Subscribers Only

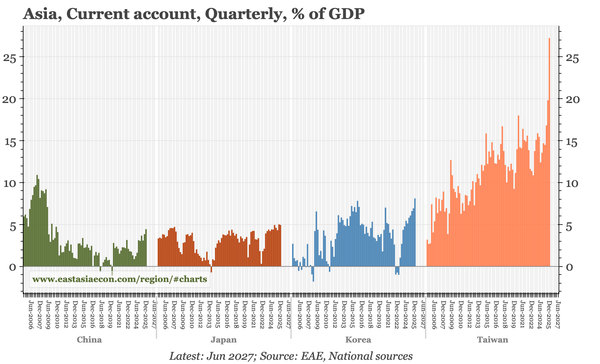

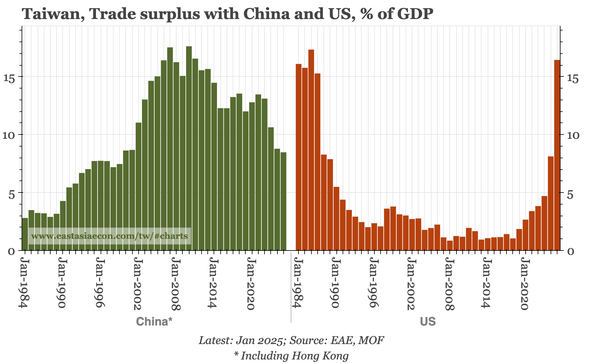

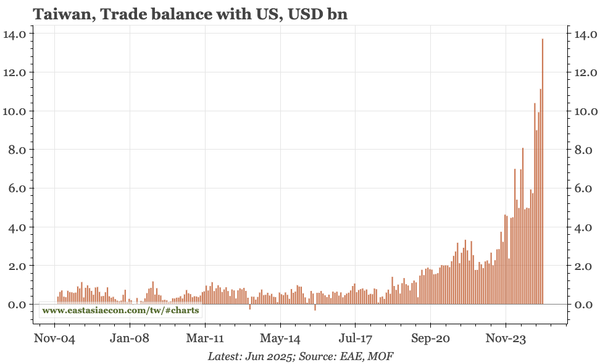

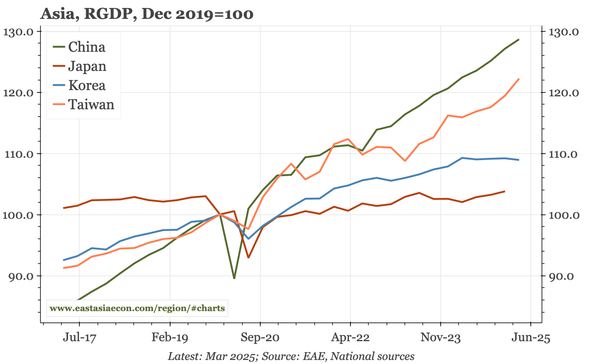

Taiwan – export surge continues

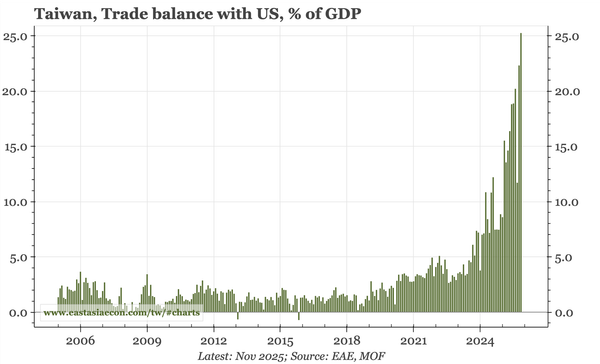

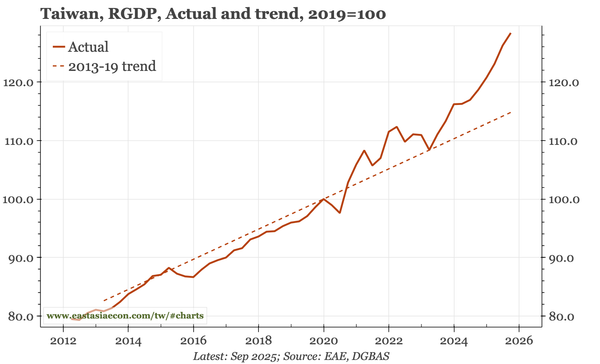

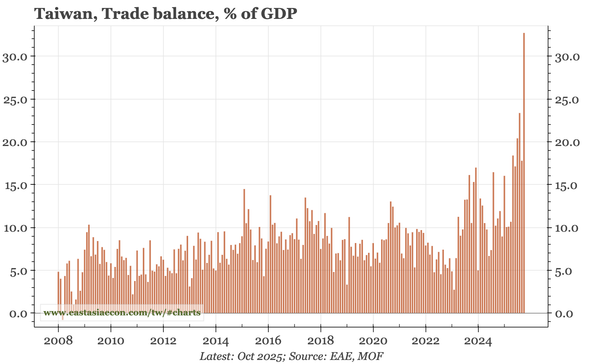

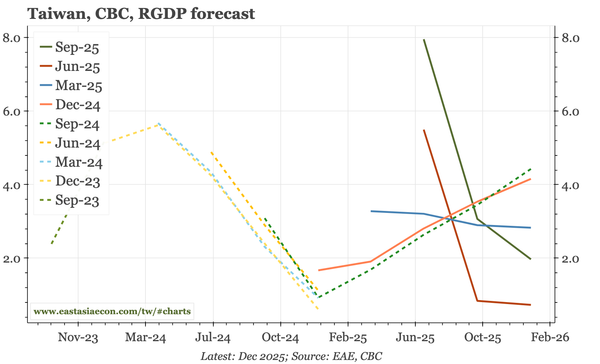

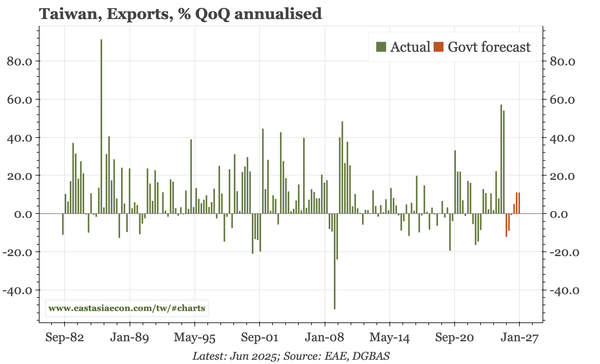

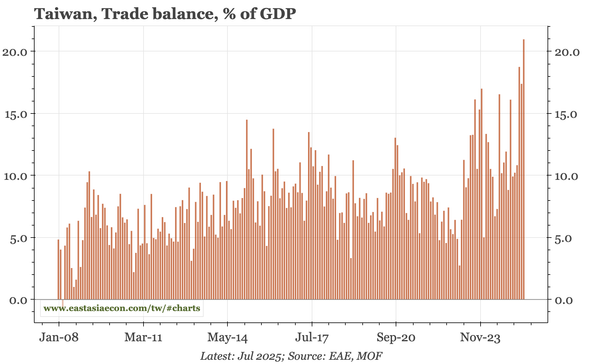

Exports in March were strong again. There aren't yet signs of the Iran war derailing the chip cycle, and while energy imports will increase more quickly, the impact on the trade surplus will be limited. The outlook for Taiwan as of now is resilient growth and higher inflation.