Subscribers Only

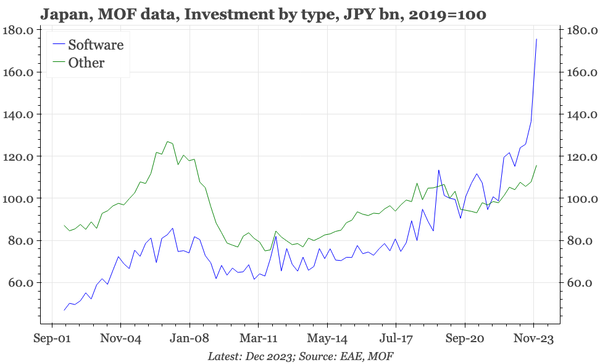

Japan – stronger capex

The big bounce in capex in Q4 suggests an upwards revision for GDP, and if sustained, potentially better productivity growth. However, wage growth was soft, and as a result, there wasn't much reversal of the sharp fall in the labour share of Q3.