Last week, next week

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

Both China and US are sounding very happy about the results of the trade talks at the weekend, and promise that an agreement will be released in the next few hours. The comments from both sides – and the smile on the face of one of Chian's negotiators, Li Chenggang – suggest that tariffs will be coming down more than the 80% level that President Trump talked about on the eve of the talks. Despite those remarks, both China and the US would want a bigger reduction than that, China because 80% is still way too high for anyone still wanting to export to the US, and for the US because 80% would still mean a big rise in prices for its consumers.

On the economy, it is highly unlikely that China will have given anything substantial in return. The presence of Wang Xiaohong, the official in charge of China's anti-fentanyl efforts, at the talks provides a hint of the area where both sides will find it easier to boast about progress as having being made. But whatever has been agreed to, any US-China deal that substantially reduces tariffs would still obviously matter a great deal for markets in Asia:

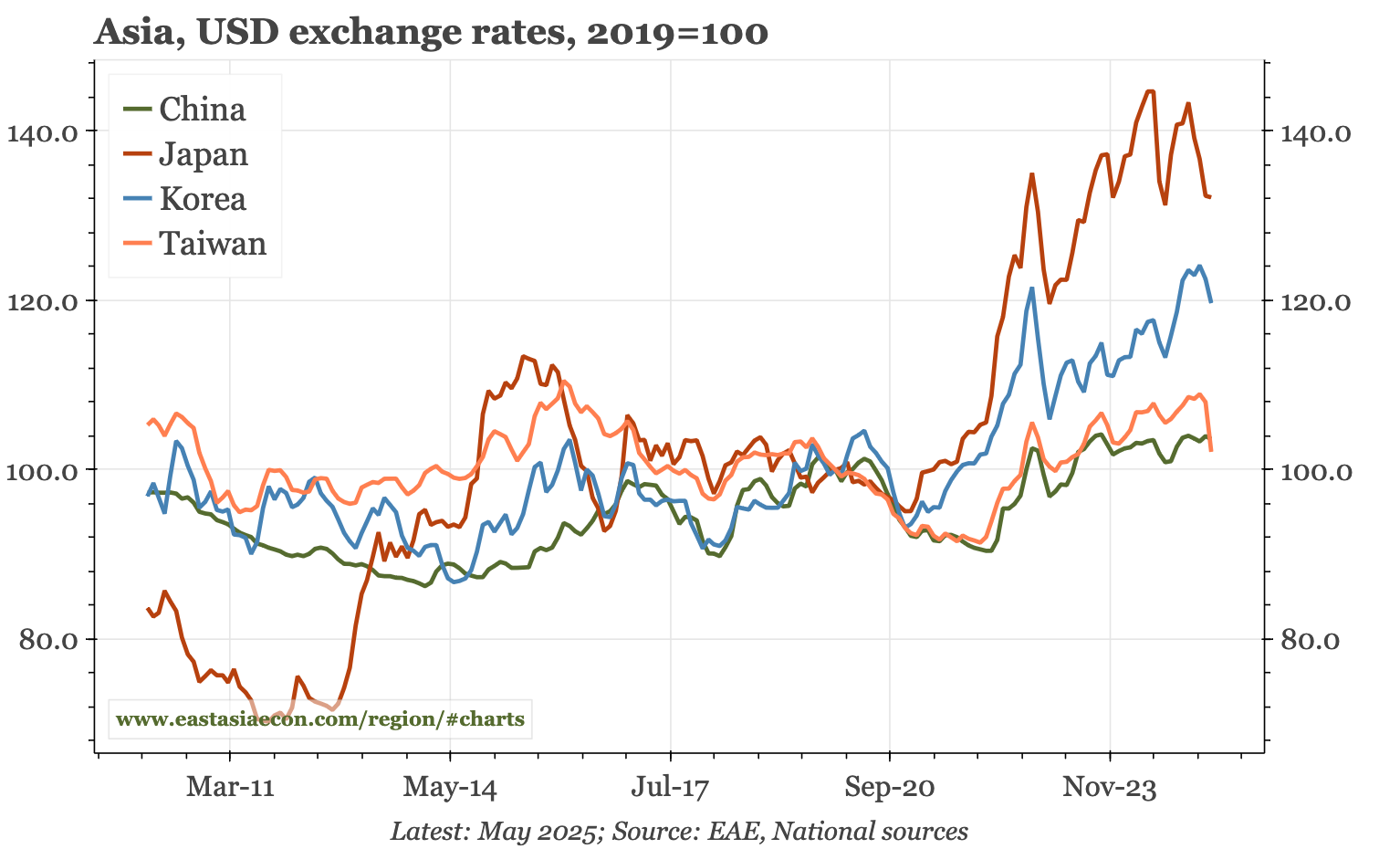

- I think that Asia appreciation relative to the dollar, a trend that was a theme at least at the beginning of last week, is more likely if the Trump administration doesn't drive the world economy into recession. That said, if there is a real drop in US-China tariffs, then some of the moves of currencies of the last week will likely reverse, at least for a while.

- Today's announcement will also impact how investors view US negotiations with other economies. With the US quickly stepping back from the brink with China, when it has already signalled that trade talks with both Korea and Japan will take months, markets should remain worried that sectoral tariffs won't be dismantled in the same way.

- A fall in tariffs will reduce some of the economic slowdown that was otherwise in the works for China. I wouldn't expect a real rebound, but the domestic market reaction to a reduction in tariffs will be even more positive than the way investors greeted last week's monetary policy easing.

With all that, the big news of the week will be the details of whatever US-China deal has been reached. Beyond that, it will be a quiet few days for releases. The highlight will be the summary of opinions of the last BOJ meeting. Japan's EW survey today will be interesting, likely showing a further decline in household sentiment. That's followed at the end of the week by Q1 GDP. This week will also bring an important export update with today's trade data from Korea for the first ten days of May. Korea will also release labour market data on Wednesday.

Thematic

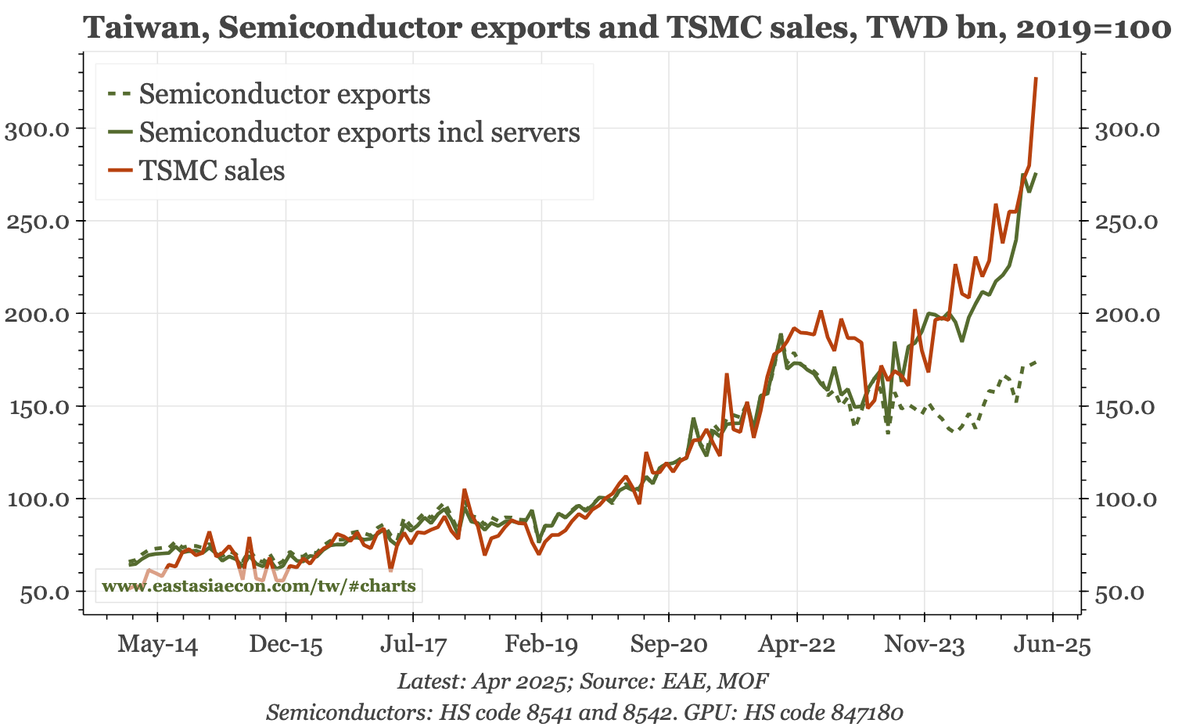

Taiwan – TSMC, Trump and the TWD. I can't claim to have expected the 10% surge in the TWD in the last couple of days. But I have been arguing for a while that the risks of a structural appreciation of the currency were real and rising. This is a brief presentation from March that highlights the issues.

Cycle

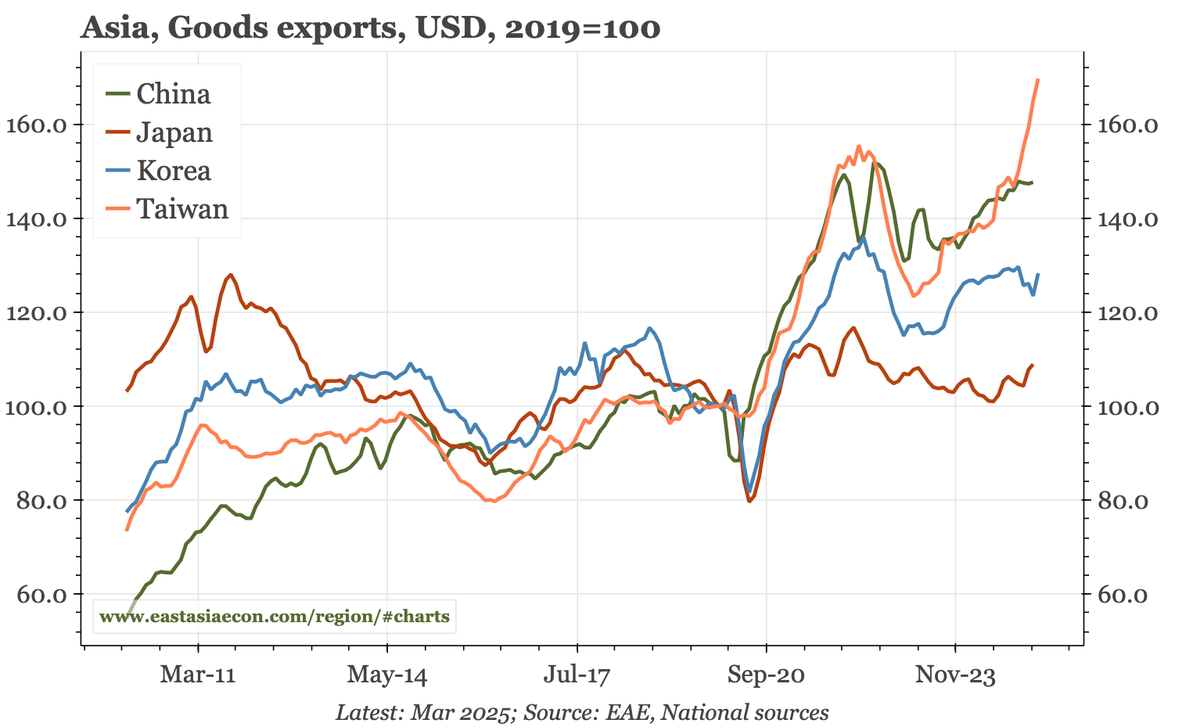

Cycle update – US exports down, but ROW up. The expected fall in exports to the US did happen in April, but that was offset by stronger shipments to ROW. I wouldn't expect that to continue, but it is worth noting that today's data showed an increase in imports of components, which would usually indicate stronger exports in the next 3M.

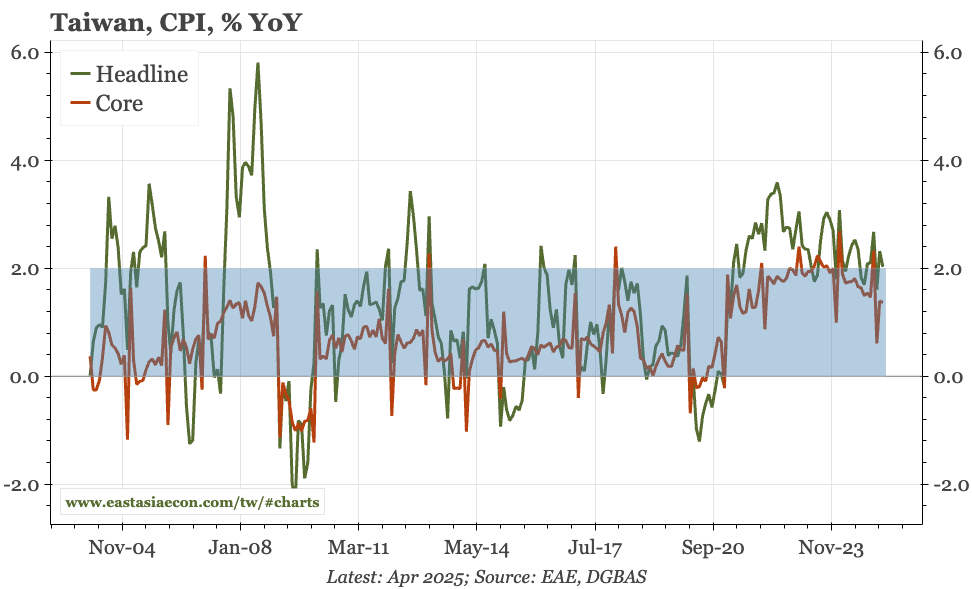

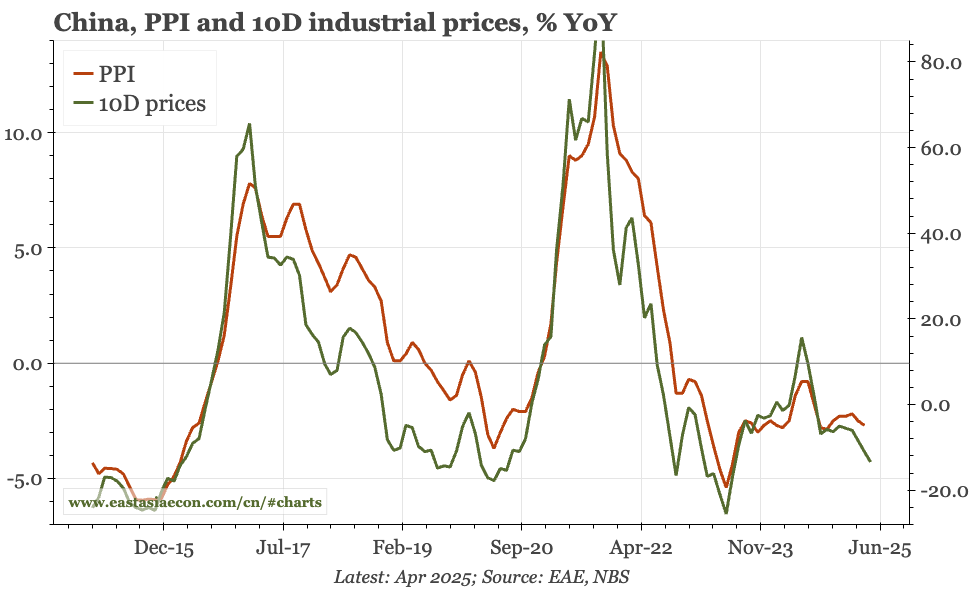

Cycle update – inflation stuck. After the deflation of much of 2024, core sequential inflation has now been positive for six months. But it is now still only +0.2% annualised, and doesn't look to be going higher. Indicators for PPI suggest even more deflation ahead, with the one exception being the decline in the USD.

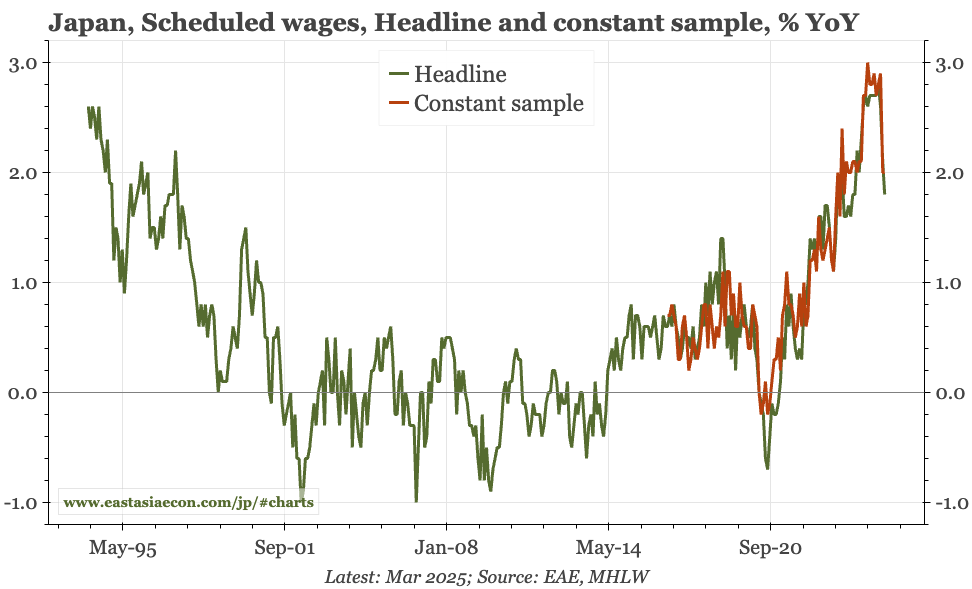

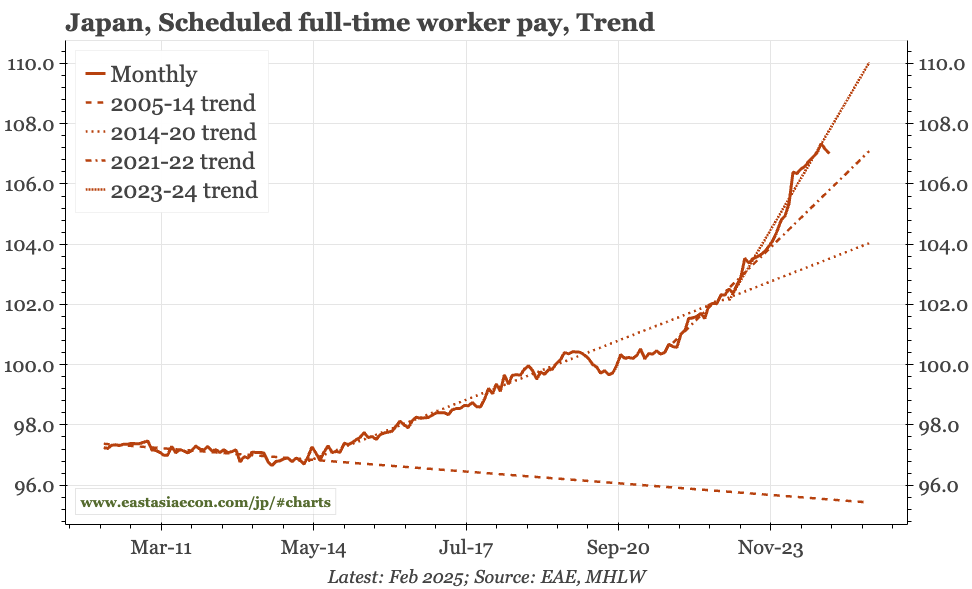

Cycle update – wage growth down, now waiting for April. With the slowdown in official wage growth in the last couple of months being so sharp, and so at odds with other labour market developments, I would assume it is due to technical factors. I'd be more concerned if the new shunto isn't reflected in this month's SPPI print, and wages next month.