Last week, next week

This is what happened on East Asia Econ this week.

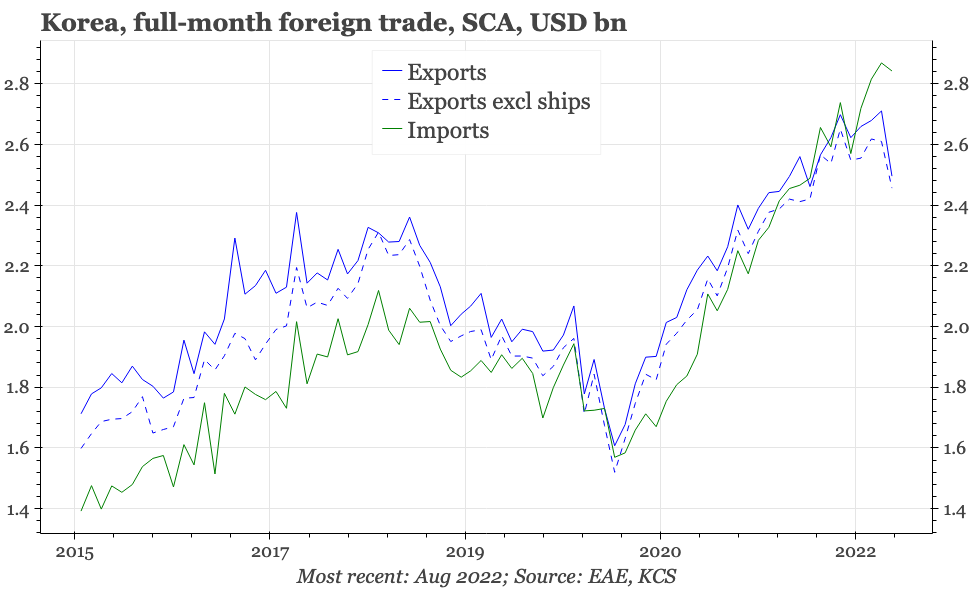

August export data for China, Korea and Taiwan dropped sharply. That makes it more likely that the industrial cycle is turning, with further weakness to be expected in the next few months.

The three data releases this week were soft: exports fell, dimming what has been the one bright spot for the economy in the last few months; underlying price trends, particularly in PPI, continue to look more deflationary than inflationary; and monetary data in August remained weak, with little reason to suggest any upturn in the economy. With this backdrop, the two most important questions for investors are whether the economic slowdown turns to financial crisis, and whether the Party Congress leads to a turn in policy. The former seems a bigger risk than the latter, and without a turn in policy, the asset that looks most vulnerable to China's deteriorating macro picture is the CNY.

The wage data for July don't change the macro picture. Wages are creeping up, but are rising less quickly than inflation, and the labour market isn't yet tight enough for nominal wages to accelerate much more. The Economy Watchers survey rebounded in August, and is at a level consistent with mild GDP growth. But the survey isn't strong or stable enough to be thinking in terms of a meaningful acceleration in the sluggish pace of the post-pandemic recovery.

Taiwan's exports fell sharply MoM in August, matching the deterioration seen in the Korean export data that were released a few days earlier. Leading indicators continue to point to more downside ahead. Inflation in Taiwan has likely peaked, and should decline in the coming months. The two risks around that are first, rising food prices, and second, cost inflation in services. There are reasons to think that services price might rise further from here, but for now, that seems like a tail risk.

The Japanese data for August on Thursday will complete the export picture for the region. There's also machine orders and the MOF's quarterly survey, which will set the scene for next month's more comprehensive BOJ Tankan. On Friday, China will release activity data for August. They likely won't do much to change our understanding of the economy. Also worth watching for next week will be labour market data in Korea, and wages in Taiwan.