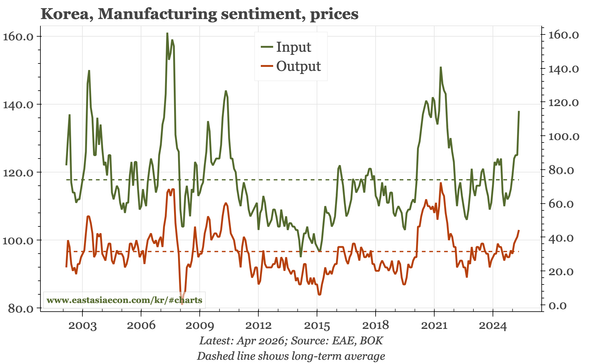

Korea – prices up, sentiment down

The easy takeaway from the rise in prices and fall in sentiment in the BOK's business sentiment survey for March/April is stagflation. I think there are reasons as yet to discount the idea that activity has slowed, but if that is right, then the rise in inflation makes BOK rate hikes more likely.

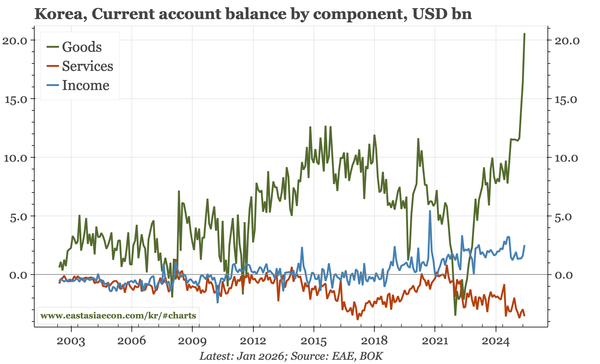

Korea – no change in BOP or CPI...yet

The CA surplus was strong in January, but while NPS outflows eased, retail buying of offshore equities remained high. Core inflation ticked up to 2.3% YoY, but that was related to holiday spending. The impact of the Middle East war will only start to be seen from March data.

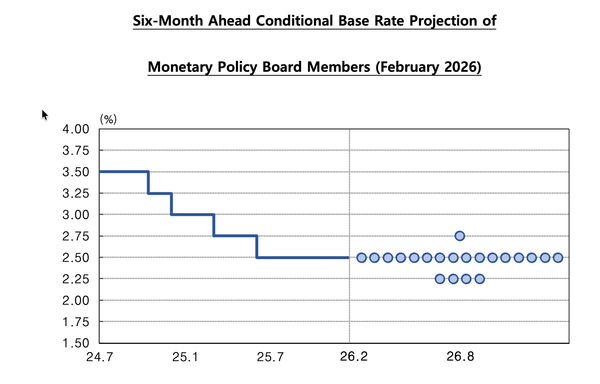

Korea – BOK remains cautious

The tone from today's BOK meeting was cautious. The new rate dot plot suggests that at the margin risks for policy are still weighted towards loosening, the upgrade to the GDP growth forecast was only 0.2ppts, and having made that change, the bank thinks risks to the outlook are now balanced.

Korea – narrow cycle, but still improving

Business sentiment in today's BOK survey returned to the level that has historically divided loosening and tightening cycles. Tomorrow, the bank will likely raise its 2026 growth forecast to above its 2% estimate of potential. The rates market has already priced this, but the currency can move more.

Korea – consumer confidence and PPI

The continued strength of consumer confidence in today's February survey might be hinting at a broader cyclical upturn. At the same time, house price expectations eased. CPI expectations were stable at 2.6%, and likewise, today's PPI for January doesn't point to a big near-term change in inflation.

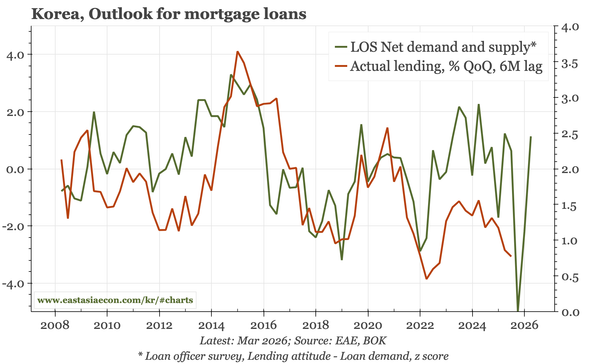

Korea – household debt down, property prices up

The BOK's quarterly data show household credit eased under 75% of GDP at in 2025 for the first time since 2017. However, the BOK is concerned that the ongoing rise in house prices will undermine this progress. The bank's own loan officer survey suggests a bounceback in lending is indeed a real risk

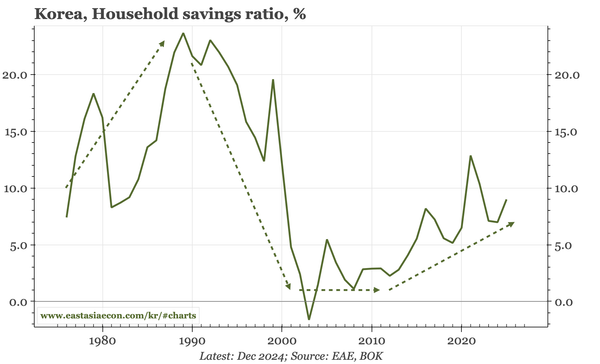

Korea – consequences of higher savings

The BOK recently published some nice research highlighting the rise in the household savings ratio. That is an important phenomenon, helping explain the weakness of consumption, the rise in the current account surplus, and being intertwined with the surge in Korea's overseas equity buying.

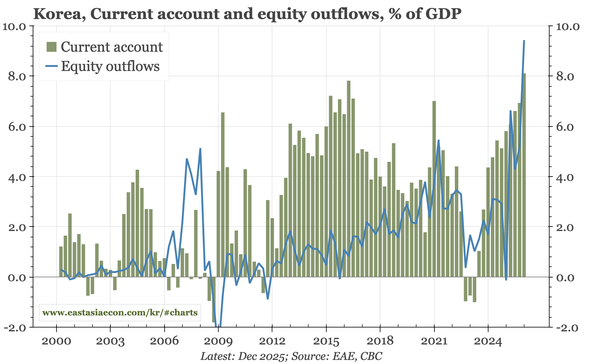

Korea – record CA, record equity outflows

Korea's current account reached a record high in Q4. But equity outflows, remarkably, increased even more. The balance between the two should diverge through 2026. The CA surplus can be expected to grow on the back of the semi supercycle, while there are four reasons to think net outflow should peak

Korea – still all about exports

Today's data releases show the domestic economy bottoming out, but not yet growing much. The upside risk rests on 1) exports, which the BOK in its last official forecast thought would only grow 1.4% in 2026 and 2) capex, with Samsung and SK Hynix this week pledging big increases.