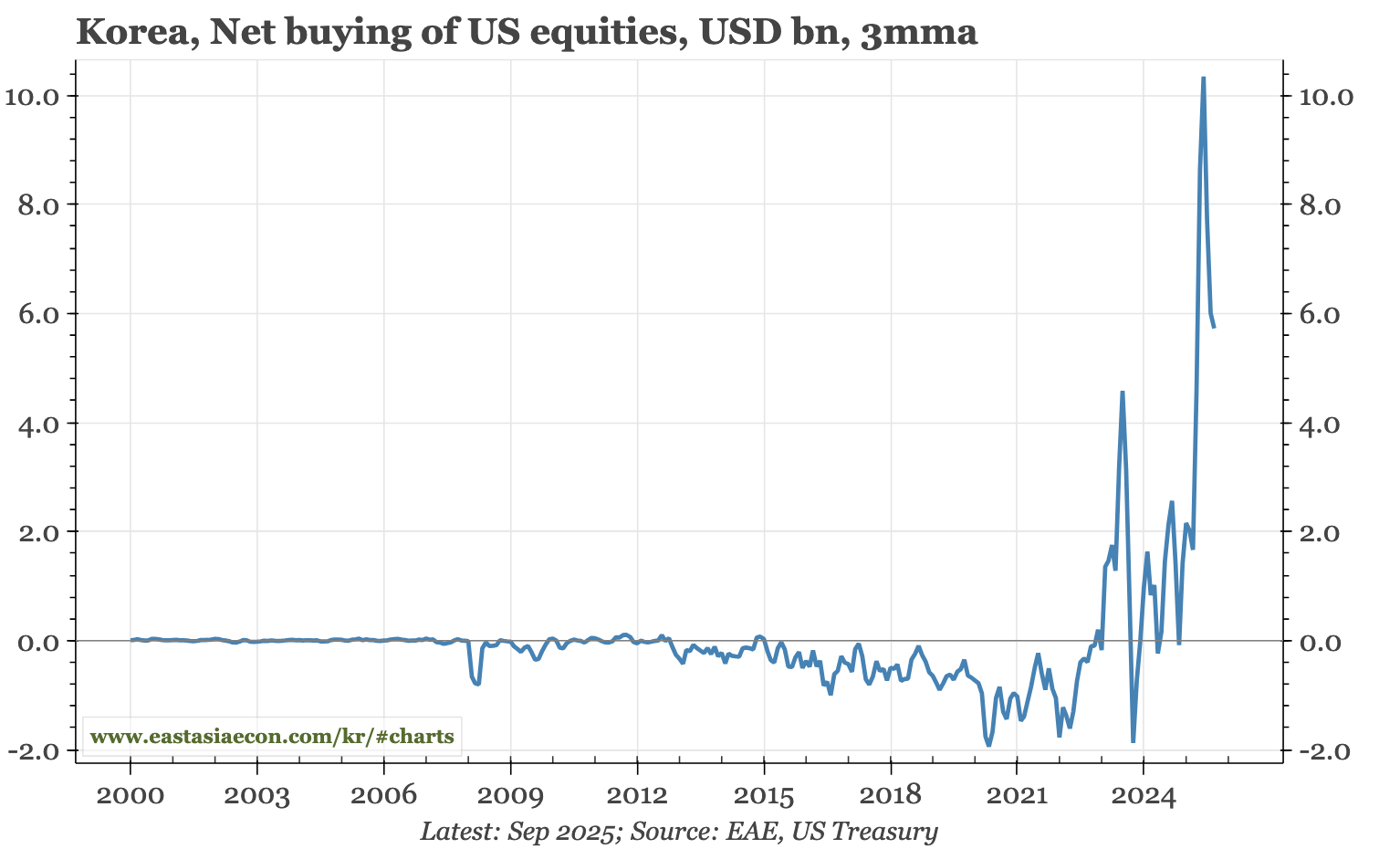

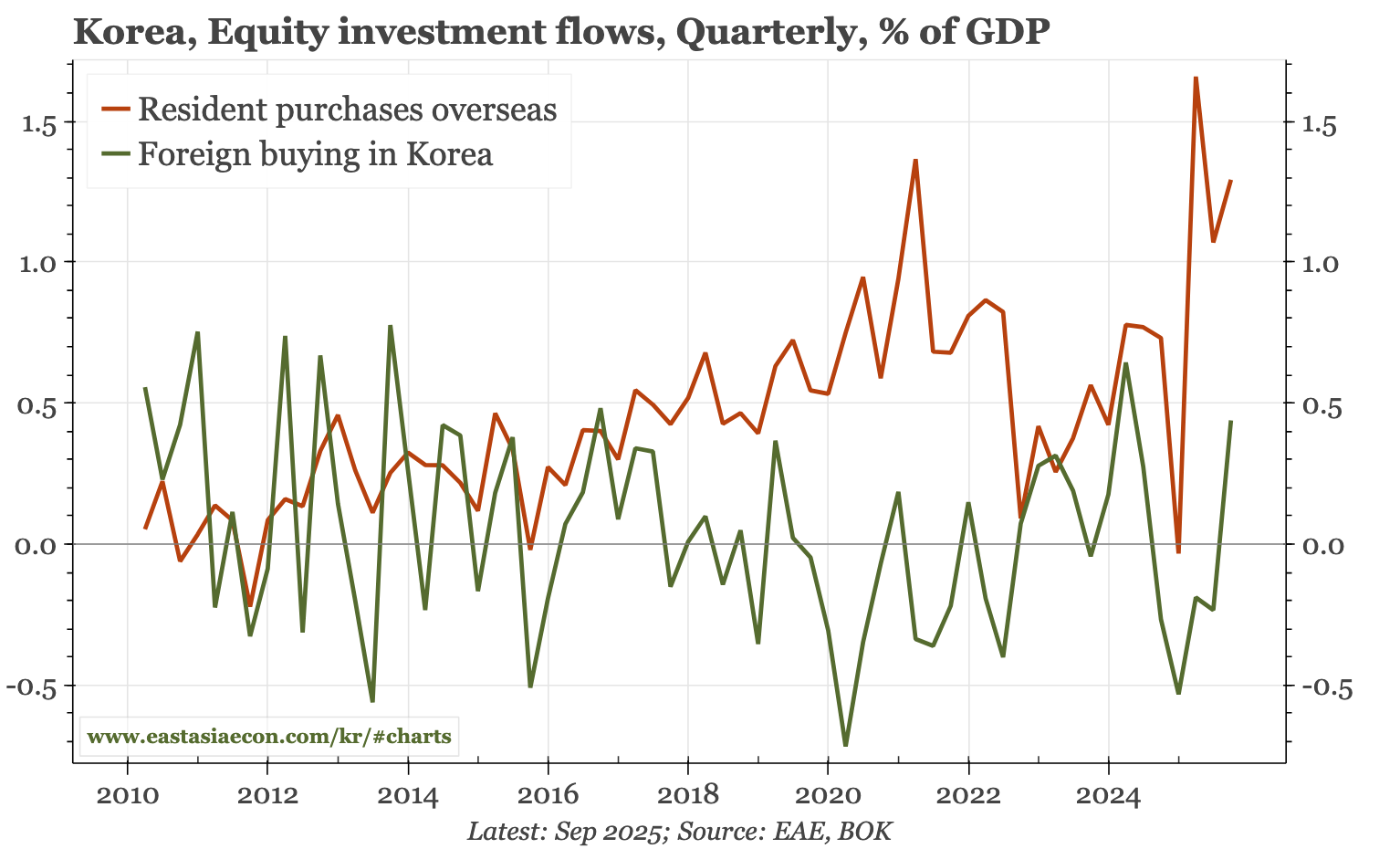

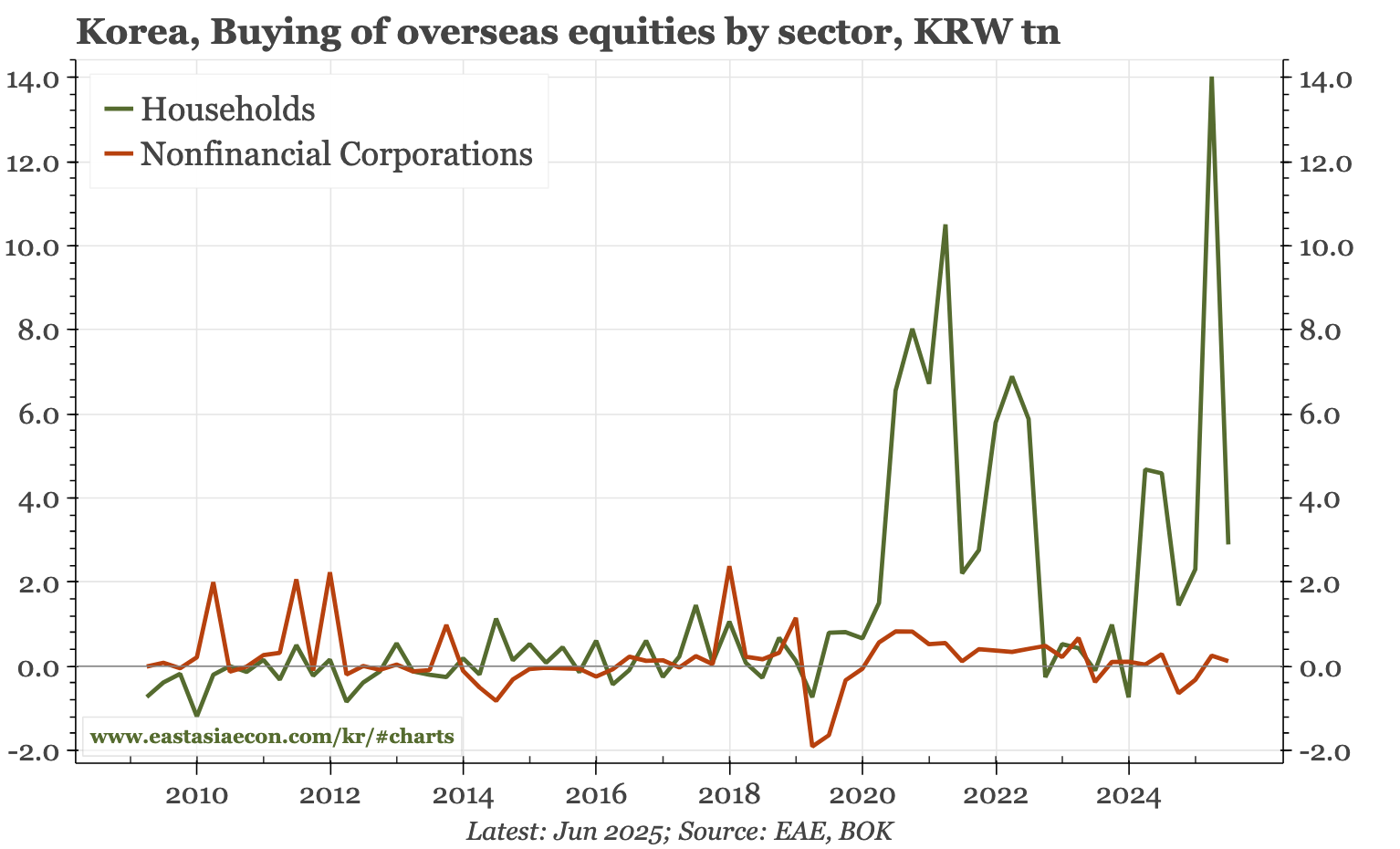

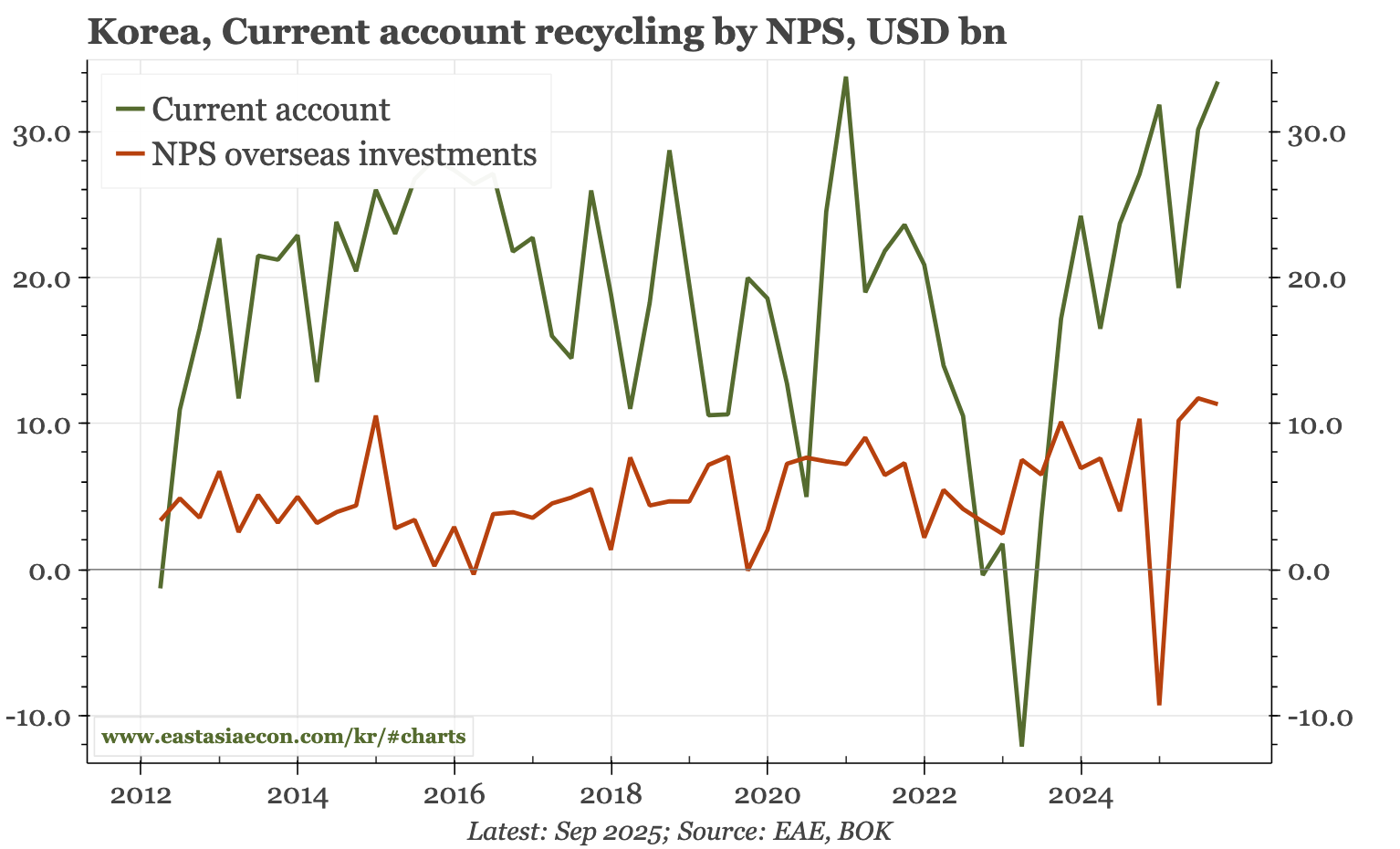

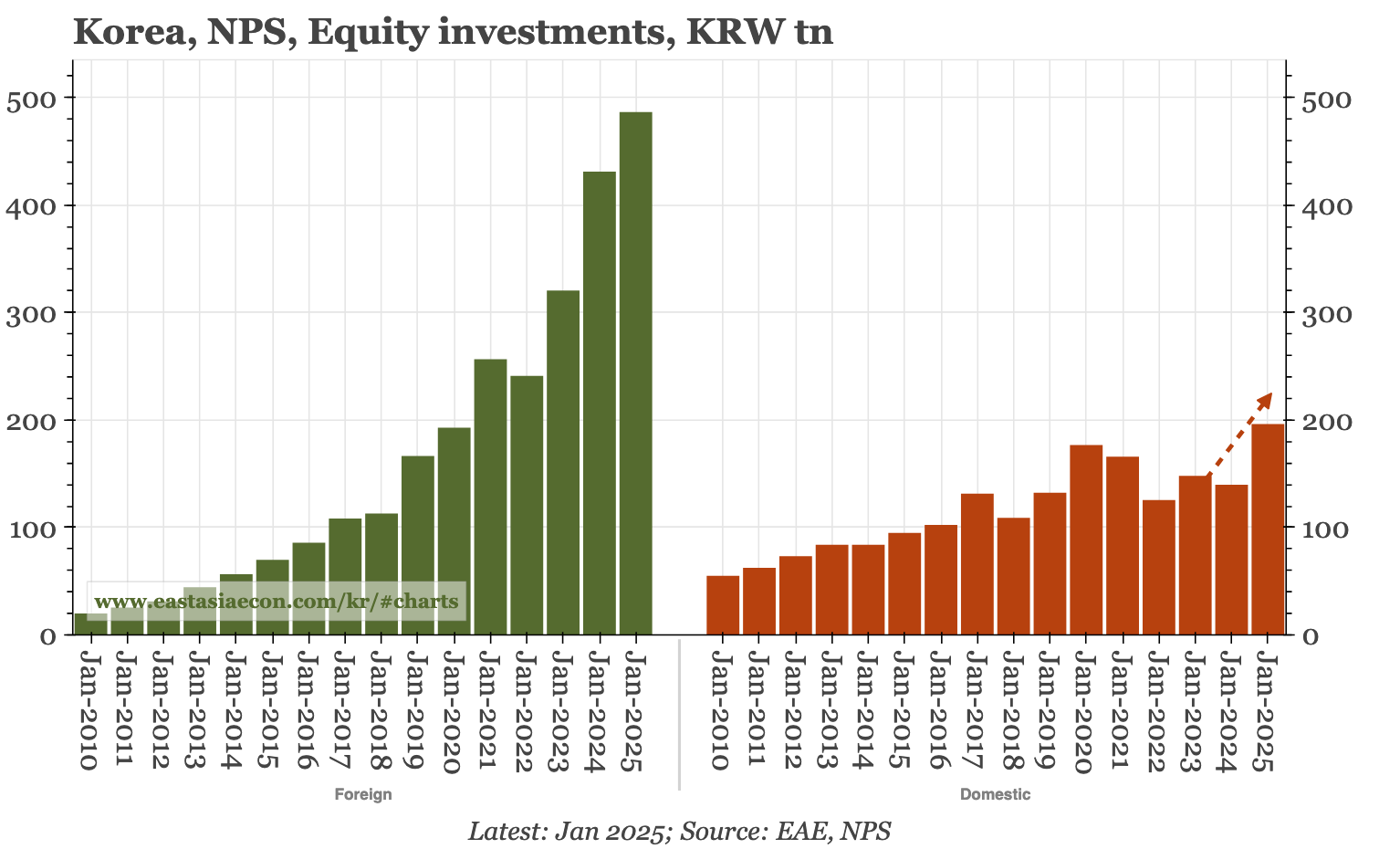

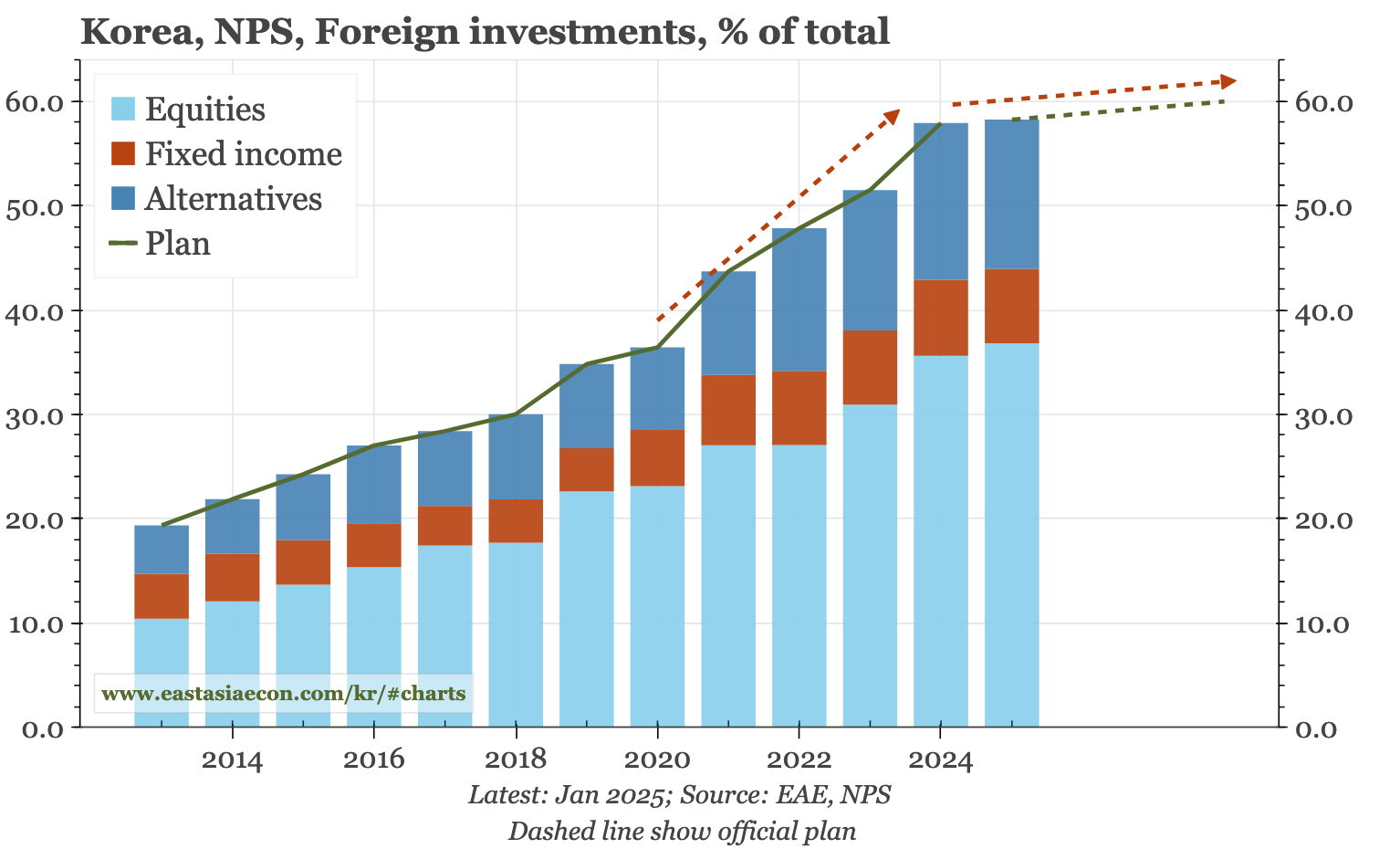

Thematic – household offshore equity buying and the KRW. Global factors like US rates and JPY weakness are dragging down the KRW. But there are also local drivers, particularly Korea's big buying of overseas equities. For both the NPS and households, I would expect that to slow, with the reversal likely to be sharp if global markets really sell off.

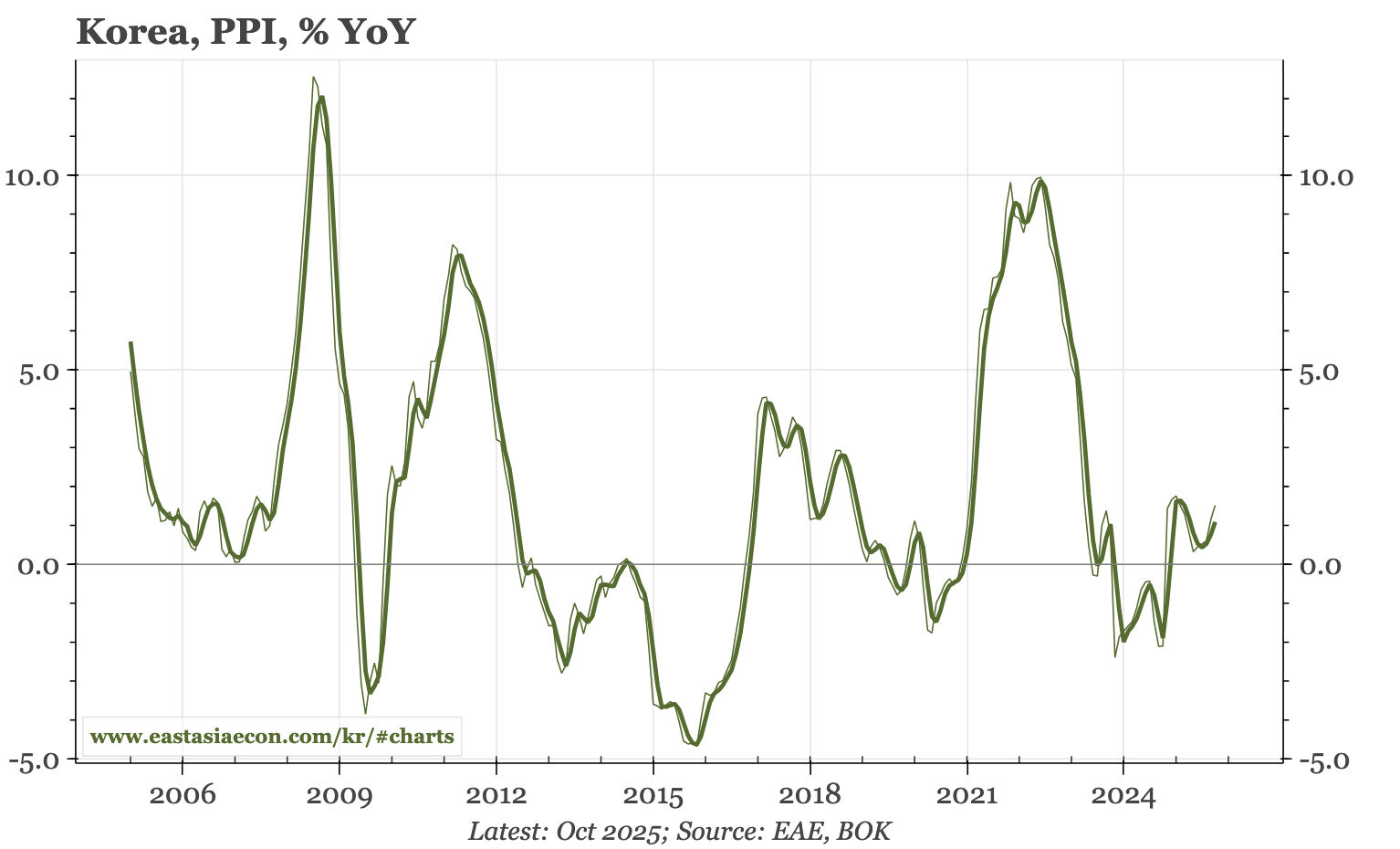

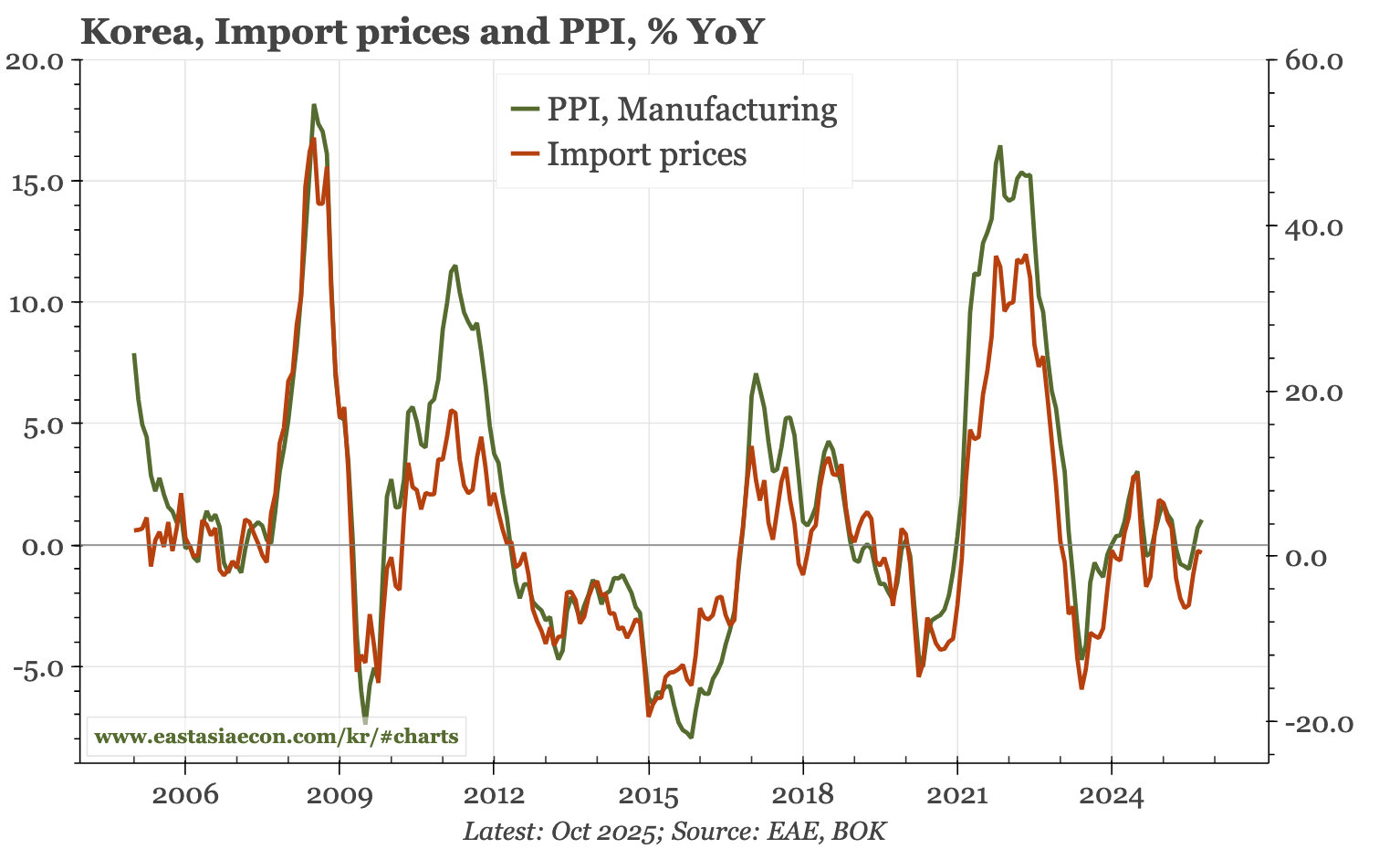

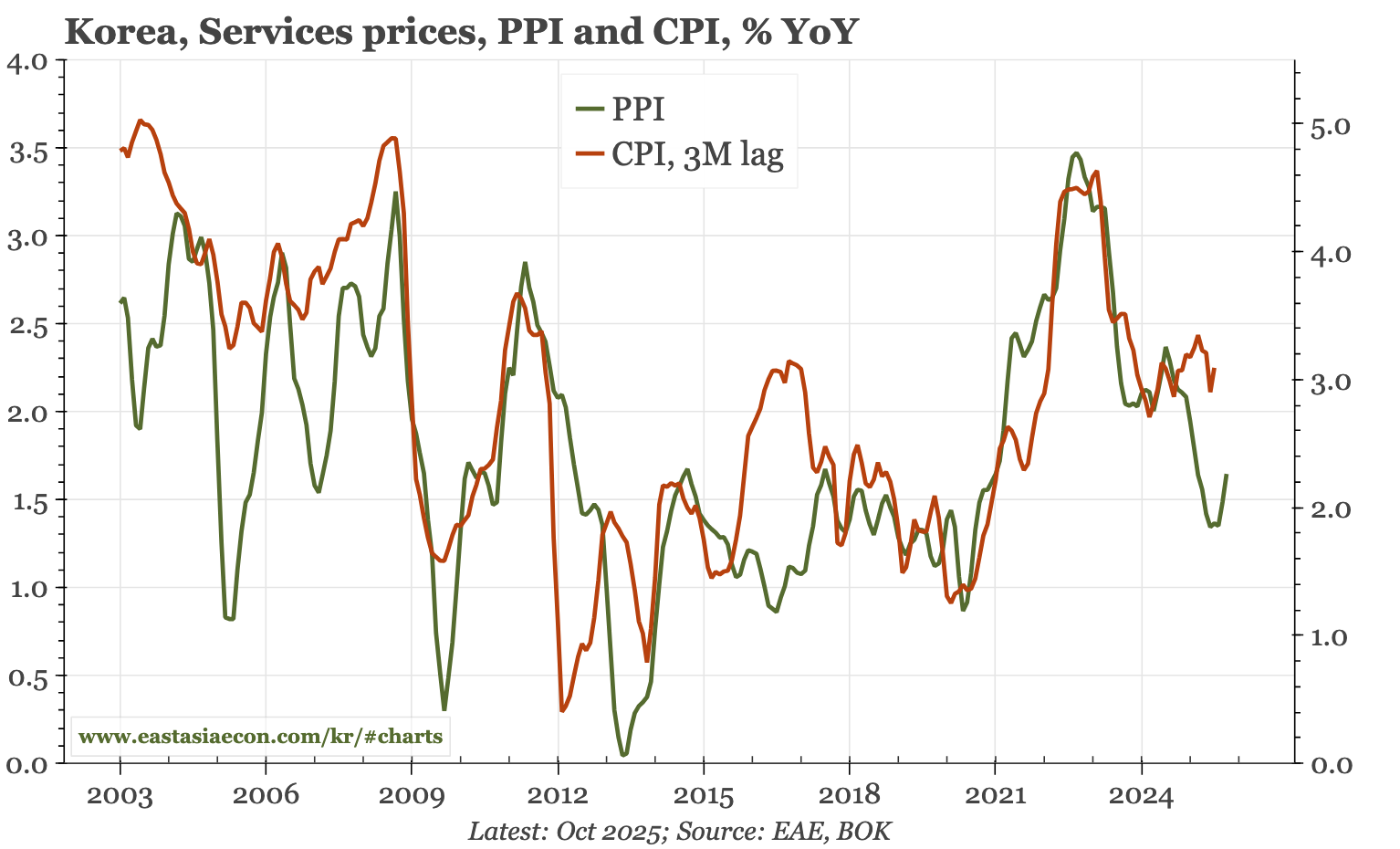

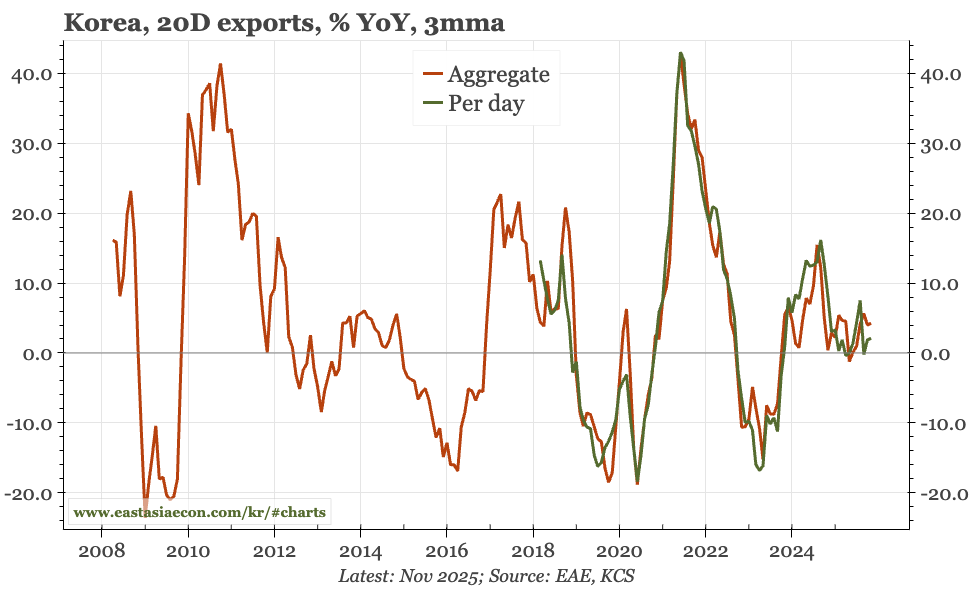

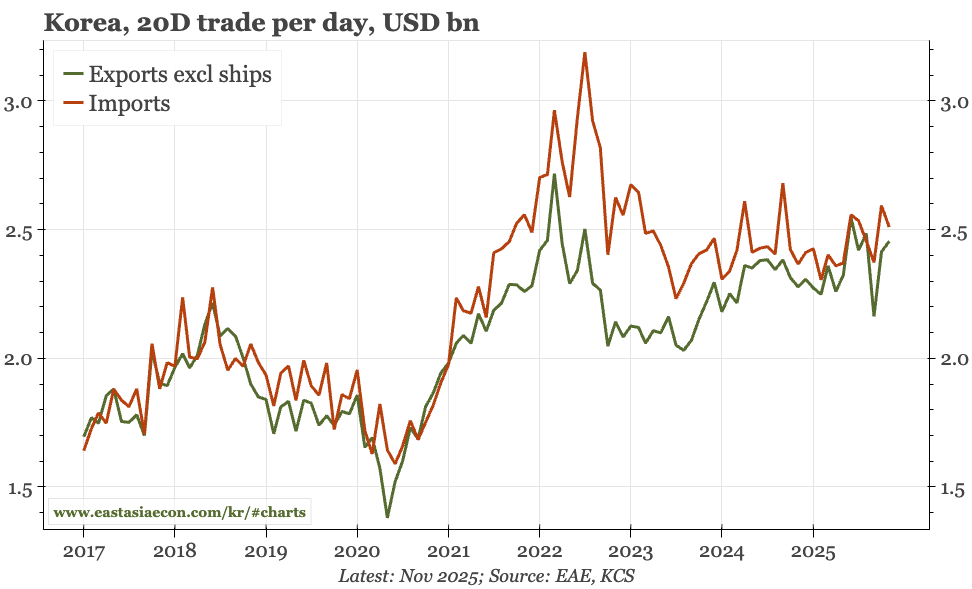

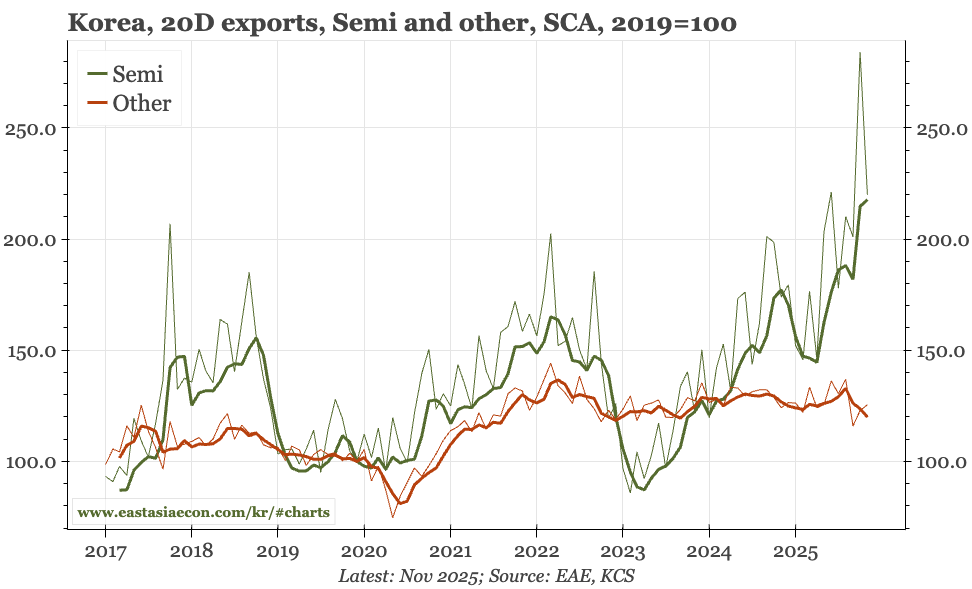

Given the extreme supply-demand tightness in the memory market shown by the spectacular rise in spot DRAM prices, there must be some upside risk for Korea's cycle. But that still isn't appearing in the data, with export growth in today's data for the first 20 days of November remaining modest. The weakness of growth has helped dampen inflation, with PPI in October rising just 1.5% YoY. That is, however, a bit higher than in previous months. Given import price trends, I wouldn't expect upstream goods price inflation to accelerate quickly. Services prices should be held down by the softness of the labour market, though the gap between upstream and downstream services inflation remains puzzlingly wide.